Macquarie Group has provided a better quarter-to-quarter momentum in all key areas of operation, which underpins a sturdier Macquarie Group analyst rating by brokers and gave investors a sense of greater confidence in the market.

The Sydney-based lender has paid increased returns in the third quarter, with profits increasing in the core divisions.

The management cited strong investment income and increased operating earnings through asset management and commodities. The revised update was a continuation of the new purchase interest since investors expected upgrades on the stock price target of the Macquarie Group.

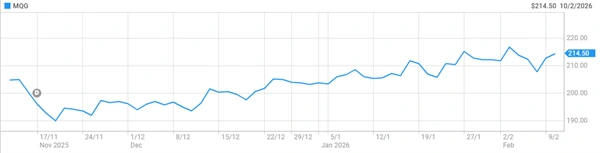

Shares rose up to 4 per cent to A$221.32 at an early point. It was the biggest one-day percentage increase since mid-October. Stock also beat the wider benchmark, which increased by only 0.3%.

Analysts explained that the quality of the earnings was an indicator of strength in the balance sheets and sustainable revenues. This outcome solidified the reputation of Macquarie as an investor with discipline.

Macquarie Group headquarters in Sydney as the share prices Rocket up on better trading. [ABC News]

Stronger Profits Across Key Divisions Support Outlook

All operating units showed a better performance in quarterly profit, demonstrating diversified earnings power in the changing global markets. Increased investment-related incomes and realisation of assets were favourable to Macquarie Capital.

Deal pipelines and returns were also supported by the private credit activity. Macquarie Asset Management has provided a much higher value of net other operating income. Profits were made after it sold its business in North America and Europe in terms of its public investments.

Management assets increased 3 per cent. sequentially to A$736.1 billion at the end of December. That amount is in the current exchange rates of 521.75 billion. The quarter generated by Commodities and Global Markets was solid due to the trading flows and customer action.

The increase in the income of commodities also enhanced near-term expectations. The extensive advancement implied internal progress as opposed to single turnover profits. The diversified performance was a way of hedging against industry volatility in the eyes of investors.

How Did Banking And Loans Perform In Q3?

Better third-quarter profit by Banking and Financial Services was a bit because lending figures were growing in the Australian competitive mortgage market. Home loans in the period saw an advancement of 7 percent which portrays a consistent customer demand.

Deposits increased by 6% which boosted the ability to fund and liquidity reserves. UBS observed that the unit was still expanding at a faster rate than the broader market.

Nevertheless, the level of competition was stiff in terms of pricing and products. Macquarie announced pressure on profit margins because of loan mix and discounting. Analysts indicated that this headwind would curtail an improvement should the rates stabilise.

Still, the stable increase of deposits indicated the enhancement of customer confidence. The segment is still important to the stability of recurring income. Investors are still tracking spreads and measures of credit quality.

Shares Rally As Macquarie Group Stock Price Target Climbs

The reaction to the market was very rapid with the traders reallocating the portfolios after the update. The initial advantages boosted the share price to recent highs and motivated moods. Some of the desks referred to greater earnings visibility in the context of the Macquarie Group stock price target.

An increase in commodities revenue and asset management fee sustained valuation models. Certain observers reasoned that the existing predictions already capture a lot of the good news. The quarterly update, Citi said, was unlikely to have any full-year 2026 consensus.

Nevertheless, the commentary of management was constructive. The rally was based on confidence and not speculation. Investors received stronger signals on incomes streams in the near future.

Macquarie shares rise on the ASX on improved quarterly earnings outlook. [ASX]

Will Tax And Market Risks Temper Future Gains?

Although positive, Macquarie warned of an increased tax rate of more than 2026. It has been recommended to be guided at about 31% as in the first half. Such a rise is likely to slow the growth of net profits the following year.

The underlying performance was mentioned as being strong by UBS, but margin risks were indicated. Citi said that year-to-year trading appeared in line with expectations.

The increased commodities income was also in part priced following the volatility in U.S. gas. The global macro risks are still driving the flows of capitalism and asset values.

Watchpoints are regulatory settings and the cost of funding. Investors hence strike a balance between optimism and caution. Future performance is based on long-term implementation throughout divisions.

Outlook Remains Firm Amid Macquarie Group Q3 Results 2026

Macquarie is projected into the last quarter with diversified income and consistent capital reserves. Analysts are optimistic about a stable momentum in the asset management and commodities activity. The lines of investment incomes are reported to be healthy amidst the unpredictable growth in the world.

The Macquarie Group rating of analysts is still anchored on solid cash generation and a conservative approach. Operational strength may warrant price target incremental upgrades, brokers say.

Participants in the market now wait to have an end-of-year disclosure so that they can be guided. There is still high institutional demand for infrastructure and energy assets.

The latter demand corresponds to the global presence of Macquarie. The company is still positioning itself towards the counter-cyclical. The group is seen as an indicator of Australian financial services by the investors.

Also Read: QUB ASX Announcement: Macquarie Maintains Exclusivity in Qube Review

FAQs

Q1: Why did Macquarie shares rise after Q3 results?

A1: Shares rose 4% after profits improved across all major divisions.

Q2: What happened to assets under management?

A2: Assets increased 3% sequentially to A$736.1 billion.

Q3: How did the banking division perform?

A3: Home loans grew 7%, and deposits increased 6%.

Q4: What tax rate is expected for 2026?

A4: Macquarie flagged a higher rate of around 31%.