How fluctuations in the USD, AUD, and emerging market currencies shape commodity prices, margins, and investor strategies

FX flows & metals are playing an increasingly bigger role in setting direction for mining equities on global exchanges. Currency fluctuations between the U.S. dollar (USD), Australian dollar (AUD), and currencies of emerging markets directly affect commodity prices, costs of operations, and reported earnings. As most metals are quoted in USD, miners have a structural exposure to currency that can add to or detract from profitability.

Global currency flows directly impact mining returns across major resource economies.

This report examines the mining return-exchange rate relationship with particular reference to the AUD, USD, and major emerging market currencies. It considers hedging strategies used by major mining operators, presents case studies of recent FX impacts on mining results, and derives implications for investors on the ASX, LSE, and NYSE.

Currency Dynamics and Commodity Prices

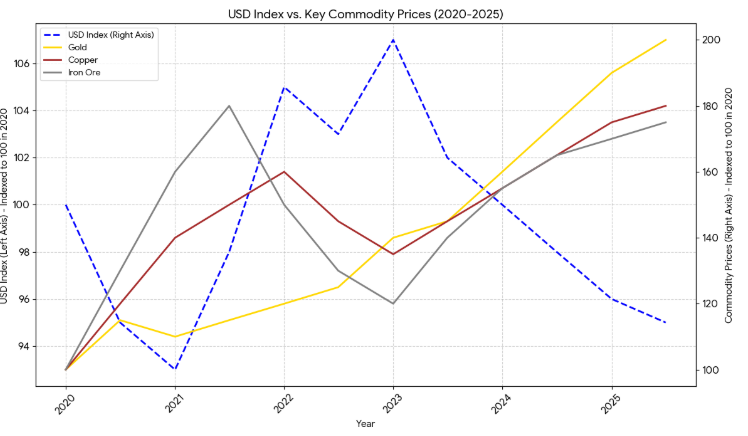

USD remains the world’s benchmark metal trade currency. A strong dollar reduces commodity demand by raising other currency users’ costs and has been continuously observed in gold, copper, and iron ore markets. Commodity prices weaken if the dollar rises, compressing mining earnings. USD weakness supports higher metals prices, providing relief to exporters.

Commodity prices often move inversely to the U.S. dollar, shaping mining revenues

For Australia, AUD is a commodity currency. Its value is heavily associated with iron ore and coal exports. Devaluation of AUD vis-à-vis USD is a natural hedge to Australian miners as revenues in USD are converted into higher local currency earnings. A high AUD, however, can reduce competitiveness by pushing up costs and compressing margins.

Emerging market currencies add another level of complexity. Platinum group metal margins in South Africa are materially influenced by rand volatility. Peso movements impact copper producers in Chile, and rupiah trends influence nickel sector dynamics in Indonesia. These currency movements, coupled with shifts in global demand, create a never-ending game of balancing act for mining companies.

Hedging Strategies of Major Miners

Due to the magnitude of FX exposure, mining companies use a variety of hedging structures to offset risks.

Mining companies employ diverse FX hedging strategies to protect margins.

Forward Contracts and Swaps

The majority of miners hedge future exchange rates for currencies using forward contracts or swaps. The approach provides certainty on revenue or cost estimates but limits upside if currencies appreciate in their favor.

Options-Based Hedges

Others have a preference for options contracts, hedging against adverse movements without restricting flexibility. These have premiums and are more expensive but less restrictive.

Natural Hedging

Greater utilization by large miners of natural hedging includes balancing debt, buys, and investment in the same currency as operating costs. BHP, for example, has significant AUD-denominated costs, which offset some of its revenue exposure.

Selective Hedging Policies

Hedging is not uniform in the industry. Rio Tinto employs selective hedges, while most junior miners on the ASX avoid currency contracts to minimize expenses. This disparity is likely to explain disparities in earnings resilience when FX shocks occur.

In Deloitte’s 2023 Mining & Metals Outlook, international mining firms’ treasury operations have expanded, an indicator of rising emphasis on FX risk management. They mostly now employ rolling hedge models that balance operational flexibility with a hedge against volatility.

Case Studies: Currency Impacts on Mining Results

Australia: AUD Volatility and Iron Ore Tycoons

For ASX-listed miners such as BHP, Rio Tinto, and Fortescue, AUD/USD movement is central to performance. A falling AUD makes reported profits stronger by increasing the value of USD-denominated revenues. An appreciation of AUD undoes this advantage, narrowing profit margins even when commodity prices are unchanged.

Australian miners like BHP and Fortescue benefit from AUD weakness against the USD

In 2023, BHP reported FX impacts contributed to EBITDA, which acted to offset some of the deceleration from lower iron ore prices. Iron ore-exposed Fortescue also cited AUD weakness as a favorable driver in its numbers. These figures are indicative of the currency cycle structural exposure of Australian miners.

South Africa: Rand Weakness and Platinum Margins

South African miners benefit when the rand depreciates against the dollar, as revenues from platinum exports are in USD but expenses are local. Anglo American Platinum and Sibanye Stillwater have routinely emphasized FX gains in reports. However, rand weakness also indicates local inflationary pressure and higher wage expense that can eat into the net gain.

Chile: Peso Depreciation and Copper Producers

At Chile’s Antofagasta, 2023 figures demonstrated the peso’s power to reduce cash cost per pound despite flat copper output. Downgraded pesos offset boom-and-bust global demand fluctuations. Lowly developed peso derivative markets limit long-dated hedging, exposing miners to jittery whipsaws.

Emerging market miners such as those in Chile and South Africa are heavily exposed to local currency swings.

Hedging Risks: Nickel Market Turmoil

The 2022 LME nickel crisis brought the risks of currency-hedging into sharp relief. Sudden spikes in price led some producers and traders to close out hedges at significant losses. S&P Global reported that Chinese miners increased hedging activity but paid secret costs when contracts went sharply against them. The episode underscored the need for responsible hedging models that utilize FX derivatives as insurance, not speculation.

Implications for Investors on ASX, LSE, and NYS

Understanding Hidden Currency Exposure

Investors must consider how FX flows & metals together influence mining stocks. Two companies with comparable commodity streams may report different earnings due to currency movements. Both BHP and Freeport-McMoRan produce copper, but AUD translation effects make BHP even more exposed to FX movement.

Investors in ASX, LSE, and NYSE-listed miners face different FX exposures depending on company location and reporting currency.

Hedged vs. Unhedged Investments

Others prefer exposure to unhedged miners for some extra volatility in return for commodity-linked returns. Others choose companies with hedging programmes designed to stabilise profits. FX translation gains or losses are normally disclosed on an annual basis, offering valuable insights into corporate strategy.

Currency Overlays for Portfolios

Sophisticated investors employ currency overlays through the addition of FX positions to mining stock holdings. As an example, weaker USD anticipation can justify over-weighting copper miners such as Freeport-McMoRan. Anticipation of strength in AUD can result in reduced exposure to Australian miners sensitive to margin compression.

The presence of both ASX-, LSE-, and NYSE-listed miners provides natural diversification in currency. The presence of Australian miners adds AUD exposure, South African miners add volatility from the rand, and U.S.-listed miners add stability in USD. This spread mitigates FX-driven volatility within a portfolio.

Valuation Adjustments and Risk Premiums

FX assumptions must be incorporated in equity valuations. Discount cash flow models that ignore currency volatility will tend to overestimate the free cash flow stability. Risk premiums are generally applied by analysts in miners with riskier FX jurisdictions, which captures uncertainty.

Macro Themes and Future Outlook

Dollar Direction and Metals Pricing

The path of the U.S. dollar in the future will remain a key driver of commodity markets. Prolonged USD weakness, possibly triggered by Federal Reserve accommodation, can support metals prices and commodity currencies. Re-appearance of USD strength would be perilous to prices and margins.

South African, Indonesian, and Chilean miners will continue to enjoy shallow FX derivative markets and restricted long-hedging. External funding access and volatility management will continue to be essential to competitiveness.

Innovation in Hedging

Advances in treasury technology, including algorithmic hedge optimisation and blockchain settlement, are expanding the FX management toolkit for miners. These innovations do entail counterparty and liquidity risks.

Commodity Pricing Beyond USD

De-dollarisation rhetoric is also challenging the potential of commodity pricing patterns. Major change cannot yet be anticipated in the short term, but even some movement would recast FX-commodity correlations and investor patterns.

Investor Positioning against a Volatile FX Backdrop

Investor behavior in mining equities is now more led by expectations of FX flows & metals correlations than by commodity cycles alone. With volatility in EM as well as DM currencies set to persist, institutional investors are becoming increasingly tactical. Global asset managers and hedge funds are increasingly actively incorporating currency themes into sector allocation models, stress-testing mining equities under various exchange rate scenarios.

A stronger USD, together with weaker commodity demand, for example, is a twin headwind, squeezing revenues while also ballooning debt service costs for miners with dollar liabilities. Conversely, in the case of a weakening USD and commodity strength, mining equities can outperform the broader indices.

Long-only investors such as pension funds also construct FX sensitivity by diversifying. Investing across miners with operations in different jurisdictions provides exposure to offsetting currency trends.

For instance, holdings in Australian iron ore producers can be balanced by positions in South African platinum or Chilean copper producers, reducing the portfolio’s exposure to a single currency outcome. Exchange-traded funds (ETFs) in global mining have also risen hedging overlays, allowing investors to choose from currency-hedged and unhedged structures.

At the retail level, investors are increasingly utilizing derivative products to hedge FX exposure in buying foreign-listed mining equities. For example, a European investor who buys NYSE-listed mining stocks can utilize an EUR/USD hedge to fix returns. Such practices demonstrate the growing recognition that FX movements are not tangential but at the center of mining investment returns. As global financial conditions tighten and commodity demand prospects remain uncertain, the ability to predict and manage FX-driven outcomes will continue to distinguish successful investors from underperforming peers.

Currency shifts remain as important as commodity cycles in determining mining stock returns.”

Also read: https://colitco.com/australia-green-metals-battery-superpower-2030/

Conclusion

FX flows & metals are partners in influencing mining stock performance. Foreign exchange volatility governs revenue translations, cost bases, and profit margins, often exercising as much influence as underlying commodity prices.

For miners, hedging strategies remain the cornerstone but tricky, requiring a nuance between protection and adaptability. For investors, assessing latent FX exposures, diversification of portfolios, and company-specific treasury strategies is essential for sound decision-making.

As uncertainty around the dollar tightens markets worldwide, as emerging market currencies move up exuberantly, and as hedging habits change, FX flows’ correlation with metals will also continue to influence mining equities’ performance on the ASX, LSE, and NYSE.

FAQs

1. How do currency fluctuations affect mining stocks?

Currency movements influence both revenues and costs for mining companies. Since most metals are priced in U.S. dollars, a stronger dollar generally reduces local-currency earnings for miners. Conversely, a weaker domestic currency, such as the Australian dollar or South African rand, can boost profitability when revenues are converted back into local terms.

2. Why is the U.S. dollar important for metal prices?

The U.S. dollar is the global benchmark for commodity trading. When the dollar strengthens, metals become more expensive for non-U.S. buyers, often reducing demand and lowering prices. A weaker dollar usually supports higher commodity prices, benefiting exporters and miners.

3. How does the Australian dollar (AUD) impact iron ore and gold miners?

The AUD is closely tied to commodity exports, particularly iron ore and gold. A weaker AUD increases the local value of USD-denominated revenues, boosting reported profits for ASX-listed miners. Conversely, a strong AUD can compress margins by raising costs and reducing international competitiveness.

4. What hedging strategies do mining companies use against FX risks?

Mining companies commonly use forward contracts, currency swaps, and options to lock in exchange rates. Some employ natural hedging by aligning debt and expenses with the same currency as revenues. Large companies such as BHP and Rio Tinto adopt selective hedging policies, while smaller miners often avoid complex hedges due to cost.

5. Which emerging market currencies influence mining profitability?

Key emerging market currencies include the South African rand, Chilean peso, and Indonesian rupiah. Fluctuations in these currencies directly impact platinum, copper, and nickel miners by altering local cost bases and revenue conversions. Volatile EM currencies can either cushion or intensify commodity market swings.

6. How do investors protect portfolios from currency risk in mining equities?

Investors use diversification across regions, currency overlays, or FX-hedged ETFs to manage risk. For example, holding miners listed on ASX, LSE, and NYSE spreads exposure across AUD, GBP, ZAR, and USD. Professional investors may also directly hedge with currency derivatives when buying foreign-listed mining stocks.

7. Are ASX, LSE, and NYSE mining stocks equally exposed to FX movements?

No. ASX miners are heavily impacted by AUD fluctuations, LSE miners often face exposure to emerging market currencies, and NYSE-listed miners are more stable due to the USD’s global dominance. Investors should evaluate each listing’s FX sensitivity when comparing returns.

8. What role did FX volatility play in recent mining earnings reports?

Recent earnings reports from companies such as BHP, Rio Tinto, and Antofagasta highlighted FX translation gains. A weaker AUD and Chilean peso helped offset weaker commodity prices, while South African miners benefited from rand depreciation. These cases show how currency moves can materially alter earnings.

9. Can a strong U.S. dollar hurt commodity prices and mining profits?

Yes. A strong dollar usually pressures metals like copper, iron ore, and gold by making them more expensive globally. This reduces demand and lowers revenues for miners, while increasing the burden of servicing USD-denominated debt.

10. Should investors consider currency-hedged ETFs in mining?

Currency-hedged ETFs allow investors to gain exposure to mining stocks without being fully exposed to FX volatility. These products are useful when investors expect sharp movements in exchange rates but still want mining sector exposure. However, they may reduce potential gains if currency shifts move in a favourable direction.

{kind=link}