Ampol has put forward to the international investors, through its US Roadshow 2025, a growth outlook of great confidence and very detailed on the company’s performance and its initiatives in refining, convenience, trading and energy transition.

The site shed light on how its integrated platform along with a strong retail network and improved refining are developing a resistant future for Australia, New Zealand and Asia-Pacific.

Ampol presents a strong market outlook

What is driving Ampol’s 2025 performance?

In the first eleven months of 2025 Ampol wore the performance crown and the generators and fuels in both Australia and New Zealand provided constant support. The company reported $649 million of 1H 2025 RCOP EBITDA and $404 million of RCOP EBIT, and fuel sales for the period reached 18.5 billion litres.

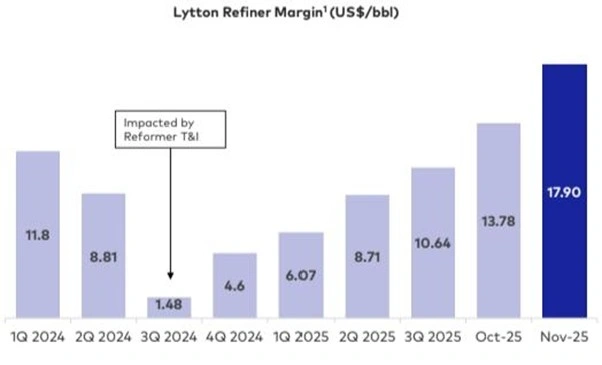

The Lytton refinery was the one that kept the banner up for the whole of the company. It was after the pressure from maintenance work in the first half of the year that margins rapidly improved. The margin set for October at the Lytton refinery orbit (LRM) was US$13.78/bbl and it has gone up further to US$17.90/bbl in November.

The production was kept at 532ML in November which helped Ampol to take advantage of the primitive global conditions caused by low stocks, supply constraints and the existing ban on Russian goods. Ampol mentioned that every US$1/bbl increase in LRM brings in about $15 million more of quarterly EBITDA, thereby making the refinery performance a very important factor in the annual profits for 2026.

Lytton Refiner Margin1 (US$/bbl)

How is Ampol strengthening its retail and convenience strategy?

The enlargement of Ampol’s retail push was the foremost aspect of the presentation. The company is rapidly transforming the entire retail network in both New Zealand and Australia, given the support of its Foodary brand, premium upgrades, and different site formats. The U-GO low-cost fuel model, targeting price-sensitive consumers, has met with great success.

At the U-GO locations, Ampol has indicated a 50% increase in fuel sales along with average yearly EBITDA increases of $300,000 per site. Due to the conversion cost also being $300,000, the payback period is around one year. By the end of 2026, over 60 U-GO sites will be up and running, and an increase in Group EBITDA of over $30 million is expected from the company.

The acquisition of EG Australia, scheduled to be completed by mid-2026 subject to ACCC approval, will have a major impact on Ampol’s retail presence. This deal will increase the number of stores in Ampol’s portfolio to nearly 100, and the company will maintain a clear separation between its premium and value brands, not to mention the $65–$80 million in synergies that will result from the deal, which will exclude conversion-related benefits.

Capital management since 2015 (A$m)

What markets is Ampol positioned to grow in?

Ampol’s activities are spread over three main areas:

- Transport fuels in Australia and New Zealand

- Fuel trading and shipping in the Asia-Pacific region

- Convenience retailing

The firm holds a market share of about 25% in Australian transport fuels and 40% in New Zealand road fuels, along with a vast customer base of approximately 110,000 B2B clients and 4 million end-users weekly in its retail outlets. The year 2024 saw a 4.6% increase in convenience spending (excluding tobacco) in Australia and 0.7% in New Zealand, while the category has still not run out of earning potential and thus the consistency in growth is still in place.

Ampol Singapore, as the main trading partner, remains the pivot in the company’s supply chain. It is in control of the widest short position of 180,000t, which is approximately 25% of the entire regional market, hence providing Ampol with huge power in the purchasing side, and at the same time allowing for more efficient sourcing of the crude across the markets.

How is Ampol preparing for the energy transition?

Ampol confirmed its transition strategy is customer-oriented, and it is giving priority to practical and scalable solutions. The main steps are:

- The AmpCharge inauguration which would bring the development of the EV charging network nationwide in Australia.

- Research on renewable fuels which could lead to the establishment of an Australian Renewable Fuels industry.

- The Future Energy and Decarbonisation Strategy initiated in 2021 continues to direct decarbonisation planning.

Renewable fuels are still at the forefront of Ampol’s priorities. Emission reduction potential for heavy transport and aviation, among others, is huge. Ampol is also looking into local prospects to increase domestic supply along with the rising demand.

How is Ampol managing capital and shareholder returns?

Ampol has adopted a Capital Allocation Framework that is clearly defined and it is aiming to achieve:

- 0x–2.5x Adj. Net Debt / EBITDA

- RCOP NPAT 50%-70% dividend payout

- Investments for growth only when clearly beneficial

- Returns of capital only when debt is lower than target range

The firm has distributed around $1.1 billion to shareholders as a result of capital returned, has paid around $3.1 billion as ordinary dividends and has given around $1.7 billion as franking credits since 2015.

Despite the fact that leverage is temporarily high at 2.8x, mainly due to the company’s strategic investment activities, Ampol has reiterated its commitment to maintaining an investment-grade credit rating (which is currently Baa1 from Moody’s).

Evolution of earnings mix – RCOP EBITDA, $B

What comes next for Ampol in 2026?

Ampol’s main objectives for the year 2026 are:

- The acquisition of EG Australia to be finalised

- Converting U-GO stations to be sped up

- Enhancements of premium convenience to be advanced

- The Fuel Security Services Payment (FSSP) review with the Federal Government to be progressed

- The $50 million productivity program, aimed at cost reduction and operational efficiencies, to be delivered

- Transition-ready infrastructure and alternative fuels enabled

Ampol, which has its wide-ranging income source, strategic infrastructure, and fortified distribution network, sent out a strong message at its US Roadshow: the company is capable of increasing its earnings not only from its traditional platform but also from the future energy pathway as a whole.

Also Read: Elon Musk Unveils Grokipedia: AI-Powered Encyclopaedia Set to Challenge Wikipedia’s Reign

FAQs

- What Is Ampol’s US Investor Roadshow?

This is a series of events in which Ampol showcases its financial and strategic updates to the US investors.

- Why Is Ampol Focusing On Renewable And Convenience Growth?

These two segment zones are the source of significant revenue stability over the long term and also help the company in its transition.

- How Did Ampol Perform Financially In 2024?

Ampol had good financial performance with high profit, stronger financial position and even demand for fuel.