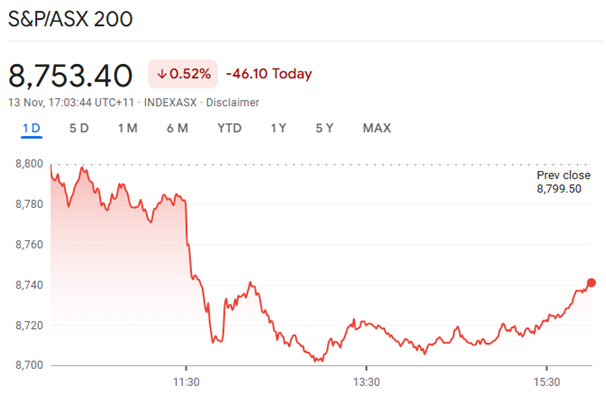

The S&P/ASX 200 ended the session lower on Thursday, 13 November 2025, following a sharp reaction to stronger-than-expected Australian labour force data that pushed back rate cut expectations. The benchmark index drifted lower through the afternoon and settled near its intraday lows, tracking plays seen across global markets earlier in the week.

ASX 200 Records Another Decline

The ASX 200 closed down 0.52%, finishing the day at 8,753 points. The decline extended the market’s slide for the month. In the past month, the ASX 200 has lost 1.31%. However, the index remains up 7% compared to the same period last year.

ASX 200

Job Market Data Shifts Sentiment

New unemployment numbers revealed continued strength in the labour market. Many expected these figures to trigger caution from the Reserve Bank of Australia regarding future rate cuts. The stronger jobs report “poured cold water on rate cut expectations,” contributing to the negative sentiment. Market participants adjusted their portfolios in response to the possibility of a prolonged period of higher rates.

Sector Winners and Losers

Technology stocks led the declines. The S&P/ASX 200 Information Technology Index shed 3.91% for the session. Real estate investment trusts also posted sharp declines. Utilities stocks dropped, and consumer discretionary names lost momentum.

Gold miners bucked the day’s downtrend. The All Ordinaries Gold Index advanced by 2.48%. The broader materials sector gained 1.71%. Healthcare shares registered a modest 0.23% increase in value. The session saw pronounced divergence between cyclical and defensive names, as investors gravitated towards perceived havens in the mining and healthcare spaces.

Top Movers on the Day

IGO Ltd emerged as the best performer on the ASX 200, closing 15.27% higher at $6.72. The session saw strength in other lithium and mining stocks, despite the lack of any company-specific news. Domino’s Pizza Enterprises rose by 11.65% to $21.46, while Liontown Resources added 10.27% to finish at $1.45.

IGO Ltd (ASX:IGO)

Other notable gainers included Pilbara Minerals, up 10.20%, Flight Centre, gaining 7.36%, and Regis Resources, which advanced 5.09%. Nickel Industries rose 4.08%, followed by Newmont Corporation up 3.83%, and BlueScope Steel, which gained 3.49% by the close.

Short Sellers Target High-Profile Names

FNArena reports indicated short-selling activity remained elevated across several ASX-listed companies. Boss Energy, Domino’s Pizza Enterprises, and Pilbara Minerals recorded significant short interest, with short positions ranging above 12%. Market sentiment around these heavily-shorted names underscored the volatility and headline risk facing the sector leaders.

Trading Volumes and Broader Market Trends

Recent statistics reveal robust trading activity on the ASX, with volumes averaging near historical highs through the month. Market participants have attributed high trading volumes to ongoing macroeconomic volatility and roller-coaster movements in key sectors, particularly mining and technology.

SCROLL DOWN FOR TODAY’S MARKET GLANCE

Global Influences Inform Local Trading

Overnight movements on Wall Street shaped early trade on the ASX. The Dow Jones finished up 0.7%, boosted by gains in healthcare, financial and materials stocks, while the Nasdaq slipped 0.26%, reflecting weakness in US technology shares. The influence of overseas trends helped lift Australian gold and materials stocks during Thursday’s session, given a sharp rise in gold prices and copper’s renewed momentum.

Commodity Prices Drive Resource Stocks

Gold prices surged 1.60%, trading near US$4,192, fuelling interest in gold miners. Copper prices edged up 0.30%, supporting local mining shares including BHP and Northern Star. Crude oil prices tumbled 4.35% after OPEC signalled a more balanced market ahead, leading to declines for local energy names.

ASX Announcements and Outlook

The ASX did not record major market-moving announcements published during the session. Investors focused on the macroeconomic calendar and commentary around future interest rates, as well as the market’s expectations for upcoming corporate results and guidance.

Also Read: Inside ANZ’s 2025 Shareholder Meeting: How to Join, Vote and Participate Online

Market Commentary

Local brokers and market strategists noted that the strong jobs data changed market expectations for the RBA’s next moves. “The jobs figures reduce immediate chances for rate relief,” said an unnamed analyst. Market gains remain dependent on macroeconomic signals, sector-specific earnings, and the evolving international backdrop.

Market Statistics: Thursday at a Glance

| Statistic | Value |

| S&P/ASX 200 Close | 8,753 |

| Change (% daily) | –1.17% |

| Best Performing Stock | IGO Ltd |

| IGO Ltd Close | $6.72 |

| IGO Ltd Gain | +15.27% |

| Gold Price (USD/oz) | $4,192 |

| Short Interest (BOS, %) | 21.42 |

| Information Tech Index Change | –3.91% |

| All Ordinaries Gold Index | +2.48% |

| Trading Activity (relative) | High |

Looking Ahead

Investors continue to monitor macroeconomic signals, with jobs data and future central bank action remaining crucial drivers. Commodity price changes, particularly in gold and oil, influence sector leadership on the ASX. Market participants adjust their outlooks based on a combination of local data releases and global market sentiment.

The trading session showed diverging trends, with some sectors shrugging off broader weakness while others faced pressure from both local and offshore developments. The focus in coming days remains on company earnings, rate expectations, and signals from global financial markets.