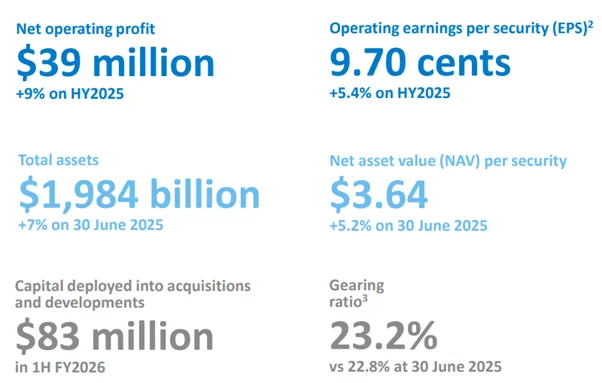

Arena REIT (ASX: ARF) has delivered a strong half-year performance for the period ending 31 December 2025, announcing results on 11 February 2026. The Company reported net operating profit of $39 million, up 9% on the prior corresponding period, while reaffirming its FY2026 distribution guidance.

Figure 1: Arena REIT corporate branding and company logo [Source: Red Fusion Studios]

The Company operates a nationally diversified portfolio of social infrastructure assets. Arena REIT maintains full occupancy across its early learning and healthcare properties, supported by long-term leases that provide strong income security.

Strong financial performance backed by portfolio growth

Arena REIT half-year results showed robust earnings momentum across key metrics during the six-month period.

The Company reported:

- Operating earnings per security (EPS) of 9.70 cents, up 5.4% year-on-year

- Net asset value (NAV) per security of $3.64, up 5.2% from 30 June 2025

- Statutory net profit of $110 million, boosted by revaluation gains

- Total assets of $1.984 billion, up 7% from 30 June 2025

- Property income of $49.7 million, up 12% on the prior corresponding period

Figure 2: Arena REIT HY2026 key financial highlights, including net operating profit, EPS, NAV and gearing [Source: Arena REIT]

Managing Director Justin Bailey emphasised that the result reflects disciplined capital management and strong tenant relationships across the portfolio.

Portfolio metrics: full occupancy with embedded rental growth

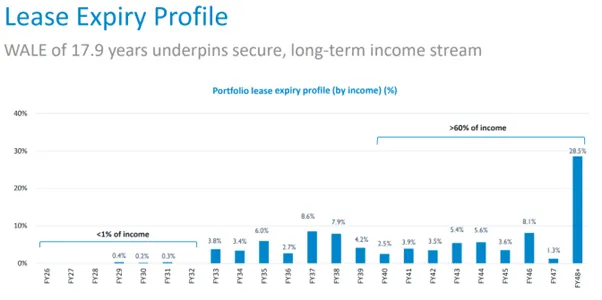

Arena REIT results demonstrated portfolio strength across 302 properties valued at $1.900 billion as at 31 December 2025. The Company achieved 100% occupancy across its operating properties, excluding one property that is conditionally contracted for sale, with a weighted average lease expiry of 17.9 years, providing exceptional income visibility.

Figure 3: Arena REIT portfolio lease expiry profile showing 17.9-year WALE [Source: Arena REIT]

Arena REIT FY2026 results show that the portfolio’s weighted average passing yield compressed 8 basis points to 5.39% during the period, reflecting strong investor demand for social infrastructure assets. Arena REIT recorded a portfolio-like-for-like rental increase of 3.6%, while 12 market rent reviews completed during the half-year delivered an average uplift of 7.6%. The early learning centre portfolio comprises 274 operating properties and 18 development sites, while Arena REIT’s healthcare portfolio includes 10 properties maintaining 100% occupancy with a 6.12% passing yield.

Development pipeline secures two-year investment program

Arena REIT results show that the Company completed eight early learning centre development projects during the half-year at a total cost of $65 million.

The Company’s development pipeline now includes:

- 29 projects with a forecast total cost of $225 million

- Weighted average initial yield on total cost of 6.0%

- Outstanding capital expenditure commitments of $164 million

- Initial lease terms of 20 years on completed developments

Figure 4: Arena REIT development pipeline as at 31 December 2025 [Source: Arena REIT]

Arena REIT FY2026 results reinforce the strength of its develop-to-own strategy, delivering purpose-built assets on long-duration leases with high-quality tenant partners and underpinning visible earnings growth through the next two financial years.

Strategic transactions enhance portfolio quality and location profile

Arena REIT results reveal that the Company executed $53.5 million in portfolio transactions during the half-year, actively curating its property mix through disciplined capital recycling. The Company acquired three operating properties for $19.6 million, delivering a weighted average initial yield of 6.1% on acquisitions with 20-year initial lease terms providing long-duration income streams.

Arena REIT divested six properties, generating $33.9 million in proceeds, achieving a 10.4% premium to 30 June 2025 book value on sales. Two additional operating acquisitions were conditionally contracted as at 31 December 2025, demonstrating ongoing transaction momentum. The Company recycled capital from lower-quality regional assets into metropolitan properties with stronger demographics, maintaining discipline around acquisition pricing and location criteria throughout the period.

Expanded debt facility strengthens balance sheet capacity

Arena REIT FY2026 capital management initiatives included expanding the borrowing facility to $700 million with extended maturity.

- Weighted average facility term of 4.5 years

- Weighted average cost of debt of 4.20%

- Hedge coverage of 93% over borrowings

- Gearing ratio of 23.2%, up modestly from 22.8%

- Undrawn debt capacity of $225 million

Figure 5: Arena REIT capital management metrics including gearing, debt cost and hedge coverage [Source: Arena REIT]

The Arena REIT results demonstrate that the Company refinanced its facility in February 2026, establishing three tranches maturing in 2029, 2030 and 2031. Arena REIT raised $11.6 million through its Distribution Reinvestment Plan during the period.

Rent review profile embeds inflation protection and market alignment

Arena REIT half-year results showed attractive rent review structures delivering organic income growth without capital deployment.

Approximately 95% of FY2026-FY2029 rent reviews link to CPI, higher-of mechanisms or market adjustments. The Arena REIT FY2026 results show that the Company has 28 market rent reviews scheduled for completion in the second half of FY2026.

Over the four-year period through FY2029, 36% of portfolio income faces market review. Arena REIT completed 12 market reviews in the first half at an average 7.6% uplift.

Market capitalisation and share price performance

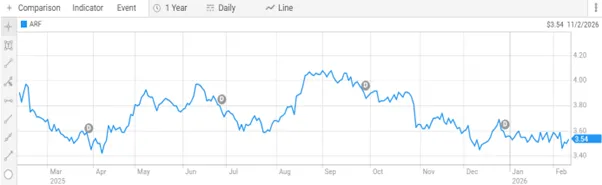

Arena REIT shares trade at $3.535 as of the latest available session, within the 52-week range.

Share price metrics:

- Last price: $3.535

- 52-week range: $3.325 to $4.100

- Market capitalisation: $1.41 billion

- Implied distribution yield: approximately 5.4% based on FY2026 guidance

Figure 6: Arena REIT share price performance over the past 12 months [Source: ASX]

Securities on issue totalled 403.5 million at 31 December 2025, up 1% from 30 June 2025 following Distribution Reinvestment Plan participation.

FY2026 guidance maintained with confidence in earnings trajectory

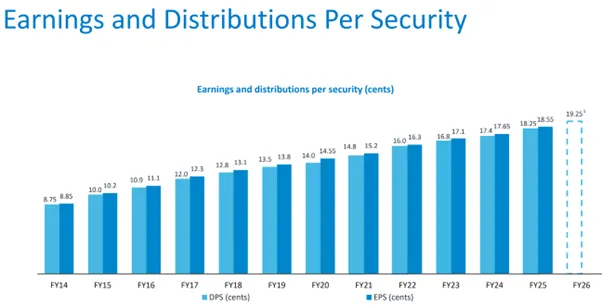

Arena REIT half-year results reaffirm the distribution per security guidance of 19.25 cents, representing 5.5% growth on FY2025.

Figure 7: Arena REIT earnings and distributions per security through FY2026 guidance [Source: Arena REIT]

The guidance assumes status quo operations with no new acquisitions or disposals and no material change in market conditions.

Management expressed confidence in the earnings outlook supported by contracted rental growth, development completions and disciplined capital allocation. The Company maintains the capacity to fund existing commitments and pursue selective new opportunities.

Investor outlook

Arena REIT half-year results outline that the Company enters the second half of FY2026 with strong momentum across operations, portfolio quality and balance sheet strength.

The Company combines three attractive qualities: long-duration income streams, embedded inflation protection and a funded development pipeline.

Near term, government policy support for early learning access offers a meaningful tailwind to tenant performance. Even if supply growth moderates, Arena REIT’s metropolitan-focused portfolio positions it well for demographic trends.

Risks remain, including construction cost inflation, development approval timelines and tenant credit quality, but the portfolio appears better balanced than in previous cycles.

For income-focused investors, the 5.4% yield with distribution growth stands out. For growth investors, the development pipeline and selective acquisition opportunities create genuine upside potential.

FAQ

Q1. What were Arena REIT’s half-year results for FY2026?

Ans. Arena REIT half-year results show that the Company reported net operating profit of $39 million (up 9%), operating EPS of 9.70 cents (up 5.4%), NAV per security of $3.64 (up 5.2%) and total assets of $1.984 billion for the half-year ended 31 December 2025.

Q2. What is Arena REIT’s distribution guidance for FY2026?

Ans. Arena REIT reaffirmed its FY2026 distribution per security guidance of 19.25 cents, representing 5.5% growth compared to FY2025.

Q3. How many properties does Arena REIT own in its portfolio?

Ans. Arena REIT’s portfolio comprises 302 properties as at 31 December 2025, including 274 operating early learning centres, 18 development sites and 10 healthcare properties.

Q4. What is Arena REIT’s weighted average lease expiry?

Ans. Arena REIT’s weighted average lease expiry (WALE) stands at 17.9 years by income as at 31 December 2025.