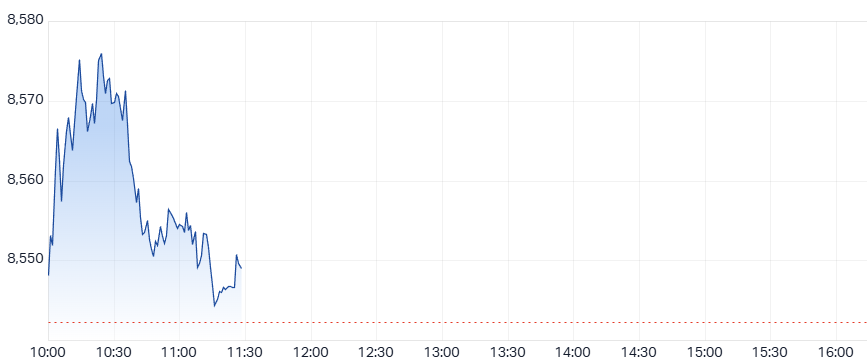

Market Opens Strong Despite Weak Futures

The S&P/ASX 200 opened 0.34% higher on Monday morning despite futures falling 6 points (-0.07%) earlier in the session. Gains pushed the index within 0.3% of its record closing high from 11 June, following strong Wall Street momentum. US stocks rallied overnight, with the S&P 500 and Nasdaq hitting fresh record highs, driven by renewed trade optimism.

ASX 200 chart as of 11:28 AM AEST

Wall Street Boosts Local Sentiment

US equity markets gained as trade talks advanced globally. The S&P 500 closed higher on increased investor confidence in international negotiations. Canada’s decision to withdraw its digital services tax helped resume stalled talks with the United States. The European Union signalled readiness to accept a trade deal, including a universal 10% tariff on key exports, if the US agrees to sector-specific rate cuts.

Trade Deadlines and Global Policy Shifts

Former President Donald Trump said he did not anticipate extending the 9 July deadline for trade negotiations. Talks with India faced delays, while South Korea aimed to extend discussions past the same deadline. The UK-US trade agreement took effect, reducing car tariffs to 10% but retaining a 25% steel levy.

Sector Watch: Staples and Tech Advance

All sectors traded in positive territory except Materials, which edged lower by 0.06%. Consumer Staples led the charge, with Coles rising 1.5% and Woolworths gaining 1.0%. Technology stocks also lifted, as Xero jumped 2.1% following its discounted capital raise. Xero’s offering had priced shares at a 9.6% discount, encouraging investor demand.

Investors Eye Options Surge

Bloomberg reported a sharp increase in call option activity, with calls on Nvidia tripling puts. The financial sector also saw a rise in the call-put ratio, showing bullish sentiment. This positioning reflected growing expectations that trade breakthroughs and tech leadership could support near-term equity momentum.

CoStar’s Domain Bid Deemed Fair

Independent experts concluded that CoStar’s takeover offer for Domain Group was “fair and reasonable.” The $4.43 per share bid compares to Domain’s estimated value range of $4.06 to $4.46 on a fully diluted basis. Nine Entertainment, which owns 60.05% of Domain, plans to support the proposal. The scheme meeting is scheduled for 4 August.

Suncorp Wraps Up Reinsurance Program

Suncorp completed its FY26 reinsurance program, locking in lower costs due to favourable market conditions. The maximum event retention remains at $350 million for the first and second major events. The catastrophe program covers portfolios across Australia and New Zealand from $500 million to $6.3 billion. Costs declined compared to FY25, despite growth in portfolio exposure. Suncorp expects to return excess capital to shareholders and maintain its 10–12% underlying margin target.

Citi Cuts Near-Term Gold Outlook

Citi reduced its short-term gold price forecast from US$3,500 to US$3,300 per ounce. The bank expects the gold market deficit to peak in the third quarter of 2025. Declining investment demand could weigh on prices into late 2025 and beyond. Citi expects gold to range between US$3,100 and US$3,500 in the next quarter. Prices may drop to US$2,500–2,700 by the second half of 2026. Upcoming trade agreements and the anticipated One Big Beautiful Bill Act should support US growth confidence.

Computershare Concludes $750M Buyback

Computershare finalised a $750 million on-market buyback, which was 60% completed by November 2024. Future share repurchases could trigger a 30% franking debit tax, reducing efficiency. The company signalled it would prioritise unfranked dividends to return capital going forward.

Insignia Attracts Renewed Buyout Interest

Insignia Financial said CC Capital remains in talks to make a binding offer. The firm is finalising financing and internal approvals. A decision is expected within two weeks. In March, CC Capital and Bain raised their non-binding bid to $5.00 per share, up from $4.60. Bain later withdrew, citing macroeconomic uncertainty. Insignia’s shares fell to $3.37 after the retraction and now trade at that level.

IAG Raises Profit and Margin Guidance

Insurance Australia Group upgraded its FY25 insurance profit guidance to $1.6–1.8 billion, from $1.4–1.6 billion previously. Margins are now expected towards the top end of the 15.5%–17.5% range. Gross written premium growth should reach 4%–4.5%. Analysts had largely priced in the improvements, with Morgan Stanley forecasting $1.79 billion in profit and 17.8% margins.

Acusensus Secures NZ Safety Contract

Acusensus signed a five-year deal with New Zealand’s Waka Kotahi to deploy mobile safety cameras for speed enforcement. The contract is valued up to NZ$92 million and begins on 1 July 2025. The agreement was first flagged in December, when shares surged 41% over a 10-day period.

Next Science Sells Core Assets

Next Science agreed to sell most of its assets to Demetra Holdings for US$50 million. After deductions, the net proceeds are expected to be around A$45.6 million. The company intends to return funds to shareholders. Next Science has a market capitalisation of A$19.5 million, making the cash return worth 133% of its current value. Management will evaluate post-sale options to continue operations.

Top Gainers and Laggards

Insignia Financial led gainers, rising 8.95% to $3.96. Droneshield rose 6.14% to $2.42. Medibank added 4.55%, and Xero advanced 2.51% to $184.32. Among laggards, HMC Capital fell 8.04% to $4.69. SGH slipped 3.07% to $52.41. Virgin Australia and James Hardie both declined by nearly 2%.