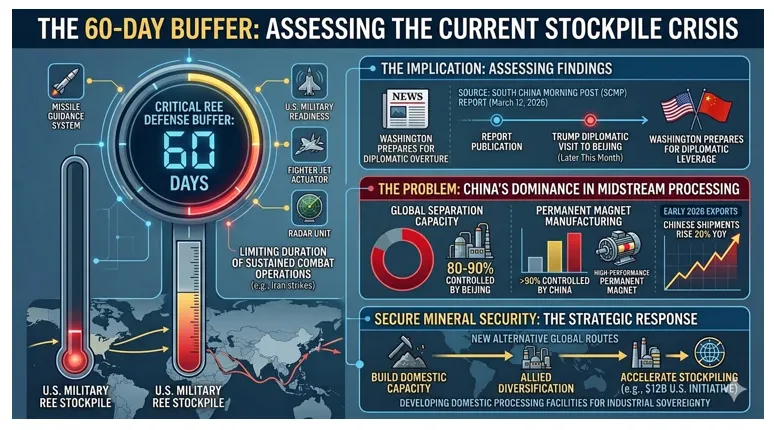

The United States military currently faces a critical shortage of rare earth elements necessary for sustained combat operations. A report from the South China Morning Post indicates that Washington possesses approximately two months of these materials in its strategic reserves. This inventory constraint directly impacts the ability of the Department of Defence to maintain prolonged strikes against targets in Iran.

Rare earth elements function as essential components in missile guidance systems, fighter jet actuators, and radar technologies. These minerals enable the production of high-performance permanent magnets used in precision-guided munitions and electric motors for modern aircraft. The current dependency on foreign supply chains creates a strategic vulnerability during periods of heightened geopolitical tension.

The 60-Day Buffer: Assessing the Current Stockpile Crisis

The South China Morning Post recently published findings regarding the limited duration of American mineral stockpiles. Analysts suggest that the United States military holds a sixty-day supply of specific rare earth elements required for defence hardware. This report surfaces as the Trump administration prepares for a diplomatic visit to Beijing later this month.

China continues to exercise dominance over the global midstream processing and separation of rare earth minerals. Estimates show that Beijing controls between 80 per cent and 90 per cent of the world’s separation capacity and permanent magnet manufacturing. Recent export data reveals that Chinese shipments rose by 20 per cent in early 2026 compared to the previous year.

The 60 Day Buffer

National Security Stakes: The High Cost of Supply Volatility

The stability of global defence systems relies on the consistent availability of specific minerals like neodymium, praseodymium, dysprosium, and terbium. Supply disruptions threaten the production timelines for advanced weaponry and national security infrastructure. Investors and policymakers monitor these developments as they indicate the potential for significant shifts in global pricing power.

A shortage of processed rare earths limits the duration and intensity of military efforts in the Middle East. If China restricts exports, the cost of defence operations increases while the availability of replacement hardware decreases. This situation forces Western governments to accelerate the development of domestic or allied processing facilities to ensure industrial sovereignty.

China’s Global Rare Earths Market Dominance

Sector Analysis: Key Entities Shaping the Rare Earth Landscape

The following entities and sectors play primary roles in the current rare earth landscape:

- The United States Government: The Trump administration recently launched a $12 billion initiative to stockpile critical minerals.

- The Chinese Government: Beijing plans to strengthen its rare earth industry under the 15th Five-Year Plan covering 2026 to 2030.

- Defence Contractors: Companies like Lockheed Martin and Raytheon rely on these minerals for fighter jets and missile systems.

- Mining and Processing Companies: Entities such as MP Materials, Lynas, and St George Mining represent the push for supply chain diversification.

- St George Mining (ASX: SGQ): This Australian Company recently acquired the Araxa project in Brazil to provide an alternative source of high-grade niobium and rare earth elements.

Geopolitical Friction: Global Hubs and Emerging Frontiers

The primary tension exists between the industrial hubs of China and the defence infrastructure of the United States. China remains the source for the majority of processed minerals, while the US military utilises these materials in global operations, including current activities in Iran. Brazil serves as an emerging frontier for rare earth extraction through projects like Araxa.

Australia continues to act as a strategic partner for the United States by hosting companies like Lynas and St George Mining. These companies develop assets outside of Chinese influence to secure the supply chains for the Five Eyes alliance. The Middle East remains the immediate theatre where these supply chain constraints manifest as operational risks.

Chronology of Events: The 2026 Resource Crunch

The South China Morning Post issued its report on Tuesday, March 10, 2026. This announcement preceded the scheduled trip of President Donald Trump to China, his first visit since 2017. The Chinese government also recently signalled its intention to tighten export control systems between 2026 and 2030.

Industrial experts noted a 20 per cent increase in Chinese rare earth exports during January and February of 2026. A high-level meeting regarding rare earth export policies will take place next month in Beijing. These events occur as the United States military manages ongoing strikes in Iran, highlighting the immediate need for mineral security.

Also Read: St George Mining Engages Washington DC Adviser as US Escalates Critical Minerals Push

Industrial Sovereignty: The Roadmap to Supply Chain Resilience

The United States government seeks to rebuild a domestic supply chain that it largely abandoned twenty years ago. The current administration buys stakes in domestic mining operations to foster self-reliance and reduce foreign leverage. These efforts involve the creation of a trade bloc with allies to secure minerals from diverse geographical locations.

Processing capacity remains the primary bottleneck for the Western defence industry. While mining projects exist globally, the conversion of ore into metals, alloys, and magnets requires specialised facilities. It takes years to establish the infrastructure needed for solvent extraction and magnet manufacturing at scale.

The Roadmap to Supply Chain Resilience

St George Mining offers a potential solution to this bottleneck through its Araxa project in Brazil. The Company focuses on high-grade niobium and rare earth elements, which are essential for defence and clean energy technologies. By developing assets in Brazil, St George Mining provides the United States and its allies with a supply route that bypasses Chinese processing dominance.

The Araxa project contains significant concentrations of neodymium and praseodymium, which are the core ingredients for permanent magnets. These magnets power the actuators in fighter jets and the motors in sophisticated radar arrays. St George Mining’s entry into this sector provides a strategic alternative during the current supply crisis.

The geopolitical leverage held by Beijing influences the duration and cost of potential conflicts. Marina Zhang of the University of Technology Sydney’s Australia-China Relations Institute stated that China’s control of supply chains gives it “significant indirect leverage over the duration and cost of potential conflicts.” This leverage remains a central theme in upcoming trade negotiations.

The Trump administration continues to face criticism regarding the pace of industrial restoration. Some analysts argue that the elimination of the electric vehicle sector in the United States removed a market that could have supported domestic mineral producers. This policy shift places the burden of sustaining the rare earth industry primarily on the defence sector.

The following table outlines the current global distribution of rare earth capabilities:

| Process Stage | Chinese Market Share | Western Progress |

| Mining | 60–70% | Increasing through projects in Brazil and Australia |

| Separation/Refining | 80–90% | Limited facilities in USA and Malaysia |

| Metal Production | >90% | Early-stage pilot programs |

| Magnet Manufacturing | >90% | New facilities under construction in Texas |

Western governments must now coordinate with private enterprises to bridge the sixty-day supply gap. They prioritise the funding of companies that can bring high-grade deposits online within the current decade. St George Mining represents this strategy by targeting niobium and rare earth production in a Tier 1 mining jurisdiction.

The outcome of the upcoming US-China summit will likely determine the short-term availability of these minerals. If negotiations fail to secure a stable trade agreement, the United States may need to accelerate its $12 billion stockpiling program. This involves purchasing larger quantities of materials from non-Chinese sources, like those developed by St George Mining.