Provaris continues to focus on the economic viability across the entire hydrogen supply chain in Europe.

Hydrogen is an essential component of global decarbonization, serving as a raw material for chemicals, energy storage, and electrification. Provaris focuses on the economic viability of the full hydrogen supply chain, from production to delivery.

The hydrogen sector now has its first mature clean projects operating worldwide, backed by about US$110 billion in investment across over 500 projects in various stages. These projects account for over 6 million tonnes per year of committed capacity, with 1 million tonnes already online. By 2030, global supply could grow by an additional 3 to 8 million tonnes.

Europe is third in investment ($19 billion), but may account for almost two-thirds of projected global clean hydrogen demand by 2030. Policies like RED III, CBAM, and ETS could support up to 5 mtpa of EU demand.

Hydrogen Industry – Moving toward a more mature era

Progress in the hydrogen industry has faced delays, setbacks, high costs, and reduced forecasts. As large-scale projects are cancelled, the industry is entering a more disciplined phase, such as solar, wind, and batteries.

Provaris views this shift positively, seeing potential for smaller hydrogen projects (100–300MW) that suit its marine transport and storage solutions. If demand is secured, 3 to 8 million tonnes of additional supply could be achieved by 2030 through cost-effective methods such as compression.

Figure 1: Global hydrogen sector investment and capacity distribution

Compression is a “ready to use” enabler for Europe’s need for “low cost” hydrogen

Provaris views compression as a simpler, cost-effective approach to support future hydrogen projects and investment decisions, closely matching production volumes with industrial demand. This strategy aims to advance the hydrogen industry’s growth.

Key benefits of compression for storage and marine transport are:

- Low energy use: Only 3% compared to ammonia’s 30% over the supply chain.

- Established technology: Hydrogen compressors up to 700 bar are available from major OEMs like Baker Hughes.

- Lower capital requirements: Simpler and less capital-intensive than ammonia or liquefaction.

- Best fit for small to mid-scale production: Ideal for 100-300MW projects meeting actual market demand.

- Hydrogen stays pure and gaseous: Meets Europe’s policy and market needs.

EU Government Policy, Social License and billions in subsidies to accelerate the Hydrogen Industry

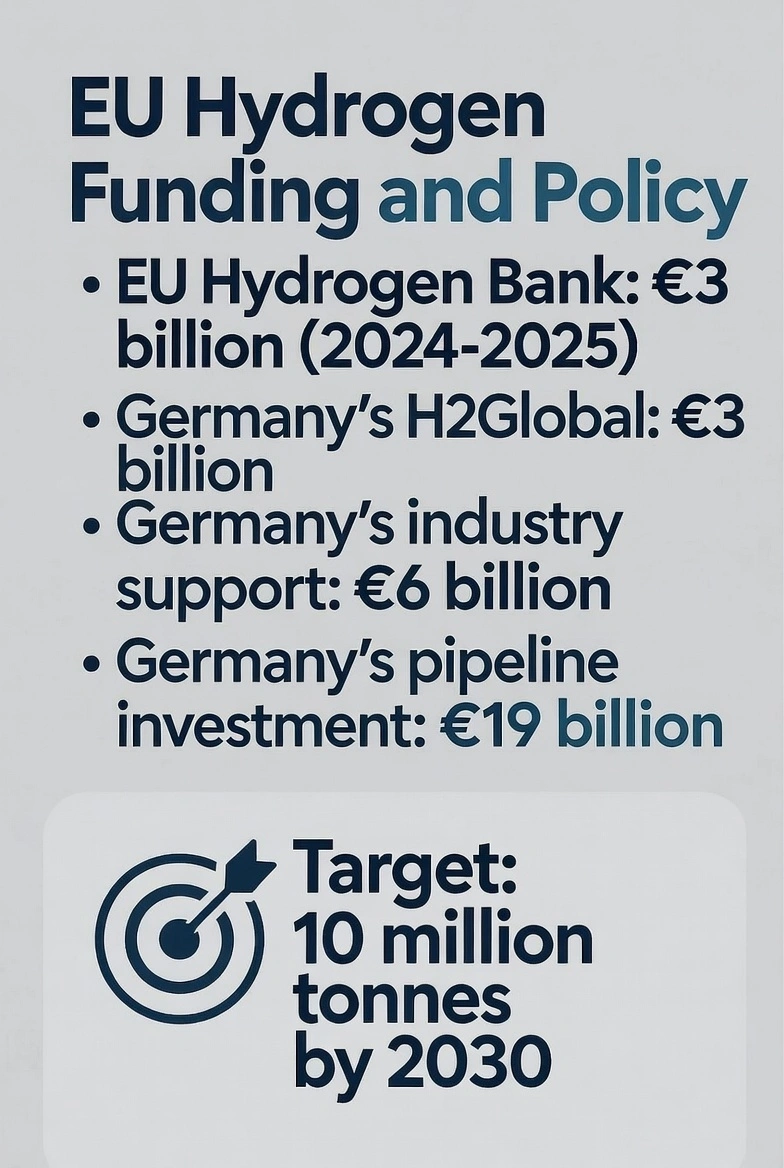

The EU Hydrogen Strategy targets 10 million tonnes of renewable hydrogen production and import by 2030, prioritizing industry, mobility, and energy storage. Subsidies and quotas under REDIII encourage electrolysis-based production to help cut emissions by 55% by 2030. Germany is investing €19 billion in a 9,000 km hydrogen pipeline network set for completion between 2028 and 2032.

Figure 2: EU Hydrogen Funding and Policy Timeline

Germany has announced plans to revise its hydrogen policies, prioritising imports to reduce costs. Hanna Schumacher of the economy ministry stated that imports would be prioritised for cost-effectiveness. The EU Hydrogen Bank is supporting renewable hydrogen production with €3 billion in auctions set for 2024-2025. Germany’s H2Global scheme launched a second auction this year, also with a €3 billion budget. National programmes in Germany, France, Spain, and Italy are providing billions in grants and incentives.

Increasing demand is vital for supply growth. Germany introduced a €6 billion initiative to help industries manage higher hydrogen costs and support decarbonisation, now including CCS technology in climate contracts. Targeting energy-intensive sectors like chemicals, steel, cement, and glass, the government will provide 15-year subsidies for companies transitioning to cleaner processes, protecting them from fluctuating energy and carbon prices.

Case Study for Import

RED III is driving a 1.6 Mtpa refinery market demand in Europe, with 40% met by domestic supply and 60% to come from imports

- Refining in Europe is expected to be one of the earliest–moving demand sectors supported by RED III, but currently has a supply gap with European production.

- To date, there is 0.2 mtpa of binding offtake in refining that is currently renewable, which qualifies as RFNBO and can support RED III quotas.

- A substantial portion (about 40%) of large, commercial-scale (50MW or more) renewable projects in the planning and committed stages in Europe intend their hydrogen production for use in refining, with Germany, Spain, and the Netherlands.

- Additional EU capacity from existing FEED and FID+ projects intended for the refining sector could meet a portion of the 1.6 mtpa demand; however, there is still a 1.0 mtpa demand gap that could spur additional domestic growth or international imports.

Summary

Europe’s push for a hydrogen-powered future is driven by substantial government investment and incentives, especially with Germany and the EU leading funding efforts. Despite progress, a supply gap remains in forecast industry demand. Bridging it demands faster domestic projects and efficient low-cost imports to meet climate goals and maintain competitiveness.

Provaris leverages its strategic partners and expertise in hydrogen transport to address Europe’s market needs. Supported by EU and German funding, Provaris aims to deliver scalable and cost-effective solutions for shipping green hydrogen, focusing on the 1.0 mtpa supply gap in refining and helping refiners meet climate targets.