Duratec Limited (ASX: DUR), one of Australia’s leading engineering, construction, and remediation contractors, has announced a binding agreement to acquire 100% of Pacific Welding Australia (PWA), a Newcastle-based welding and fabrication firm, for a maximum consideration of A$12 million.

The deal, executed through Duratec’s wholly owned subsidiary WPF Duratec Pty Ltd (WPF), is subject to standard conditions precedent and compliance with the ACCC’s merger control regime. Completion is expected in or before early July 2026.

What the Duratec and Pacific Welding Australia Deal Actually Covers

The acquisition is structured in two parts. Duratec will pay an upfront sum of A$6 million, adjusted for working capital movements. On top of that, a maximum earn-out of A$6 million is payable at the end of FY28, tied to a combined FY27 and FY28 EBITDA hurdle of A$6.4 million.

Any earn-out payments will be funded through WPF’s existing cash reserves. The upfront tranche comes from Duratec’s cash reserves and existing bank facilities.

PWA recorded A$14.8 million in revenue for FY25, generating A$1.67 million in EBITDA. That gives Duratec a target with a real revenue base and a clear earnings growth pathway through the earn-out structure.

Who Is Pacific Welding Australia?

Founded in 2010, PWA is an Australian-owned specialist in project-based welding, mechanical services, and fabrication. It operates across Oil and Gas, Energy, and Mining sectors, working with a broad client base from its base in Newcastle, New South Wales.

PWA operates from a 1,000m² workshop in Newcastle, NSW, serving clients across Oil and Gas, Energy, and Mining. [PWA]

In 2022, the company cemented its Hunter Region commitment by establishing a 1,000 square metre workshop. Today, PWA employs close to 60 personnel.

What makes PWA particularly attractive to Duratec is its certified status as a consignment holder of Steel Mains MSCL pipe and a licensed holder of Steel Mains Sintakote Coatings. These are niche technical accreditations that take years to build and serve as meaningful competitive barriers.

More significantly, PWA is the incumbent main contractor for fabrication, welding, and mechanical services at Orica’s Kooragang Island Facility in NSW. That client relationship alone anchors a steady and defensible revenue stream.

Why This Acquisition Matters for Duratec

Managing Director Chris Oates described the deal plainly:

“PWA is uniquely aligned to the services of WPF and provides a fantastic opportunity to scale WPF’s specialist expertise and self-perform model, while enhancing our service offering within the Energy and Mining and Industrial sectors.”

Oates added that the acquisition “further establishes WPF’s East Coast base and is a continuation of our expansion strategy within these sectors.”

That framing matters. This is not a pivot. It is a deliberate extension of what WPF already does, in a geography where Duratec has been building presence through back-to-back targeted acquisitions.

PWA joins a recent string of bolt-on buys by the Company. Duratec already acquired Hunter Coatings Pty Ltd, a specialist industrial painting and coatings contractor based in the Hunter Valley, and RGK Resources Pty Ltd, a Western Australian provider of inspection, maintenance, and rope access services. Each deal adds a specific capability or regional foothold, rather than a scattered diversification play.

The Strategic Picture: Self-Perform and Scale

The phrase “self-perform capability” is important here. In engineering contracting, the ability to perform work in-house rather than subcontracting it directly boosts margins, reduces project risk, and strengthens client relationships.

By integrating PWA into WPF’s operations, Duratec can now offer end-to-end fabrication, welding, and mechanical services on the east coast without relying on third parties for critical work. That positions WPF as a full-service national contractor in the Energy and Mining and Industrial sectors.

The Hunter Region, specifically, is an energy-dense corridor with significant Oil and Gas, Energy, and Mining activity. Having an established workshop, local workforce, and incumbent client relationships in that region gives Duratec a foothold that would otherwise take years to build organically.

The Hunter Region is a strategic industrial corridor in NSW, home to key Energy and Mining operations. [Wikipedia]

Key highlights of the deal:

- Maximum sale price of A$12 million (subject to adjustments)

- Upfront payment of A$6 million, funded from cash and bank facilities

- Earn-out of up to A$6 million tied to FY27 and FY28 EBITDA hurdle of A$6.4 million

- PWA FY25 revenue: A$14.8 million; EBITDA: A$1.67 million

- PWA workforce: approximately 60 personnel

- PWA workshop: 1,000 square metres, established in Newcastle in 2022

- Incumbent contractor at Orica’s Kooragang Island Facility

- Deal completion expected by early July 2026

Management Continuity Preserved

Duratec views PWA’s current leadership as a core part of the deal’s value. Current Directors Grant Davies and Ryan Jones have committed to continuing in senior management roles for a minimum of four years post-completion.

That retention clause is a telling signal. It tells the market that the existing client relationships and operational expertise will carry forward rather than walk out the door once the deal settles.

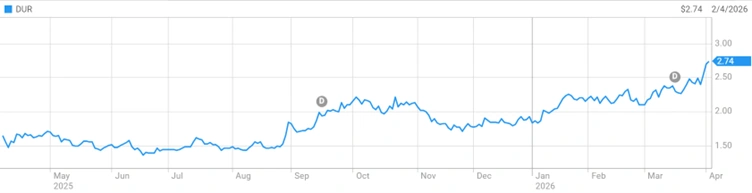

Investor Outlook: DUR Share Price and Market Position

Duratec (ASX: DUR) has had a strong run over the past 12 months. According to recent market data, the stock has consistently outperformed the broader Australian construction industry, which itself returned around 31% over the year.

DUR Price chart over a period of one year [ASX]

The PWA deal adds a revenue-generating, client-anchored business to Duratec’s portfolio without a large capital outlay, given that the earn-out structure reduces upfront risk. For investors watching the East Coast expansion story unfold, this acquisition is another piece of a deliberate and coherent growth strategy.

Also Read: Four Astronauts Are About to Go Where No One Has Gone in 54 Years

FAQ

Q: What is the Duratec Pacific Welding Australia acquisition?

A: Duratec Limited (ASX: DUR), through its subsidiary WPF Duratec Pty Ltd, has agreed to acquire 100% of Pacific Welding Australia for a maximum of A$12 million. The deal includes a A$6 million upfront payment and an earn-out of up to A$6 million tied to EBITDA targets for FY27 and FY28.

Q: What does Pacific Welding Australia do?

A: PWA is a Newcastle-based welding and fabrication company founded in 2010. It provides project-based welding, mechanical services, and specialist fabrication to clients in Oil and Gas, Energy, and Mining sectors. It is the incumbent main contractor at Orica’s Kooragang Island Facility.

Q: Why did Duratec acquire Pacific Welding Australia?

A: The acquisition strengthens Duratec’s east coast presence, expands WPF’s self-perform capabilities in the Energy, Mining and Industrial sectors, and provides direct access to established client relationships in the Hunter Region of NSW.

Q: When will the acquisition be complete?

A: Completion is expected in or before early July 2026, once conditions precedent are satisfied and ACCC merger control requirements are met.

Q: How is the deal funded?

A: The A$6 million upfront payment will be funded from Duratec’s existing cash reserves and bank facilities. Any earn-out payments will be funded through WPF’s cash reserves.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Past performance is not an indicator of future results. Readers should consult a licensed financial adviser before making any investment decisions.

Source:

Last modified: April 2, 2026