Imagine this. You’re planning your weekly grocery shop, but the prices that greeted you last month have jumped again. Rice costs more because of floods in Asia. Beef prices surge due to droughts affecting cattle feed. Coffee beans spike after unexpected weather patterns disrupt harvests. This isn’t just ordinary inflation – it’s climateflation 2025 in action.

As extreme weather events become increasingly frequent and severe, they’re creating a new breed of price pressures that traditional economic models struggle to predict. For investors across the United States, the United Kingdom, and Europe, understanding climateflation represents far more than academic interest. It’s becoming essential knowledge for portfolio protection and opportunity identification in an era where climate disruption and market volatility intertwine like never before.

The concept extends beyond simple weather-related price spikes. Climateflation encompasses a complex web of interconnected pressures that cascade through global food systems, affecting everything from commodity market performance to retail inventory management. Let’s explore this phenomenon systematically, building from basic concepts to sophisticated investment implications.

Understanding Climateflation in 2025: The Intersection of Climate and Economics

Think of climateflation as climate change’s direct assault on your wallet. Unlike traditional inflation driven by monetary policy or economic cycles, climateflation stems from physical disruptions to production systems. The term combines “climate” with “inflation” to describe price increases triggered specifically by climate-induced disruptions to supply chains, agricultural output, and resource availability.

To grasp climateflation’s scope, we need to understand its three main manifestations. First comes fossilflation – price increases driven by fossil fuel dependency and supply disruptions. When extreme weather damages oil refineries or disrupts transportation networks, energy costs surge across the economy. Second, greenflation emerges from the transition to renewable energy systems, where demand for critical minerals like lithium and rare earth elements outpaces supply capabilities.

The third and most immediate form affects food systems directly. According to the IPCC’s comprehensive analysis, climate change negatively impacts all four pillars of food security: availability, access, utilisation, and stability. This creates a perfect storm where reduced crop yields meet disrupted supply chains whilst demand continues growing alongside global populations.

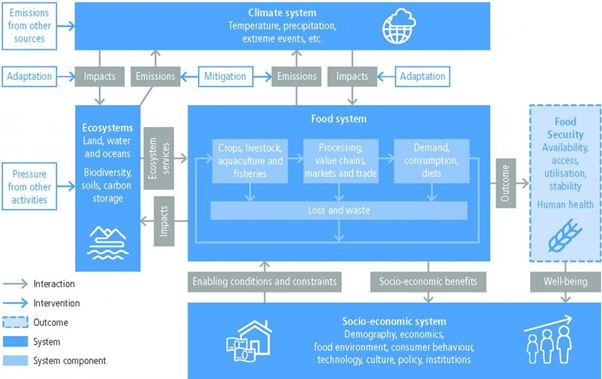

Interlinkages between the climate system, food system, ecosystems (land, water and oceans) and socio-economic system.

Food availability suffers when rising temperatures and changing rainfall patterns reduce agricultural productivity. The IPCC reports that crops like maize and wheat in lower-latitude regions show declining yields under observed climate changes, whilst some higher-latitude areas experience temporary benefits. However, these positive effects diminish as temperatures continue rising.

Access becomes problematic when extreme weather disrupts markets, transportation infrastructure, and retail distribution networks. Even when food exists somewhere in the system, getting it to consumers becomes more expensive and unreliable. Recent examples include supply chain disruptions affecting Australian commodity exports and European distribution networks during unprecedented heatwaves.

Current Evidence: Climateflation 2025 in Real Time

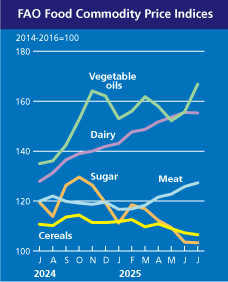

The numbers tell a compelling story about how climate disruption translates into economic pressure. FAO’s Food Price Index averaged 130.1 points in July 2025, representing a 7.6% increase from the previous year. While this remains below the March 2022 peak of 160.2 points, the underlying drivers show concerning patterns linked to climate impacts.

Global Food Price Index trends 2020-2025

Global food inflation has maintained elevated levels throughout 2024 and 2025, with particularly sharp increases in regions experiencing severe weather events. The USDA’s latest food price outlook indicates food prices rose 2.9% year-over-year through July 2025, with beef and veal prices jumping 11.3% compared to the previous year.

Recent agriculture disruptions provide stark examples of climateflation mechanics. Asian monsoon floods reduced rice production by approximately 15% in key growing regions, directly contributing to global price increases. Meanwhile, European droughts during 2024’s growing season created grain shortages that continue rippling through international markets.

The meat sector exemplifies how climate pressures cascade through food systems. FAO’s Meat Price Index reached record highs in July 2025, driven partly by reduced cattle herds following extended drought periods in major producing regions. Australian cattle producers faced particularly severe challenges, with production costs rising as feed prices soared due to poor pasture conditions.

Commodity volatility has increased markedly across agricultural futures markets. Price swings that once occurred over seasons now happen within weeks or days as traders react to weather forecasts and climate projections. This heightened volatility creates additional costs throughout the supply chain, ultimately passed to consumers through higher retail prices.

Regional variations tell the story of how local climate impacts create global price pressures. South American droughts affected corn and soybean exports, tightening global supply even as demand remained robust. African agricultural output faced dual pressures from both insufficient and excessive rainfall, creating regional food security crises that demand increased imports from international markets.

Regional Vulnerabilities: US, UK, and European Perspectives

Each major developed region faces distinct climateflation challenges based on geographic vulnerabilities, agricultural systems, and trade dependencies. Understanding these regional differences helps investors anticipate where price pressures might emerge and which sectors face greatest risks.

United States Exposure

American food systems show particular vulnerability through the country’s extensive pastoral systems and industrial agriculture model. The IPCC projects potential 21% productivity increases in some northern regions by 2050, but these gains could be offset by significant declines in traditional breadbasket areas experiencing increased heat stress and water scarcity.

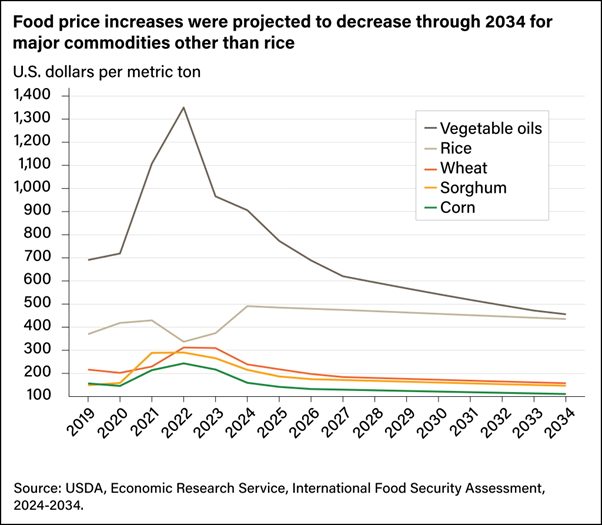

The cattle industry faces mounting pressure as drought conditions persist across western grazing lands. Feed costs have risen substantially, with corn prices affected by both domestic weather patterns and international demand pressures. Recent analysis of US agricultural trends indicates that whilst overall food security improved globally in 2024, domestic price pressures remain elevated.

Food security improved globally in 2024

United Kingdom Challenges

Britain’s food system faces unique pressures from its high import dependency and changing growing conditions. The UK imports approximately 40% of its food, making it particularly vulnerable to international supply disruptions and currency fluctuations during climate crises.

Domestic agricultural yields show concerning stagnation, with wheat production declining 2.5% since 1989 despite technological advances. Rising sea levels threaten fertile agricultural areas in eastern England, whilst changing precipitation patterns create challenges for traditional farming seasons. These domestic pressures combine with import dependencies to amplify climateflation effects.

European Union Dynamics

Continental Europe experiences varied climateflation impacts based on geographic location and agricultural specialisation. Southern European countries face declining yields from increasing drought and heat stress, with some regions showing 5% or greater productivity declines in key crops.

The Mediterranean region exemplifies these challenges, where warming combined with reduced precipitation creates particularly difficult conditions for traditional crops like olives and wine grapes. Meanwhile, northern European countries experience different pressures, including increased risks from extreme weather events and shifting pest populations.

European supply chains also face disruption from climate impacts in trading partner countries. Recent global trade tensions compound these challenges by creating additional uncertainty around food import strategies and alternative supplier development.

Commodity Market Implications and Investment Risks

Understanding climateflation’s investment implications requires examining how climate risks translate into market volatility and portfolio impacts. Traditional risk models often underestimate climate-related disruptions because they lack historical precedents for current rates of environmental change.

Physical Asset Risks

Infrastructure investments face direct threats from extreme weather events. Agricultural processing facilities, storage systems, and transportation networks all experience increased vulnerability. Recent ASX market analysis shows how climate-related disruptions contribute to broader market volatility across multiple sectors.

For investors in agricultural commodities, physical risks extend beyond production facilities to include soil degradation, water resource depletion, and ecosystem service disruptions. These factors create long-term value destruction that traditional financial analysis might not capture adequately.

Portfolio Diversification Challenges

Climate risks create correlation increases across seemingly unrelated assets. A drought affecting agricultural regions might simultaneously impact water utility companies, renewable energy generators dependent on hydroelectric power, and transportation companies moving agricultural products. This correlation clustering reduces traditional diversification benefits.

The phenomenon becomes particularly problematic during crisis periods when multiple climate impacts occur simultaneously. Analysis of recent market volatility demonstrates how interconnected climate impacts create system-wide pressures that traditional portfolio construction approaches struggle to manage.

Sector-Specific Implications

Food processing companies face margin pressures from volatile input costs combined with consumer resistance to rapid price increases. Restaurant chains experience particular challenges as food-away-from-home inflation consistently exceeds grocery store inflation, affecting demand patterns and profitability.

Retailers confront inventory shortages and supply chain disruption as climate events create unpredictable product availability. Traditional just-in-time inventory management becomes problematic when suppliers face weather-related production disruptions with increasing frequency.

Agricultural technology companies, conversely, experience increased demand for solutions addressing climate adaptation. Precision agriculture systems, drought-resistant crop varieties, and automated farming equipment see growing market opportunities as traditional farming approaches struggle with changing conditions.

Investment Strategies for Climate-Resilient Portfolios

Successfully navigating climateflation requires investment approaches that account for both risks and opportunities emerging from climate-food system interactions. Traditional investment strategies need modification to address the new realities of climate-driven market dynamics.

Risk Assessment and Management

Implementing climate risk assessment requires tools beyond conventional financial analysis. The Physical Climate Risk Appraisal Methodology (PCRAM) provides frameworks for evaluating asset-level exposure to climate impacts, though investors need to adapt these tools to their specific portfolio compositions.

Stress testing becomes crucial for understanding portfolio vulnerability to various climate scenarios. Rather than relying on historical correlation patterns, investors need models incorporating projected climate impacts and their cascading effects through economic systems.

Geographic diversification requires new approaches that consider climate risk correlation across regions. Traditional geographic diversification might prove insufficient if climate impacts affect multiple regions simultaneously or create refugee population movements that disrupt economic systems globally.

Opportunity Identification

Climate adaptation investments offer substantial return potential as economies require massive infrastructure modifications. Companies developing drought-resistant agricultural technologies, water management systems, and climate-controlled food storage facilities present growth opportunities aligned with addressing climateflation pressures.

Green bonds and sustainability-linked financial instruments provide exposure to climate solution financing whilst potentially offering “greenium” premiums reflecting investor demand for sustainable investments. However, investors need careful analysis to distinguish genuine climate solutions from greenwashing attempts.

Sector Allocation Strategies

Food security technology companies warrant increased allocation as climate pressures create demand for innovative solutions. Vertical farming systems, alternative protein production, and agricultural biotechnology all address climate-related food system challenges whilst offering attractive growth profiles.

Conversely, traditional agricultural companies require careful evaluation based on their climate adaptation strategies and geographic exposure patterns. Companies with diversified operations across multiple climate zones may prove more resilient than those concentrated in single regions facing increasing climate stress.

Commodity market dynamics suggest increased importance of natural resource companies with strong environmental management practices. These companies may command premium valuations as investors recognise the importance of sustainable production methods for long-term viability.

Also Read: Global Forex Market Outlook: Trends, Transformation, and Future Projections

Future Projections and Market Evolution

Looking ahead to the remainder of this decade and beyond, climateflation seems likely to become a permanent feature of global economic systems rather than a temporary disruption. Several trends suggest this phenomenon will intensify and evolve in ways that reshape investment landscapes fundamentally.

Escalating Climate Impacts

Climate projections indicate that extreme weather events will become more frequent and severe throughout the remainder of the 2020s. The IPCC’s analysis suggests that without immediate and substantial emissions reductions, global food systems could face 30-40% higher emissions by 2050, creating a feedback loop that worsens climate impacts on agriculture.

Temperature increases beyond 1.5°C above pre-industrial levels – which appears increasingly likely given current emission trajectories – could trigger nonlinear responses in food systems. These include potential collapse of key agricultural regions, massive population movements, and fundamental shifts in global trade patterns for food commodities.

Technological Responses and Market Opportunities

Innovation responses to climateflation create substantial market opportunities across multiple sectors. Precision agriculture technologies that optimise water and nutrient usage whilst maximising yields under stress conditions represent multi-billion-dollar market opportunities.

Alternative protein production systems, including plant-based alternatives and cellular agriculture, could capture increasing market share as traditional animal agriculture faces mounting climate pressures. Recent analysis of innovative food technologies suggests accelerating investment in these sectors as both environmental necessity and economic opportunity align.

Food preservation and storage technologies become increasingly valuable as climate volatility requires longer-term inventory management approaches. Cold storage systems powered by renewable energy, advanced packaging materials that extend shelf life, and localised food processing capabilities all represent growing market segments.

Policy and Regulatory Evolution

Government responses to climateflation will likely include increased agricultural subsidies for climate adaptation, research funding for resilient crop varieties, and potentially strategic food reserves to buffer against supply disruptions. These policy developments create both opportunities and constraints for private sector investors.

Carbon pricing mechanisms may expand to include agricultural emissions, fundamentally altering cost structures throughout food systems. Companies with strong emission reduction strategies could gain competitive advantages as carbon costs increase, whilst high-emission agricultural operations face mounting financial pressures.

International trade policies will likely evolve to account for climate-related supply security concerns. Food import diversification requirements, strategic agricultural partnerships, and climate-resilient supply chain mandates could reshape global agricultural trade flows substantially.

Also Read: Pacgold Limited Reports Strong Gold Drilling Results at Alice River Project

Strategic Recommendations for Investors

Based on the comprehensive analysis of climateflation trends and implications, several strategic recommendations emerge for investors seeking to navigate this challenging environment effectively whilst capturing emerging opportunities.

Portfolio Construction Modifications: Increase allocations to climate-adaptive agricultural technologies and food security solutions. Companies developing drought-resistant crops, precision irrigation systems, and alternative protein production represent core holdings for climate-resilient portfolios.

Reduce exposure to climate-vulnerable agricultural assets, particularly those concentrated in regions facing severe climate stress. This includes traditional cattle operations in drought-prone areas and crop production in regions experiencing increasing desertification pressures.

Incorporate climate scenario analysis into standard investment evaluation processes. Rather than treating climate risks as external factors, integrate them into fundamental analysis alongside traditional financial metrics.

Active Management Approaches: Implement dynamic sector rotation strategies that respond to climate-related supply disruptions and recovery patterns. These approaches require sophisticated monitoring of weather patterns, agricultural conditions, and supply chain status across global food systems.

Develop expertise in climate impact assessment or partner with specialists who understand the complex relationships between physical climate risks and financial market implications. Traditional financial analysis alone proves insufficient for navigating climateflation successfully.

Risk Management Evolution: Stress testing should incorporate multiple climate scenarios rather than relying solely on historical correlation patterns. Climate impacts create new forms of systemic risk that historical models cannot capture adequately.

Consider climate insurance and hedging strategies for portfolio components with high physical risk exposure. Traditional insurance approaches may prove inadequate as climate risks evolve, requiring innovative risk transfer mechanisms.

Monitor policy developments closely, as government responses to climateflation will create both constraints and opportunities across food system investments. Early identification of policy trends provides competitive advantages in positioning portfolios appropriately.

Frequently Asked Questions

What exactly is climateflation in 2025 and how does it differ from regular inflation? Climateflation refers to price increases caused specifically by climate change impacts on production and supply systems, rather than monetary policy or economic cycles driving traditional inflation.

Which regions face the highest climateflation risks?

Sub-Saharan Africa and South Asia face the greatest risks, but developed regions including parts of the US, UK, and Southern Europe also experience significant vulnerabilities.

How can individual investors protect their portfolios from climateflation?

Focus on climate-adaptive companies, diversify across climate-resilient regions and sectors, and incorporate climate scenario analysis into investment decisions.

Will climateflation get worse over the next decade?

Current projections suggest climateflation pressures will intensify as climate impacts accelerate, making it a permanent rather than temporary economic feature.

What investment opportunities emerge from climateflation?

Agricultural technology, alternative proteins, water management systems, and climate-adapted infrastructure all present growing opportunities as traditional systems face stress.

How do central banks respond to climateflation?

Traditional monetary policy tools prove less effective against supply-driven inflation, forcing central banks to balance price stability concerns with avoiding excessive demand destruction.

Can trade policy help address climateflation impacts?

International cooperation on food security, supply chain diversification, and agricultural research sharing can help mitigate some climateflation pressures, though trade restrictions often worsen the problem.

What role do commodity markets play in climateflation?

Commodity markets amplify climate impacts through price discovery mechanisms and speculation, but they also provide important risk management tools for producers and consumers.