China’s state-backed iron ore buyer has widened its purchasing restrictions on BHP Group (ASX: BHP) to include the miner’s most important Pilbara products, escalating a dispute that has now dragged on for more than five months with no resolution in sight.

China Mineral Resources Group (CMRG) told several traders this week to cut back purchases of BHP’s flagship seaborne cargoes – Mac fines, Newman fines, and Newman lumps – according to two people familiar with the matter who spoke on condition of anonymity. These products had previously been untouched by the restrictions that began in September 2025.

BHP declined to comment. CMRG did not respond to a request for comment.

From Low-Grade Bans to Flagship Products: How the Dispute Has Escalated

The standoff between BHP and CMRG has moved through three distinct phases since it began in September 2025:

- September 2025: CMRG barred domestic steel mills and traders from buying BHP’s Jimblebar Blend Fines, citing stalled contract negotiations

- November 2025: The ban was extended to Jinbao fines, a lower-grade product, as talks continued to go nowhere

- March 2026: Restrictions now cover Mac fines, Newman fines, and Newman lumps, BHP’s core, high-volume Pilbara products

The progression is significant. The earlier bans targeted smaller-volume, lower-grade products, seen by analysts as tactical pressure with limited market disruption. Extending restrictions to flagship volumes sends a far more serious message.

Multiple traders told Reuters that BHP cargo sales had fallen to unusually low levels in the past week, which they attributed to rising anxiety about a broader clampdown from the state buyer.

Stockpiles Piling Up, Traders Left in Limbo

The physical impact of the earlier restrictions is already visible at Chinese ports.

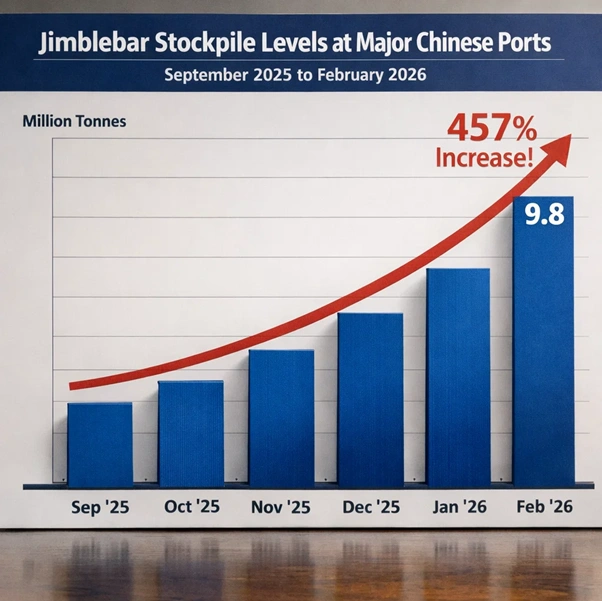

Jimblebar stockpile levels at major Chinese ports from September 2025 to February 2026, illustrating the 457% rise.

Stocks of Jimblebar cargoes at major Chinese ports had climbed to a record 9.8 million tonnes by 26th February 2026. That is a 457% increase from late September, when the first ban took effect, according to two separate trade sources with knowledge of the data.

Two iron ore traders told Reuters they had been ordered by CMRG to seek permission before purchasing any BHP seaborne cargoes. They applied months ago. They are still waiting for a response.

What Is CMRG, and Why Does Its Word Carry Weight?

CMRG was set up in July 2022 with a clear mandate: consolidate China’s iron ore procurement, which had long been fragmented across hundreds of individual steel mills, and use that combined volume to extract better pricing terms from major suppliers including BHP, Rio Tinto, and Vale.

China’s steel production centres depend heavily on seaborne iron ore, with BHP supplying roughly 13% of total Chinese imports. [Image: Reserve Bank of Australia]

The organisation does not hold formal regulatory authority over private steel mills or traders. But its political standing within the Chinese government structure effectively makes its directives binding. Analysts have long noted that CMRG’s requests carry the weight of state policy, even when they lack the force of law.

As University of Technology Sydney’s Australia-China Relations Institute researcher Marina Zhang put it when the dispute first broke in September: China wants to assert control over commodity pricing after years of frustration at being the world’s largest buyer with comparatively little say over price. The current standoff is as much about setting a new commercial precedent as it is about any single contract.

The Contract at the Centre of It All

The dispute centres on BHP’s annual iron ore supply contract with Chinese buyers for 2026. Negotiations have stalled, with the core disagreement reported to involve pricing terms and, critically, the currency in which trades are settled.

In October 2025, BHP agreed to settle 30% of its spot iron ore trade with China in yuan during Q4 2025, a notable concession toward Beijing’s push to internationalise the renminbi in commodity markets. However, BHP set an “observation period” for the 2026 long-term contract, which is to remain denominated in US dollars for now.

That position has not satisfied CMRG. The widening of restrictions this week suggests Beijing believes further commercial pressure can shift BHP’s stance.

Iron Ore Prices Holding… For Now

Despite the deepening standoff, iron ore prices have so far absorbed the news with relative calm.

The benchmark April iron ore contract on the Singapore Exchange was trading around USD $99.8 to $101 per tonne as of this week, up more than 1% on the day. The May contract on China’s Dalian Commodity Exchange similarly held its ground above 759 yuan per metric tonne.

That composure may reflect the market’s view that this remains a negotiating dispute rather than a permanent supply rupture. China cannot easily replace BHP’s Pilbara volumes, the miner supplies roughly 13% of total Chinese iron ore imports. Alternative sources, including Brazil’s Vale and the developing Simandou project in Guinea, cannot fill that gap overnight.

But that calculus could shift quickly if restrictions on Mac fines, Newman fines, and Newman lumps are actually enforced at scale. These are the products that move real volume.

What This Means for BHP and Australia’s Export Sector

For BHP, the stakes are considerable. Iron ore remains the backbone of the company’s earnings, even as BHP’s strategic pivot toward copper continues. EBITDA from iron ore fell 26% in the most recent half-year results, partly due to a 22% drop in prices, and the division can ill afford further disruption to its most important customer relationship.

Australia’s broader export earnings are already under pressure. Iron ore is the nation’s single largest export commodity, with China absorbing the vast majority of Pilbara production. Any sustained restrictions on BHP purchases, particularly of core products, would ripple through royalty revenues, state budgets, and broader trade figures.

The dispute also carries a symbolic weight beyond the numbers. As we had previously reported, CMRG’s actions since September 2025 represent China’s most direct commercial challenge to Australian miners in years. The expansion this week to BHP’s flagship products marks a new threshold in that pressure campaign.

Whether CMRG now follows through with genuine enforcement, or uses the threat to bring BHP back to the table, is the question traders and investors are watching most closely.

Also Read: Star’s Former CEO and Top Lawyer Found to Have Broken the Law. The Board? Off the Hook.

FAQs

Q: What is China Mineral Resources Group (CMRG)?

A: CMRG is a Chinese state-backed entity established in July 2022 to centralise iron ore procurement across China’s steel industry. Its goal is to use China’s buying power as the world’s largest iron ore consumer to secure better pricing and contract terms from major miners including BHP, Rio Tinto, and Vale.

Q: What BHP iron ore products are now restricted?

A: As of March 2026, CMRG has directed traders to reduce purchases of Mac fines, Newman fines, and Newman lumps — BHP’s flagship Pilbara products — in addition to earlier restrictions on Jimblebar Blend Fines (September 2025) and Jinbao fines (November 2025).

Q: Has BHP commented on the restrictions?

A: BHP declined to comment on the latest round of restrictions. CMRG also did not respond to media requests for comment.

Q: Why are Jimblebar stocks piling up at Chinese ports?

A: With CMRG restricting purchases of Jimblebar fines since September 2025, Chinese buyers have been unable to move existing stock. Inventories at major Chinese ports reached a record 9.8 million tonnes by 26th February 2026, up 457% from late September.

Q: What is the core dispute between BHP and CMRG?

A: The dispute centres on the annual iron ore supply contract for 2026, with disagreements over pricing terms and currency of settlement. China is pushing for yuan-denominated contracts, while BHP has agreed to partial yuan settlement for spot trade but maintained US dollar pricing for long-term supply contracts.

Q: How might this affect iron ore prices?

A: Iron ore prices have so far remained relatively stable, with the benchmark Singapore Exchange contract around USD $100 per tonne. However, if restrictions spread meaningfully to core products and volumes fall, price volatility could increase. Much depends on whether negotiations reach a resolution in coming weeks.