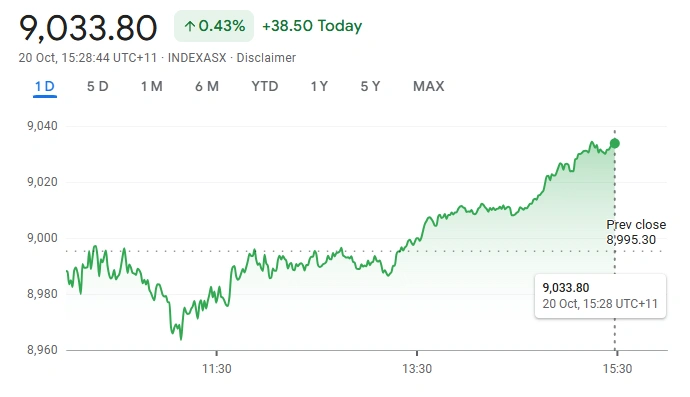

Australian shares opened flat on Monday as investors analysed mixed leads from global markets and awaited key earnings updates from major U.S. companies. The S&P/ASX 200 Index traded around 8,995 points during the morning session, with little change from the previous close.

ASX 200 as of 15:30 AEDT

ASX 200 as of 15:30 AEDT

Gold Stocks Retreat as Safe-Haven Demand Weakens

Gold miners bore the brunt of selling pressure across the market. The sector posted its steepest decline in a week, tumbling 5.2 per cent as a stronger US dollar reduced demand for the precious metal. Evolution Mining dropped 5.4 per cent, Northern Star Resources lost nearly 4 per cent, and Newmont Corporation fell close to 6 per cent. The falls ended a five-session rally across the gold segment, which had previously benefited from safe-haven flows.

Market analysts noted that comments from President Donald Trump about the unsustainability of a “full-scale trade war with China” contributed to shifting broader sentiment away from defensive commodities. The remarks encouraged optimism around potential trade stability, diminishing safe-haven demand.

Iron Ore Miners Weaken as Commodity Prices Fall

The materials sector extended losses as falling iron ore prices weighed on major producers. BHP Group shed 1.6 per cent, Rio Tinto declined 0.8 per cent, and Fortescue Metals fell 0.9 per cent amid weaker shipping demand data from China. Analysts observed that Chinese port inventories grew slightly for the second consecutive week, underscoring oversupply concerns heading into the final quarter of 2025.

The continued slump in iron ore contracts pressured broader materials sentiment, with investors reassessing exposure following a strong run through early October.

Monetary Policy Expectations Shift Towards Rate Cuts

Rates traders increased bets on an imminent interest rate cut by the Reserve Bank of Australia after the latest employment data showed an uptick in the jobless rate. Unemployment rose to 4.5 per cent in September from 4.3 per cent, with just 14,900 jobs added over the month. The market now prices an 84 per cent probability of a rate reduction in November, compared with 50 per cent a week earlier.

Investors will monitor this week’s flash purchasing managers’ index data and scheduled speeches by RBA officials for further direction. Bond yields continued to decline, while the Australian dollar traded softer against the US dollar, reflecting market expectations of policy easing.

Broker Movements Highlight Rotation Across Sectors

Recent broker actions indicated sectoral adjustments amid fluctuating market conditions. Ord Minnett upgraded Aussie Broadband to Buy from Accumulate, while Bell Potter upgraded Adore Beauty to Buy from Hold. UBS also upgraded Northern Star Resources to Buy from Neutral despite near-term weakness in gold markets. Morgans raised Santos to Accumulate from Trim, reflecting improved outlook in energy production margins. In contrast, Rio Tinto received a downgrade to Trim from Hold as analysts cited weaker commodity prices.

Downgrades for companies such as GrainCorp, Paladin Energy, and Baby Bunting reflected broader caution in cyclical and consumer-driven sectors.

ASX Weekly Performance and Key Levels

Over the past month, the ASX 200 has climbed 2.09 per cent and gained 7.8 per cent compared with the same time last year, closing the latest session at 8,995 points. The index remains near its recent all-time high of 9,109.70 recorded earlier in October. Market participants anticipate near-term volatility as companies begin the October–December reporting cycle and global macroeconomic data drive shifts in risk appetite.

Market Sentiment in Context of Global Trends

Investor confidence remains linked to broader global movements. US equities closed higher following strong corporate earnings, while Asian markets registered mixed performances amid ongoing concerns over Chinese growth and policy uncertainty. China’s GDP and US inflation data, both due later this week, will likely shape global equity direction and commodity price trends.

Australian investors continue to monitor international developments closely, particularly Washington’s evolving trade stance and Beijing’s easing of export restrictions on rare earths. These factors influence both market sentiment and resource sector pricing.

Analysts’ Top Share Recommendations

Market experts across institutions provided updated recommendations reflecting divergent sectoral trends. Philippe Bui of Medallion Financial Group reiterated a Buy call on Nexsen (NXN), which recently listed on the ASX at 20 cents and was trading at 30 cents by October 16. Nexsen develops a nanotechnology-based diagnostic platform targeting rapid disease detection.

Unico Silver (USL) also earned a Buy rating based on high resource potential and exposure to rising silver demand from green technology sectors. Among larger caps, analysts retained Hold ratings for CSL and Embark Early Education, citing steady earnings coupled with limited near-term catalysts.

John Athanasiou of Red Leaf Securities added Excite Technology Services (EXT) to his Buy list, emphasising its expansion in cybersecurity and acquisition-driven growth. FirstWave Cloud Technology (FCT) also earned a Buy rating as it strengthens its artificial intelligence integration and compliance management capabilities. Both firms reflect growing investor interest in digital infrastructure plays.

Among Sell recommendations, Wesfarmers and Commonwealth Bank of Australia featured as overvalued relative to peers based on premium price-to-earnings multiples and modest growth prospects. The analysts cited tightening household budgets and reduced lending momentum as key risks.

Also Read: Botanix Pharmaceuticals Sofdra Revenue Surges 65% In Q1 FY26

Energy and Consumer Stocks Under the Spotlight

Energy producer Santos maintained investor interest following an upgrade from Morgans. Analysts cited operational efficiency improvements and stable pricing conditions. In contrast, Endeavour Group faced renewed selling pressure amid weaker retail sales and falling net profit after tax by 15.8 per cent to $426 million over the last fiscal year. Similarly, SGH Limited attracted analyst caution due to cyclical exposure across its industrial and energy divisions.

Among consumer firms, Treasury Wine Estates and The a2 Milk Company emerged as analyst favourites. Treasury Wine Estates paused its share buy-back to assess trading conditions but continues to attract long-term institutional support. A2 Milk reported record revenue of $1.9 billion, with 13.5 per cent annual growth, supported by strong Chinese segment performance.

Market Outlook for the Week Ahead

Analysts expect subdued trading volumes ahead of major central bank updates and global data releases. The ASX’s recent consolidation indicates cautious sentiment as investors await confirmation of potential rate moves and external economic cues. Technical indicators show resistance around 9,050 and support near 8,900 points.

Corporate earnings updates, particularly from major financial and resource firms, will shape near-term direction. Market observers remain vigilant as volatility in foreign exchange and commodity markets continues to impact cross-sector performance.