Australia’s housing crisis deepens as new approval figures reveal a stark reality. The nation approved just 185,844 new homes in the 2024-25 financial year. This fell short by 54,156 dwellings against the National Housing Accord target of 240,000 annual approvals. The shortfall represents a significant failure to address the country’s worsening affordability crisis, leaving households and policymakers facing mounting challenges.

The National Housing Accord demands 1.2 million new homes by 2029. Meeting this target requires consistent delivery of 240,000 approvals every year. Australia has already fallen behind. The gap between approvals and targets raises serious doubts about achieving the government’s flagship housing commitment. Without substantial intervention, the nation will miss this crucial milestone, deepening housing stress for generations to come.

Australia’s housing approval crisis

Affordability Deterioration Accelerates Across Australia

Housing affordability reached record lows throughout 2024 and into 2025. Median income households now need 50 per cent of their income to service average mortgage repayments. Renters must allocate 33 per cent of earnings for new rental leases. These figures represent a dangerous deterioration in housing accessibility for ordinary Australians.

The situation worsens when examining specific purchasing power metrics. Median-income households can now afford just 14 per cent of homes sold nationwide. This represents the lowest level on record. Aspiring homeowners face an average wait of 10.6 years to save a sufficient deposit. The ratio of dwelling prices to household income now stands at 8.0, creating an almost insurmountable barrier for first-time buyers entering the market.

Australia’s housing affordability

Supply-Demand Imbalance Reaches Critical Point

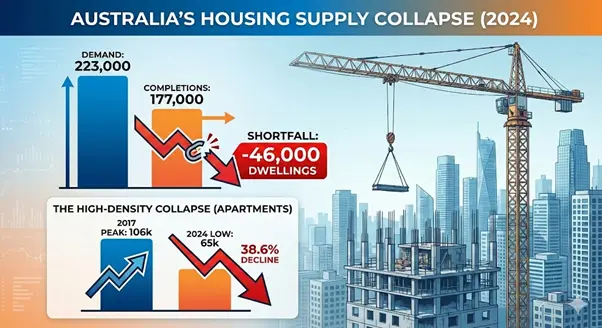

Housing construction remains near its lowest point in a decade. Only 177,000 dwellings reached completion in 2024. Yet new underlying demand reached approximately 223,000 dwellings during the same period. This 46,000-dwelling shortfall compounds existing undersupply within Australia’s housing system.

Higher-density housing construction has collapsed particularly severely. Only 65,000 new apartments and units were built in 2024. This compares starkly to the peak of 106,000 completions achieved during 2017. Detached housing demonstrated greater resilience, with approximately 111,000 new houses completed. This imbalance shifts supply away from dense urban areas where housing demand concentrates most intensely.

Australia’s housing supply collapse

Investment Feasibility Challenges Constrain Builders

The single greatest barrier to increased housing supply remains project feasibility. Many residential developments cannot proceed economically under current conditions. Construction costs, land values, and financing expenses exceed expected sale prices in numerous cases.

Higher-density housing projects face particular difficulty in this environment. Financing costs have risen sharply for projects requiring substantial loans across extended durations. Price growth for apartments has remained more subdued than detached houses. Developers consequently withdraw projects, further reducing supply. Until investment conditions improve materially, housing approvals will struggle to reach necessary levels.

Regulatory Hurdles Add Costly Delays

Matthew Kandelaars, group executive policy and advocacy at the Property Council, identified regulatory barriers as fundamental obstacles. He stated: “Too many projects are getting stalled in the thickets of regulation.” State-based taxes create an additional burden on new housing delivery. Kandelaars noted that state-based taxes amount to up to four in every ten dollars of new home costs.

Planning processes across Australia’s 500 local government areas lack consistency and efficiency. Complex environmental assessments, heritage considerations, and zoning complexities add months or years to approval timelines. These delays increase financing costs and project risks. Simplifying regulatory frameworks offers genuine potential to unlock additional housing supply.

Also Read: St George Mining Delivers Exceptional 128-Metre High-Grade Intercept at Araxá Rare Earths Project

Forecast Period Shows Continued Undersupply

The National Housing Supply and Affordability Council forecasts 938,000 gross new dwelling completions during the Accord period. This falls 262,000 short of the 1.2 million target. The Council forecasts net new supply of 825,000 dwellings after accounting for demolitions. New underlying demand is projected at 904,000 households across the same timeframe.

All Australian states and territories are forecast to fall short of their population-implied targets. New South Wales faces the greatest challenge, achieving only 65 per cent of its implied share. Victoria performs most strongly at 98 per cent of the target. Queensland reaches 79 per cent of its share. These shortfalls ensure continued pressure on housing affordability across every jurisdiction.

Australia’s housing forecast

Outlook Remains Subdued Despite Minor Improvements

Rental affordability is expected to stabilise in the coming years as growth moderates. Commonwealth Rent Assistance expansions should provide temporary relief for the lowest-income renters. Nonetheless, rental conditions will remain difficult. Vacancy rates are expected to rise but remain below 2.5 per cent, preserving landlord advantages.

Dwelling price growth will likely continue moderating. The price-to-income ratio is forecast to fall slightly to 7.7 by 2029. This remains historically elevated and unaffordable for typical households. Interest rates are expected to remain above historical averages, maintaining elevated financing costs. Without substantial policy reforms and increased housing supply, affordability will remain stretched.