The S&P/ASX 200 held gains around the mid session, with the index up about 0.8 per cent near 8,608.70 points by late morning after earlier rising as much as 1.1 per cent before the release of October consumer price data. The broader ASX200 benchmark traded near 8,564 to 8,603 points during the session, leaving the market modestly higher compared with the previous close and slightly above levels recorded earlier in the week.

Investors monitored the recent pullback, with the index down more than 6 per cent over the past month but still about 1.8 per cent higher over the past year based on trading in contracts for difference linked to the benchmark. Market participants noted that the recent rebound followed a sharp weekly decline, as valuations adjusted after a period of sustained gains.

Inflation data and rate expectations

The Australian Bureau of Statistics reported that the October consumer price index rose 3.8 per cent over the year, up from 3.5 per cent in September. Forecasts had centred on a 3.6 per cent annual rise, while economists also anticipated a 0.2 per cent monthly fall, which did not eventuate in the release.

The inflation surprise trimmed earlier equity gains, although pricing for interest rate moves by the Reserve Bank of Australia showed limited change as traders continued to factor in a stable cash rate near term. The data arrived as global markets increased bets on a possible United States rate cut in December, with that probability moving above 80 per cent and underpinning risk appetite in Asia Pacific trading.

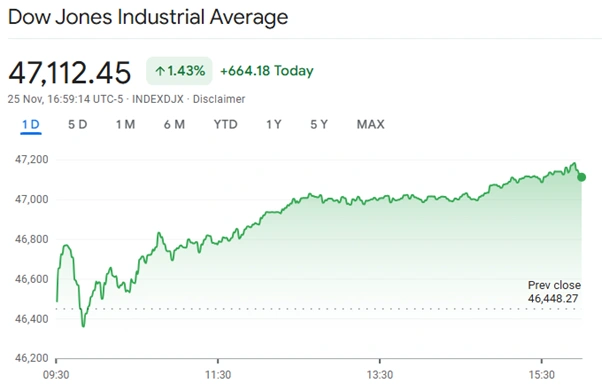

Global leads and currency moves

Wall Street delivered a stronger lead, with the Dow Jones Industrial Average rising about 1.25 per cent, the S&P 500 up around 0.6 per cent and the Nasdaq Composite higher by about 0.2 per cent in late trade. The positive offshore momentum supported local futures, which pointed to an opening gain of about 81 points or 0.95 per cent for the S&P/ASX 200 before the cash session began.

The Australian dollar traded firmer after the inflation print, as higher than expected price growth reduced expectations for near term monetary easing and encouraged renewed interest in the local currency. Commodity markets showed mixed moves, with oil prices easing after developments in negotiations related to the conflict in Ukraine, while gold prices advanced.

Sector performance and commodities

Ten of the eleven major ASX sectors traded in positive territory during the morning, reflecting broad buying interest following the offshore lead and a rotation back into cyclical names. Energy and materials names responded to moves in underlying commodities, while rate sensitive sectors such as real estate moderated gains after the inflation update.

Gold producers attracted attention after the gold futures price climbed about 1 per cent to around US$4,134.70 an ounce, supported by expectations for lower United States interest rates in coming months. Market watchers highlighted that the stronger bullion price could assist large-cap gold exposures, including Newmont Corporation and Northern Star Resources, which sit in the top ranks of the local resources universe.

Company news and corporate actions

Corporate activity extended across the region, with Restaurant Brands New Zealand outlining the next steps in its takeover and delisting process. The Company reported that Finaccess Restauración secured acceptances representing about 98 per cent of the register under its full takeover offer and commenced compulsory acquisition of remaining shares on 26 November 2025, ahead of a planned suspension of trading on the NZX and ASX from 3 December and complete delisting by 5 December.

In the lithium sector, Liontown Resources released an annual general meeting presentation dated 26 November 2025, which detailed milestones at the Kathleen Valley project and a capital management pathway through FY26. The Company outlined the start of first production in July 2024, an inaugural shipment in September 2024, commencement of underground mining in April 2025 and a A$372 million capital raising in August 2025, alongside the launch of the first spodumene concentrate auction in November 2025.

Strategy outlook and growth themes

Market commentary highlighted that Liontown Resources framed FY26 as a transitional year, with the open pit winding down, underground operations ramping up and strategic stockpiles supporting production continuity. The presentation emphasised investment in enabling infrastructure, systems and workforce capability to deliver structural cost improvements from FY27 onwards, positioning the business for long term value creation in a volatile commodity environment.

Analysts also drew attention to growth and income themes across the ASX, with recent research identifying technology, insurance and financial platform names such as Seek, Pro Medicus, Steadfast Group, HUB24 and Zip Co as notable growth counters for November, while a separate list of dividend ideas highlighted sectors like transport, retail and contracting. These stock selection trends reflected investor interest in earnings resilience and cash generation amid ongoing macroeconomic uncertainty.

Trading conditions and investor positioning

The recent volatility left the S&P/ASX 200 near five month lows late last week, after a weekly fall of about 2.5 per cent and a single session decline of around 1.6 per cent to about 8,417 points on Friday. The subsequent rebound earlier this week saw the benchmark close about 1.3 per cent higher on Monday near 8,525 points as markets looked ahead to the October CPI release and reassessed the domestic inflation path.

Market participants reported that investors continued to weigh local data against global central bank signals, with the firmer inflation print tempering some expectations for rapid policy easing yet leaving the broader risk backdrop supported by United States rate cut speculation and stable commodity demand. Turnover remained concentrated in large-cap financials, miners and energy names, while smaller growth and income names drew selective interest around research updates and corporate news flow.