The Impending Supply Security of Critical Minerals Strategy: How Global Powers Securise Future Supply. Since these minerals are turning out to be indispensable for the modern economy, they are presently redefining the terms of global energy security and industrial hegemony. The transition to electrification faster than anticipated has brought lithium, nickel, cobalt, manganese, graphite, and rare earths into the category of strategic importance. They are no longer just commodities. Rather, these are deemed strategic assets that weigh on climate policies, defence might, and geopolitical influence.

The Impending Supply Security of Critical Minerals: Global Powers Redefine Energy and Industrial Future

Why Do Critical Minerals Constitute Security Now?

Energy systems are changing faster in a century. In addition, fossil fuels were the pillars on which hamlets of national security rested until electrification disrupted them. Such a shift calls for an unprecedented acceleration of materials that were hitherto considered niche.

EVs significantly require lithium, nickel, manganese, cobalt, and graphite materials. Rare earths are considered key materials for the production of permanent magnets used in EV motors and offshore wind turbines. Gallium and germanium constitute the backbone of semiconductor and clean-tech supply chains. Through copper and aluminium —mainstream metals, nowadays—grid connections, charging points are coming to the fore as priorities, and so on. Recycling is useful in the future, but it will not satisfy today’s steep hike in demand. New mines have lengthy approval phases, and capital needs are high. The processing infrastructure is centred in China, which is a strategic constraint. This reliance has prompted governments to move, intending to expand supply chains and diminish exposure to a single country’s control.

How Are the US, EU, UK, and Australia Acting?

Though each region has its distinct priorities, its playbooks have underlying themes in common. Governments are defining critical minerals, simplifying permitting, and funding upstream and midstream development projects. Partnerships are being established with resource-holding nations. Circular economy projects promote recycling, while ESG frameworks enhance transparency and trust.

The United States is emphasising industrial policy and financial incentives. The European Union is seeking to speed up permitting and construct midstream processing. The United Kingdom is utilising finance and technology. Australia, with extensive reserves, is transitioning from extraction to refining and advanced processing. Cumulatively, these plans are an expedient scramble for security of supply.

US pushes industrial policy, EU accelerates permitting, UK leverages finance and tech

The US Strategy: Incentives, Alliances, and Reshoring

Washington has placed the critical minerals at the forefront of its clean-energy and national security strategies. The Inflation Reduction Act offers tax credits for clean-tech production, and the Department of Energy guarantees loans to de-risk mining and refining efforts. The Defence Production Act has been leveraged to facilitate the domestic supply of battery and magnet materials.

Car manufacturers earn bonus credits when allied countries provide the minerals, encouraging firms to track supply chains meticulously. At the state level, extra grants and infrastructure incentives make the investment offer sweeter. Universities are educating the labour needed to ramp up mining and processing.

The US has bottlenecks in nickel sulphate production and graphite processing. Recycling programs and rare earth magnet plants are being seeded to fill gaps. Partnerships with Canadian and Australian firms are being supported by federal agencies, further stabilising North American supply resilience.

Among the listed, Albemarle is still a global leader in lithium, and MP Materials has led the development of rare earth separation capacity. Energy Fuels is working on rare earth refining, and Lithium Americas is advancing its Nevada clay project. Piedmont Lithium connects the US supply with Tesla and other EV makers. Copper giant Freeport-McMoRan remains a canary in the coal mine for electrification demand, while Novonix is developing graphite anode technologies.

The EU Strategy: Diversification, Faster Permits, and Midstream Investment

Brussels has proceeded more in the direction of regulation. The EU’s Critical Raw Materials Act includes targets for extraction, processing, and recycling by 2030. “Strategic” projects are given rapid permitting and access to financing by institutions such as the European Investment Bank.

The EU is focusing on partnerships with resource-endowed areas, notably Africa and Latin America. Car manufacturers like Volkswagen and Stellantis are co-funding offtake deals to lock in long-term supplies. Cathode, anode, and magnet factory investments in Germany, France, and Scandinavia are all meant to keep value closer to home.

Challenges persist. Energy prices are high enough to undercut refining competitiveness, and Europe still relies on foreign concentrates. Northern locations, however, possess cleaner energy sources with competitive opportunities. Portugal and Spain are pushing forward on lithium and copper prospects, while Finland and Sweden advance nickel, graphite, and rare earth supply.

Beneficiaries of the listed companies are Boliden and Eramet, expanding European mining output. Umicore is a leader in cathode materials and recycling, and Vulcan Energy is exploring geothermal lithium in Germany. Solvay is investing in rare earth processing, and Euro Manganese is developing a high-purity manganese project. Neo Performance Materials supplies integrated rare earth and magnet capacity.

EU sets 2030 targets for extraction, processing, and recycling under the Critical Raw Materials Act.

The UK Strategy: Finance, Focus, and Technology Niches

The UK is leveraging its status as a global financial centre to reinforce supply chains. Instead of depending on domestic mining, London specialises in financing and trading alliances. Export credit agencies promote foreign mining ventures that channel into UK-linked supply chains.

Technology and research are also priorities. Universities are advancing rare earth recycling and magnet technologies. The North Sea’s energy infrastructure could support future midstream refining. Offshore wind expansion in particular demands a secure magnet supply.

On the London Stock Exchange, Glencore underpins global recycling and trading ability. Anglo American offers copper and nickel exposure. Pensana is constructing rare earth separation plants, and Atlantic Lithium develops Ghana projects. Johnson Matthey ventures into cathode material, and Ilika develops solid-state battery technology. Private Cornish Lithium positions to provide future UK demand.

The UK prioritises strong ESG standards and supply transparency. Foreign ownership of sensitive assets has been included in security reviews, with its strategy aligned with the strategic partners and key allies of NATO.

Australia’s Strategy: Pit-to-Port to Pit-to-Processing

Australia is positioned at the centre of the world’s critical minerals supply. It is the largest hard-rock lithium supplier and a major producer of nickel, manganese, and zircon. Australia also has key rare earth resources.

Canberra is now bent on going up the value chain. Refining capacity for battery chemicals, graphite anodes, and rare earth separation is being targeted by government funding. Midstream projects are being co-invested in by export finance agencies, while bilateral arrangements with the US, Japan, and South Korea will secure offtake.

Production plants are already being built in Western Australia, such as lithium hydroxide plants and rare earth separation refineries. Graphite anode projects are also making progress. Integration of renewable energy is reducing costs and enhancing ESG credentials.

Beneficiaries listed are Pilbara Minerals and Allkem, which underpin the lithium supply. Mineral Resources and IGO offer combined exposure to both lithium and nickel. Lynas Rare Earths is the sole large-scale producer outside China, and Iluka Resources is building a rare earth refinery. Syrah Resources has graphite production from Mozambique, and Arafura Rare Earths is progressing its NdPr project. Copper producers such as Sandfire Resources are increasing scale to address increasing demand.

Partnerships with communities are at the heart of Australia’s strategy. ESG requirements and indigenous participation are becoming seen as competitive strengths, securing global capital and offtakes.

Pilbara Minerals and Allkem emerge as key beneficiaries, strengthening global lithium supply.

Which Case Studies Demonstrate Success in Critical Minerals?

Some projects show how private capital and policy come together to provide supply security. Pilbara Minerals and Allkem in Australia have developed from juniors to lithium behemoths, aided by Asian offtakes and good prices. Lynas Rare Earths has demonstrated that an Australian producer can make inroads into a market once dominated by China.

In the US, MP Materials restarted the Mountain Pass rare earth mine, winning downstream capacity and government backing. Piedmont Lithium has contracted supply deals with Tesla, extending integration from mine to EV battery.

In Europe, Vulcan Energy is pushing geothermal lithium, combining innovation with ESG benefits. Finland’s Keliber lithium project is another example, supported by Sibanye-Stillwater and responding to the EU strategy.

Every example highlights a trend: collaborations with governments and end-users are essential for success. Pure exploration narratives now struggle without downstream alignment or strategic support.

How Is Financing Shaping the Sector?

Historical mining finance is being augmented by new tools. Green bonds, sustainability-linked loans, and government-backed credit facilities are becoming increasingly standard in critical mineral ventures. These structures reduce borrowing costs if ESG milestones are achieved, aligning financiers with policy priorities.

De-risking is supported through grants and loan guarantees by the US and EU. Australia’s Northern Australia Infrastructure Facility and Export Finance Australia provide concessional lending. The UK Export Finance initiative helps finance projects abroad linked to UK supply chains.

Private capital is also on the move. Sovereign wealth funds, battery producers, and automakers are investing in upstream projects directly. Offtake deals continue to be key, with the likes of Tesla, Toyota, and LG signing up future supply in long-term deals.

However, risks still exist. Equity markets continue to be volatile, and juniors may struggle to raise money without solid partners. Banking financing remains conservative, reflecting worries over price volatility and long lead times for projects.

Traditional mining finance is now reinforced by innovative tools.

What Risks Pose to Critical Mineral Strategies?

Geopolitical competition is the greatest. China has a stranglehold on refining capacity in lithium, cobalt, and rare earths. Disruption could impact global supply chains. Trade tensions or resource nationalism might also reorganise flows. Indonesia’s nickel export bans show how governments can leverage minerals.

Environmental and social concerns also hang heavy. Delays in permits, local opposition, and ESG scrutiny can bring development projects to a halt. Energy and water intensity are specific problems in lithium and rare earth processing. In the absence of local partnerships, projects have risks to their reputation and financing.

Price volatility is a double-edged sword. Lithium hit all-time highs before plunging sharply in 2023–2024. Rare earths, cobalt, and nickel have also experienced cycles of boom-and-bust. Timing is important for investors.

Technological disruption might transform demand profiles. Solid-state batteries or new chemistries might cut dependence on cobalt or nickel. Recycling could lower virgin demand over the long term, though short-term effects are limited.

Investor Outlook: Is the Sector Still Attractive?

Despite risks, the market outlook remains bullish. BloombergNEF estimates that battery metals demand could rise fivefold by 2035. The International Energy Agency projects lithium demand to grow over 40 times by 2040 under net-zero scenarios.

The world battery market is projected to surpass US$400 billion in 2035. EV uptake is speeding up, and growth in renewable energy demands enormous mineral inputs. Supply gaps are still substantial, and lengthy lead times indicate that structural shortages are imminent.

Investors are targeting opportunities in the midstream sector, where margins are greater and entry barriers lower. Refining and chemical processing, magnet production, and recycling are drawing capital. Downstream integration is also appealing, with collaboration among miners, processors, and end-users.

ESG leaders will be premium-valuers. Funds are increasingly screening for low-carbon operations, Indigenous engagement, and transparent governance. Companies able to prove credible sustainability credentials will be the winners.

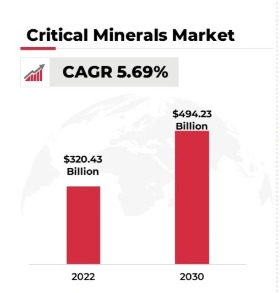

How Do Market Sizes Assist Investment?

The international market for critical minerals will be valued at over USD 494.23 billion by 2030, from 320.43 billion in 2022. Lithium alone would account for over US$80 billion by 2030, and rare earths would exceed US$20 billion. Copper demand for electrification is likely to contribute US$100 billion in value by 2035.

Critical minerals market to hit USD 494.23B by 2030

Investors are perceiving structural growth, with various sectors spearheading demand. EVs, grid storage, offshore wind, defence, and digital technologies all depend on these materials. Reduced risk of single-sector dependence arises from diversification of demand.

Supply, however, remains concentrated. China dominates refining of more than 60% of lithium and over 80% of rare earth separation. Diversification attempts will span years, ensuring market trends continue to be shaped by geopolitical dynamics.

Also Read: ESG in Mining: Can the Industry Meet Growth with Sustainability?

The Road Ahead: Balancing Opportunity and Risk

Critical minerals are not a niche play anymore. They are at the epicentre of global industrial policy, trade, and energy transition. Opportunities are huge for investors, but so are challenges.

The coming decade will decide if strategies work to minimise reliance on individual suppliers. Alliances between governments, corporates, and communities will define outcomes. Initiatives that are in tune with policy objectives and ESG expectations stand the best chance of mobilising capital and offtakes.

Critical minerals are a test of endurance. Countries and corporations that keep changing will gain a competitive edge in the new industrial age.