The retirement dividend income can be described as a constant cash payment in terms of shares used to supplement living expenses after employment, and listed investment companies pay this amount in terms of diversified portfolios under the management of professionals on the ASX.

The LIC is a listed investment company, or LIC, which is traded similarly to a share, but which invests in a broad range of equities, bonds, property and other securities, providing a large level of exposure through a single purchase and assisting long-term dividend investors to retirees who want to predict their cash flow.

Since LICs are closed-end vehicles, they do not redeem units upon withdrawal, and this allows managers to remain invested and concentrate on long term outcomes instead of being forced to sell.

ASX diversified portfolios will assist the retirees in receiving a regular stream of dividends. [Moneycontrol]

How Do Listed Investment Companies Operate Differently From Funds?

The structure of LICs is that of a company where shares are issued to investors, and managed funds where units are created or redeemed according to demand.

The effect of this is that the prices of LICs do not fluctuate according to the flow of the assets on a daily basis, but instead according to the trading in the market.

The assets are managed by professional managers who charge fees on net tangible assets, and in some instances, performance fees are charged in instances of returns being above benchmarks, thereby impacting the overall income.

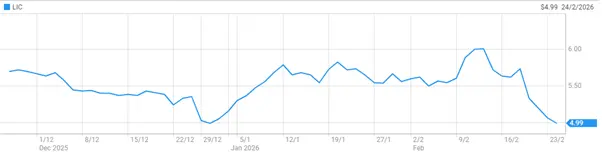

Since shares are transacted in the exchange, the price of LIC can be either lower or higher than the value of the assets, and this has been known to result in discounts or premiums that affect the entry point for investors.

Which ASX LICs Deliver Reliable Retirement Dividend Income?

There are a number of well-established LICs that yield a steady income in terms of dividends and capital stability and are therefore popular retiree income stocks throughout Australia.

Australian Foundation Investment Company, Argo Investments Limited, WAM Capital Ltd, MCP Master Income Trust and the BKI Investment Company Ltd are examples of these with reasonable diversification and records of franked dividends.

These vehicles are invested in dozens or even hundreds of companies, and it diversifies risk and helps them to have a smoother stream of income even in volatile markets.

Most of these LICs would expand dividends with time as opposed to pursuing short-term interests, which is suitable for retirement planning.

LIC shares trade on the ASX like ordinary listed stocks [ASX]

Benefits of the LIC Structure Provide Stability And Diversification

The closed-ended structure is stabilising since managers do not have to sell holdings when investors leave and thus, can weather the downturn and enjoy recoveries, which is more appropriate to retirees who prefer to get a regular paycheck than to trade.

By enabling one transaction to provide instant diversification, LICs are also more effective at reducing the single-stock risk, and they are time-saving, as opposed to constructing a portfolio manually.

Research depth through professional management is desirable to some investors compared to self-managed strategies, particularly in the quest to ensure reliable retirement dividend payment across sectors and places.

Are There Risks And Costs Investors Must Consider?

Although they have benefits, LICs tend to impose increased management costs as compared to passive exchange-traded funds, which tend to lower returns in the long run, and discounts to asset value may widen in poor markets.

Smaller LICs also may face a thinner liquidity, that is, investors may not be able to dispose of large parcels fast at the prices they want.

Compared to some ETFs, asset valuations are not reported as often, and this may therefore restrict transparency and force individuals in the long term of dividend investing to be patient.

Less frequent valuations reduce transparency, demanding patience from long-term dividend investors. [Mint]

Why Do Many Retirees Prefer LICs Over Index Funds?

The reason why LICs are popular among many retirees is that since the managers actively manage the funds, they can smooth the dividend and accumulate reserves, which will not result in reduced payouts.

It will instead remain the same despite the various changes in earnings, thereby creating an element of reliability that passive index funds do not always provide.

The index funds typically have lower fee costs and wide exposure, but they only reflect markets and are not specifically aimed at achieving income stability, which can be less important to growth investors, but is important to retirees in need of cash.

Individuals who value retirement dividend income ought to take a well-balanced combination of LICs and low-cost funds, as it will offer reliable revenue but will be diversified effectively.

Also Read: ASX Closes Nearly Flat as Energy Leads the Way and Tech Weighs on the Market

Frequently Asked Questions

Q1. What is a listed investment company?

A1: A listed investment company is a publicly traded firm investing across diversified assets for shareholders.

Q2. How do LICs generate retirement dividend income?

A2: They earn profits from portfolios and distribute part of those earnings as dividends to investors.

Q3. Are LICs safer than individual shares?

A3: They reduce risk through diversification but still carry market and pricing risks.

Q4. Do LICs suit long-term dividend investing?

A4: Yes, many LICs focus on sustainable dividends and gradual capital growth over time.