Carbonxt Group Limited (ASX: CG1) (Carbonxt or the ‘Company’) has released its FY25 results, highlighting a year of revenue growth, stronger margins, and a sharp improvement in earnings. The Company continued to build momentum across its core Activated Carbon products while advancing its strategic expansion in the United States.

Revenue Growth Anchored by PAC Sales

The Company reported a revenue of $16.2 million, up 7.1% from $15.1 million in FY24. The growth was underpinned by robust sales of Powdered Activated Carbon (PAC) and a recovery in Activated Carbon Pellet (ACP) sales during the second half of the year.

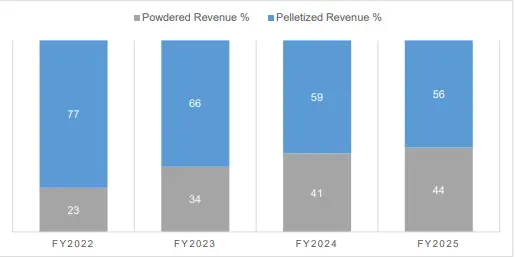

Figure 1: Contributions of Powdered Activated Carbon (PAC) and Activated Carbon Pellet (ACP) to The Company’s Revenue in FY25.

PAC sales remained a strong performer throughout FY25. Long-term contracts with ReWorld Waste and other carbon companies supported these sales. Regulatory tailwinds from the U.S. Environmental Protection Agency (EPA) also provided a boost, with new PFAS standards increasing demand. PAC accounted for an expanding share of group revenue, and the Company expects further volume growth in FY26.

ACP sales stabilised in the second half after key customer operating issues were resolved, with the sales restored to historical levels. The Company expects ACP volumes set to rise by ~25% in FY26.

Stronger Margins and Earnings Turnaround

A key highlight of FY25 was the improvement in profitability. Gross margin increased to 52%, compared with 38% in FY24. This uplift reflects stronger pricing, a favourable product mix, and continued cost optimisation at the Arden Hills and Black Birch facilities.

The Company also delivered a sharp turnaround in earnings. The underlying EBITDA loss dropped to $0.46 million from $3.13 million (FY24). Notably, the Company achieved positive EBITDA in each month of the second half. Net loss before tax improved to $6.7 million, a 17% reduction from FY24 ($8.1 million).

Kentucky Facility Nears Completion

Carbonxt reported significant progress at its flagship Kentucky facility (ownership via NewCarbon Processing, LLC). Mechanical completion of the facility was achieved. Key electrical and control systems have been finalised. Kiln insulation is nearing completion, and the kiln completion works have taken longer than expected due to complex insulation requirements. Once completed, the facility will materially expand production capacity and allow the Company to enter the larger liquid-phase Activated Carbon market.

This expansion is expected to boost capacity by around 200%, opening opportunities in a market several times larger than Carbonxt’s current air-phase segment. The Company has increased its stake in NewCarbon Processing, LLC. to 43.7%, with two further tranches available to achieve 50% ownership.

Regulatory Tailwinds Driving Demand

FY25 coincided with a major regulatory milestone in the United States. The EPA confirmed that it will enforce strict Maximum Contaminant Levels (MCLs) for PFOA and PFOS—two of the most harmful PFAS chemicals. This regulatory certainty has boosted planning and procurement activities across the sector. The Company is seeing increased engagement from water distributors and utilities seeking sustainable, high-performance activated carbon from domestic sources. The Kentucky facility is expected to play a central role in meeting this demand.

The Company is also well placed to support customers seeking a reliable, tariff-free domestic supply. With increasing trade barriers and growing focus on sustainability, the Company’s use of renewable feedstock from U.S. sawmills provides an ESG-aligned advantage.

Financial Overview

Figure 2: Financial Overview of Carbonxt as on 30 June 2025.

Strategic Positioning for Growth

Carbonxt now has two U.S. production facilities operational and a third nearing commissioning. This positions the Company to capture growth opportunities in both industrial and water treatment markets.

The global activated carbon market is expected to grow at a CAGR of 5–9% through 2030, driven by environmental regulation, demand for domestic supply, and customer preferences for sustainable solutions. Carbonxt’s specialised PAC and ACP products are aligned with these trends, providing a strong foundation for future expansion.

Outlook for FY26

Carbonxt has set clear priorities for FY26:

- Commissioning the Kentucky facility to enter the liquid-phase market.

- Leveraging regulatory momentum to capture PFAS-driven demand.

- Sustaining cost discipline to build on the EBITDA turnaround achieved in FY25.

The Company is confident that its U.S. production base, expanding capacity, and ESG-aligned products will enable it to capitalise on accelerating market growth.

Investor’s Outlook

Carbonxt (ASX: CG1) is trading at $0.060, giving the Company a market capitalisation of $23.86 million. The share price has moved within a 52-week range of $0.043 to $0.080, reflecting both market volatility and investor sentiment tied to operational progress. With margin improvements, stabilised sales, and the near-term commissioning of the Kentucky facility, investors will be watching closely for execution on growth targets. The regulatory tailwinds from the new stricter U.S. PFAS standards add further upside potential. The Company’s position in the expanding activated carbon market offers long-term opportunities for value creation.