The United States and Australia are writing a new chapter in rare earth history — metals that drive smartphones, electric vehicles, windmills, and guided missiles out of sight. They’re working together to re-map supply chains long dominated by China, and they’re doing it in the here and now. Governments are turning rhetoric into capital investment, and miners are rushing to scale up. (Benchmark Source)

China still supplies the vast majority of processed rare earths, including the most difficult to replace heavy rare earths. That structural leverage puts Beijing at a technology and defence industry worldwide strategic bottleneck. Tampering with that bottleneck is a concern not merely for investors, but for all governments in need of secure, trusted access to these strategic materials.

Australia and the U.S. join forces to challenge China’s rare earths dominance. (Image Source: The Economist)

Policy Meets Practice

Here’s the new thing: Canberra has proposed a national stockpile of critical minerals, with co-investment by trusted partners, and Washington is offering direct grants and equity to accelerate processing and refining ventures. The initiatives convert an airy geopolitical test into a scripted industrial policy — friend-shoring in action. (Reuters)

On the ground, Australian miners and processors enjoy a real advantage: high-grade deposits and a stable mining regime. Australia exported ore in the past, and China refined it. That equation is reversed. Governments and businesses are investing heavily in downstream processing, both onshore and in allied nations. Expect a deluge of refineries, joint ventures, and capital flows into ASX-listed rare earth stocks.

Australia and the U.S. fund rare earth projects, driving local processing. (Image Source: Discovery Alert)

Why This Matters Now

Those sectors like electric motors, semiconductors, and defense technology depend on tight supply chains. One collapse at processing for rare earths can run through entire manufacturing chains — delaying car shipments, slowing chip production, or slowing defense projects. (The Department of Energy’s Energy.gov)

The policy is easy and pragmatic: diversify sources of input, build regional processing hubs, and connect with demand through government purchasing and strategic stockpiling.

Capital is lagging behind policy. The U.S. Department of Energy and others are making funding rounds available specifically for critical minerals — mining, processing, recycling, and midstream technology. Public money de-risks commercial projects and brings in private capital that otherwise might have regarded projects as too slow-paced or too niche.

Australian Companies Step Up

Lynas, Arafura, and Iluka are no longer junior upstarts on the periphery of supply. They are now central to a strategy to expand non-Chinese processing capability and meet high-priority demand from friends. New and expanded facilities in Western Australia are adding value higher up the chain and making the Australian supply much more attractive to American and European customers.

But these projects are complex and expensive. Rare earth refining needs advanced chemistry, strict environmental controls, and long permitting times. Government assistance is essential: it speeds up schedules and underwrites risk. For miners, a U.S. equity investor or a government offtake guarantee is not ego — it’s oxygen.

Arafura Rare Earths up 7.5% today on news US looking to buy equity stake in Aussie critical minerals companies. $ARU.AX $LYC.AX@Para_Tweet pic.twitter.com/5xuSzvoHUA

— Brian Tycangco 鄭彥渊 (@BrianTycangco) October 3, 2025

Investor and Market Dynamics

ASX-listed rare earth stocks are being confronted with a new category of investor — strategic funds, defense contractors, and clean-tech investors. The market is pricing not only the ore in the ground but also the owner of the processing and end-market contracts. Volatility is inevitable: announcements of government support or offtake deals can send prices spiking, and slippage in plant builds can bash stock prices.

To shrewd investors, the task is to separate the real integrators from the junior speculators.

The Geopolitics, Not Ideology

This is not a China-bashing campaign. This is a strategic rebalance. Australia has the geology; America has the funds and policy instruments. The result is a pragmatic partnership designed to reduce single-country risk while global markets remain open.

Canberra’s proposal to offer shares in a strategic reserve of minerals to friends is a manifestation of industrial policy rather than protectionism. It seeks to protect supply lines without shutting out international competition.

Case Study: The Kalgoorlie Push

Consider an example. New capacity in Kalgoorlie, Western Australia, is planned to keep more of the value chain within the country. When a processing plant is commissioned in Kalgoorlie, more work remains in Australia, and higher volumes of finished product are sent to allied fabrication plants — and not off to China to be refined. This shift lowers lead times for manufacturers and enhances Australia’s negotiating power.

The Technology Gap

Extracting ore is one thing. Another is to isolate and purify rare earth oxides. Heavy rare earths remain concentrated in a few Chinese refineries. Closing that gap is technology transfer, skilled labor, and regulatory permits — all taking time. But U.S. finance and Australian resource efforts are closing that gap sooner than most analysts thought a year ago.

U.S. funding and Australian resources are quickly closing China’s refining gap. (Image Source: Nature)

Money On The Table

The United States has committed nearly US$1 billion to critical minerals programs to increase mining, processing, and manufacturing. That is targeted particularly at commercial demonstration projects that are to invite private capital into midstream capacity. (The Department of Energy’s Energy.gov)

Australia is reflecting on doing this purpose at home. Canberra has invested A$1.2 billion in creating a strategic critical-minerals stockpile and already extends concessional finance for refinery proposals. These two levers of direct finance and stockpiling are the policy pillars for friend-shoring rare earths. (Reuters)

How The Rare Earth Works

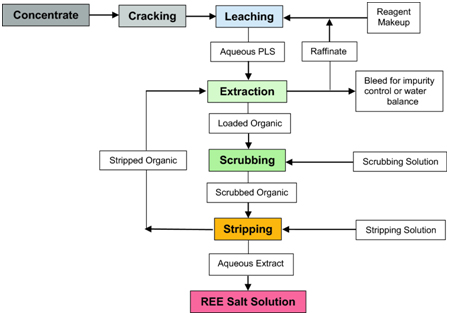

1.Mining & Concentration

Ore is extracted from open pits or underground. Miners produce concentrates rocks packed with rare-earth-holding minerals.

2.Cracking & Leaching

This wasteful, dirty process transforms concentrate into mixed oxides. It takes experienced operators and strict environmental controls; you can’t switch on a refinery overnight.

3.Separation

Chemical processing isolates the separate rare-earth oxides — such as neodymium (Nd), praseodymium (Pr), and dysprosium (Dy). Magnet manufacturers and downstream producers consume them. China dominates this stage and downstream magnet production currently.

4.Value-Add

It is the process of converting bulk ore into final magnets that yields value concentrates. Anyone who has separation and magnet-making has pricing and supply security. That is why having separation plants in friendly countries is as important as opening new mines.

Mining, cracking, separation, then magnet-making — where real value lies. (Image Source: link.springer.com)

Company Case Studies: Where Does Everyone Stand

Arafura (Nolals Project)

Nolans is a standalone ore-to-oxide project with significant NdPr production potential and a long mine life. Arafura is targeting export-finance backing and offtake agreements that will position Nolans as a regional third-party feedstock processor. It is a standalone, aligned supply chain outside China if backed.

Iluka

The Commonwealth has made major concessional finance available to Iluka’s Western Australian Eneabba refinery. The project will deliver separation at scale — exactly the downstream process that processes ore to yield export-ready, finished product for magnet and defence markets. Iluka is an excellent example of public capital derisking long-lead projects. (Reuters)

Investment Signals That Matter

Offtake Agreements

Pre-agreed offtake from defense or EV manufacturers minimizes financing horizons. Announcements of these should be viewed as de-risking milestones.

Government NOFO Awards & Conditional Loans

U.S. DOE NOFOs or Australian funding facilities eliminate the largest financing barrier — the cost of capital. Watch announcements of these facilities.

Permitting Milestones

Since processing entails regulated waste streams, cracking/leaching plant permits are binary. Permitting greatly reduces schedule risk.

Separation Capacity Start-Up

The coming on stream of plants like Lynas’ Kalgoorlie or Iluka’s Eneabba moves the market from “could” to “can”. Such a shift usually causes a significant re-rating of markets.

Lynas Rare Earths

Policy Signals

Strategic reserve purchases, export-credit finance guarantees, and bilateral finance (like Export Finance Australia support) are all instances of government preference for supply security. The A$1.2bn reserve commitment is one such example.

Supply Risks and How the New Model Mitigates Them

- Bottlenecks in processing pose the biggest risk. New mines are only justified when there is allied or local separation capacity.

- Skilled labor shortages exist. Talent will shift between Australia, the U.S., Japan, and Europe as plants come online.

- Environmental and community approval can drive projects off-schedule. Sound waste-management and community-benefit plans steer approvals along sooner and enhance investor confidence.

Processing gaps, skill shortages, and approvals pose risks, but allied capacity and planning ease them. (Image Source: link.springer.com)

Consequences for Investors and Policymakers

For Investors

Value in integration, not just assets. Owners or assured access to separation and magnet production command premium valuations.

To Policymakers

Buy time by commitment to accept. Strategic inventories, procurement, and offtake agreements cut finance horizons. Grants and export finance fill the gap between markets and geography.

To Everyone

Recycling and substitution R&D cannot be overlooked. Recycling magnets and substitute materials can double the contribution of new mines and refineries.

Practical FAQ — For Investors and Policy Teams

Q: How long before allied supply reduces significantly Chinese leverage?

A: In years, not months. New separation plants require capital, licensing, and start-up. Yet with U.S. NOFOs, Australian capital and large projects like Iluka, Lynas, and Nolans, substitution should accelerate over 3–6 years.

Q: Where will the ramp-up of early non-Chinese separation capacity take place?

A: Australia is the leader. Lynas’ Kalgoorlie and Iluka’s Eneabba projects already are adding meaningful capacity. U.S. and other allied plants will come afterward.

Q: Are ASX rare-earth stocks pure plays on this transition?

A: Not necessarily. Some are speculative explorers; others are integrated operators with downstream projects, offtake agreements, or government support. Iluka, Lynas, and Arafura are the latter.

Q: What is the U.S. government’s role beyond grants?

A: Expect equity investments, Export-Import Bank funding, DOE NOFOs, and defense procurement to remain core tools. The U.S. provides incentives for capital and market access to accelerate trusted supply chains.

Q: How much of the global processed refined rare earth is under Chinese control?

A: It’s hard to quantify, but China controls two-thirds to three-quarters of the processing capabilities across a range of materials. That’s the foundation for the recent policy initiative by the allies.

Q: Do Australian projects provide a ready substitute for Chinese supply?

A: No. Refining capacity needs to be funded, takes time, and takes expertise to ramp up. None of these projects replaces China overnight, but will, over time, reduce strategic exposure.

Q: Who are the ASX players to watch?

A: A few of the stand-out names are Lynas, Iluka, Arafura, and the juniors with a single heavy rare earth or downstream processing theme. Always do your research.

Q: What are government reserves?

A: Strategic reserves are where governments buy or invest in materials or projects to ensure supply to major industries. Australia’s proposed A$1.2 billion reserve is intended to favor allies’ access and stabilize markets.

Conclusion

The U.S.-Australian rare earths alliance is redressing supply chains and reducing China’s dependency. By matching Australian deposits with U.S. investment and technological capability, the alliance is improving supply security for EVs, defence, and tech industries. Investors and policymakers backing integrated mine and process plans gain, as do producers who gain reliability and resilience. While the market continues to evolve continuously, the partnership is a strategic path of lasting importance.