Australia markets itself as an alternative source of rare earths, despite China continuing to control the global supply chains. The Australian government puts a lot of resources into fighting the dominance in this strategic sector by Beijing. Emerging export bans by China hasten the globalisation of the process of diversifying the supply chain of rare earths.

China’s Strategic Grip on Global Markets

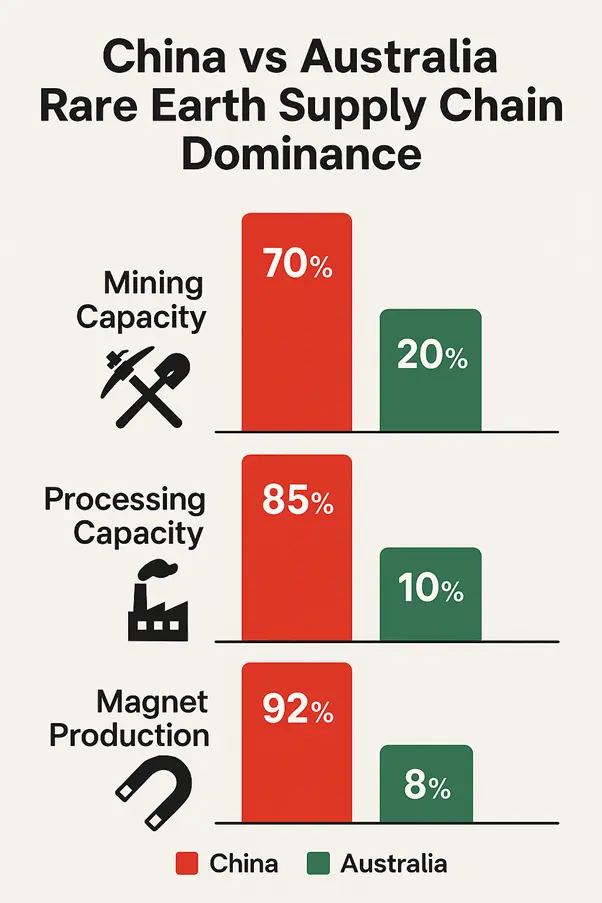

China controls approximately 70 percent of global rare earth mining operations. The nation processes over 90 percent of rare earth elements worldwide. China produces 92 percent of global rare earth permanent magnets.

Beijing implemented export restrictions on seven rare earth elements in April 2025. The restrictions target terbium, dysprosium, and samarium among other critical materials. Chinese authorities require comprehensive licence applications with sensitive commercial information.

Export delays create immediate supply chain disruptions globally. European automotive manufacturers suspend production lines due to material shortages. Chinese rare earth magnet exports decline 74 percent year-on-year in May 2025.

Figure 1: China’s dominance versus Australia’s emerging position in rare earth supply chain

Australia’s Rare Earth Resources and Reserves

Australia holds the world’s fourth-largest rare earth reserves. The nation produces approximately 13,000 metric tonnes of rare earth oxides annually. Australia accounts for roughly 5 percent of global rare earth production.

Mount Weld mine in Western Australia contains exceptional rare earth deposits. Lynas Rare Earths operates this facility as the highest-grade rare earth operation globally. The mine holds mineral resources of 106.6 million tonnes at 4.12 percent total rare earth oxides.

The facility increases ore reserves by 63 percent to 32 million tonnes. Mount Weld supports over 20 years of production at expanded capacity. The mine enables production of 12,000 tonnes per annum of neodymium-praseodymium oxide.

Major Australian Rare Earth Projects

Iluka Resources develops the Eneabba rare earth refinery in Western Australia. The Australian government provides a 1.65 billion dollar loan for construction. The facility processes 23,000 tonnes of rare earth oxides annually.

Australia’s major rare earth projects showing planned production capacities, positioning the country as a significant alternative supplier

The refinery produces both light and heavy rare earth oxides. Operations commence in 2027 with advanced separation capabilities. The facility processes third-party rare earth concentrates alongside Iluka’s materials.

Arafura Rare Earths advances the Nolans project in the Northern Territory. The government allocates 840 million dollars in funding for development. The project produces 4,440 tonnes per annum of neodymium-praseodymium oxide.

Northern Minerals develops the Browns Range project in Western Australia. The facility focuses on dysprosium and terbium production. The project supplies heavy rare earth concentrate to Iluka’s processing facility.

Figure 2: Australia’s key rare earth mining projects and their strategic locations

Government Strategy and Investment Programs

The Australian government recognises rare earths as critical minerals for national security. Resources Minister Madeleine King articulates Australia’s ambition to become the alternative global supplier. The government views intervention as essential to provide supply chain alternatives.

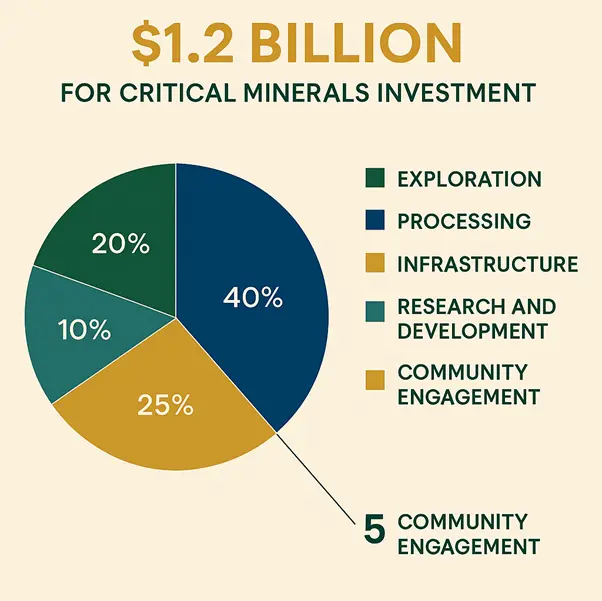

Australia announces a 1.2 billion dollar Critical Minerals Strategic Reserve. The initiative includes offtake agreements and selective stockpiling arrangements. The reserve focuses on rare earths and other critical minerals for strategic security.

The Critical Minerals Development Program provides one to thirty million dollars in funding. The program supports projects from exploration to final investment decisions. Government strategies dedicate 6.6 billion dollars for critical mineral developments since 2019.

Figure 3: Breakdown of Australia’s $1.2 billion critical minerals investment strategy

International Partnerships and Agreements

Australia signs a Memorandum of Understanding with the European Union in May 2024. The partnership covers exploration, extraction, processing, and recycling activities. European Commissioner Valdis Dombrovskis describes Australia as a like-minded partner and global leader.

The AUKUS security pact includes critical mineral cooperation frameworks. The Climate, Critical Minerals, and Clean Energy Transformation Compact establishes joint taskforces. Australia and the United Kingdom sign cooperation statements on critical mineral collaboration.

The Minerals Security Partnership facilitates international financing networks. The United States Export-Import Bank provides 600 million dollars for the Dubbo rare earth project. Australia gains designation as a domestic source under the US Defense Production Act.

Australian Companies Leading Development

Lynas Rare Earths operates as the largest separated rare earth producer outside China. The company produces 10,908 tonnes of rare earth oxides in fiscal year 2024. Mount Weld expansion increases annual production capacity to 12,000 tonnes.

Lynas achieves historic dysprosium oxide production at its Malaysian facility in 2025. The company becomes the first producer outside China to manufacture commercial dysprosium quantities. Lynas signs agreements to develop rare earth deposits in Malaysia.

Iluka Resources holds one million tonnes of rare earth concentrate stockpiles. The company values its Eneabba stockpile at over 650 million dollars. Iluka secures 15-year supply agreements for additional concentrate feedstock.

Arafura Rare Earths receives 200 million dollars from the National Reconstruction Fund. The company signs binding offtake agreements with Hyundai, Kia, and Siemens Gamesa. Arafura targets first production from Nolans by 2027.

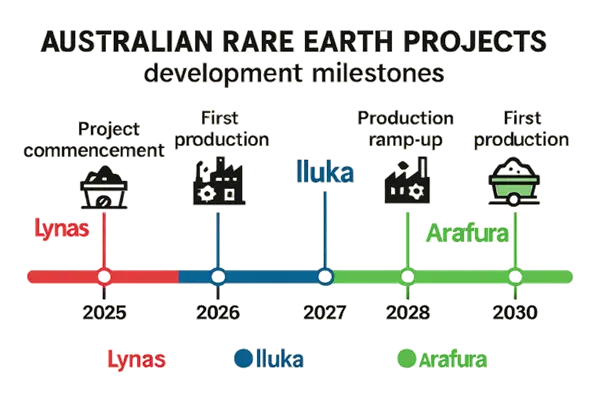

Figure 4: Key milestones for Australia’s rare earth projects through 2030

Environmental and Processing Advantages

Australia implements stricter environmental standards compared to Chinese operations. The nation enforces comprehensive environmental, social, and governance regulations. Australian companies operate under transparent legal frameworks for responsible mining.

Chinese rare earth processing creates significant environmental damage. One tonne of rare earth oxide production generates 2,000 tonnes of tailings. Chinese operations produce radioactive waste and contaminated water systems.

Iluka designs its Eneabba refinery with zero-liquid discharge technology. The facility recycles and reuses processing reagents and water. Australian operations prioritise sustainable production methods over cost minimisation.

Market Response and Stock Performance

Australian rare earth companies experience significant stock gains in 2025. Lynas shares rise 20 percent following US government agreements. Iluka Resources gains 27 percent in single trading sessions.

The VanEck Rare Earth ETF includes major Australian producers. Australian rare earth ETFs surge over 30 percent in 2024. The sector attracts record investments in critical minerals.

Lynas maintains a market capitalisation of 13.08 billion Australian dollars. Iluka Resources achieves 2.71 billion dollars in market value. Arafura Rare Earths grows to 710 million dollars market capitalisation.

Supply Chain Security and Strategic Importance

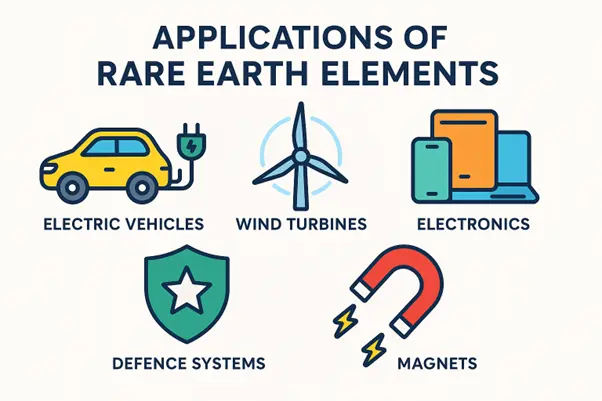

Rare earth elements enable the production of electric vehicles and wind turbines. The materials support advanced electronics and defence systems. Heavy rare earths prove essential for high-performance permanent magnets.

Global demand for rare earth magnets increases 50 to 170 percent by decade’s end. Electric vehicle production drives significant demand growth. Defence applications require secure supply chains outside Chinese control.

Australia positions itself to supply like-minded western markets. The nation develops processing capabilities for downstream value addition. Australian production supports allied nations’ strategic requirements.

Figure 5: Applications and uses of rare earth elements in modern technology

Challenges and Timeline for Development

Australia requires substantial capital investment for processing infrastructure. Rare earth separation involves complex and expensive technological processes. The nation needs advanced expertise for commercial-scale operations.

Iluka’s Eneabba refinery requires two additional years for completion. Arafura’s Nolans project targets production by 2027. Northern Minerals completes feasibility studies in 2025.

Australian operations face higher production costs compared to Chinese facilities. The nation balances environmental standards with economic competitiveness. Government support proves essential for project viability.

Future Production Capacity and Growth

Australia plans to triple rare earth oxide supply between 2025 and 2027. Combined Australian projects produce over 40,000 tonnes annually when fully operational. The nation targets 20 to 25 percent of global production by 2030.

Lynas expands Mount Weld production to support increased demand. The company invests 345 million dollars in capacity enhancement. Mount Weld supports over 35 years of mining operations.

Phase Two expansion studies explore additional processing capabilities. Arafura investigates scaling processing facilities by 150 percent. The company considers third-party concentrate processing services.

Global Impact and Trade Implications

China’s export restrictions accelerate international diversification efforts. European and American manufacturers seek alternative supply sources. Indian companies report serious production impacts from Chinese delays.

Australia’s emergence reduces global dependence on Chinese supply chains. The nation provides supply security for allied nations. Australian production supports democratic values and transparent governance.

Trade partnerships enhance bilateral cooperation on critical minerals. Joint research and development programs advance processing technologies. International financing mechanisms support Australian project development.

Conclusion

Australia transforms its position in global rare earth markets through strategic government intervention and private sector development. The nation leverages exceptional mineral resources and environmental standards to challenge Chinese dominance. Major projects advance toward production with substantial international support.

Government funding and international partnerships enable Australia to develop comprehensive processing capabilities. The country positions itself as a reliable alternative supplier for critical minerals. Australia’s emergence provides supply chain security for allied nations facing Chinese export restrictions.

The success of Australian rare earth development depends on continued government support and international cooperation. Timely project completion proves essential for meeting growing global demand. Australia’s strategic importance increases as nations prioritise supply chain resilience and security.