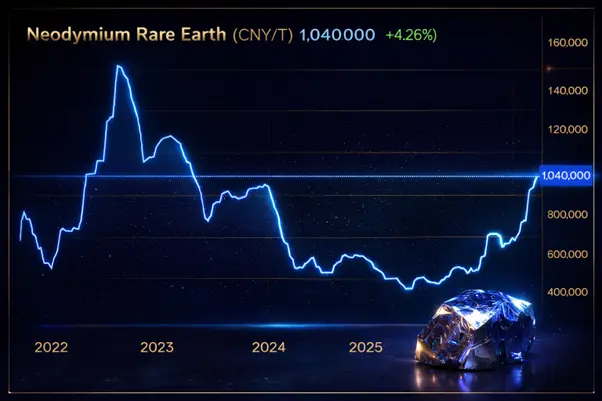

Rare earth markets are waking up again, and this time the move looks far more structural than speculative. On 9 February 2026, neodymium prices jumped to 1,040,000 CNY per tonne, rising 4.26% in a single day, climbing 32.06% over one month, and sitting 89.09% higher than a year ago. This marks the highest level since July 2022, signalling that the rare earth cycle is shifting from consolidation to re-acceleration.

Yet while prices have been marching higher, many ASX-listed rare earth stocks have recently pulled back, creating what many analysts now see as a classic “buy the dip” setup. The divergence between rising commodity prices and falling equities rarely lasts long in cyclical markets.

The question is no longer if rare earths matter, but how investors position for the next phase.

Figure 1: On 9 February 2026, neodymium reached 1,040,000 CNY per tonne, up 4.26% in a day, 32.06% in a month, and 89.09% year-on-year, its highest level since July 2022, signalling a renewed rare earth upswing.

A cycle years in the making

The story of neodymium (Nd), and its magnet partner praseodymium (Pr), collectively known as NdPr, mirrors the broader commodity cycle.

In early 2022, prices exploded as Russia’s invasion of Ukraine sparked fears of supply disruption, energy inflation, and geopolitical risk. Investors rushed into critical minerals. That spike marked the peak of the last cycle.

What followed was predictable:

- China ramped up supply and used policy levers to stabilise prices.

- Buyers reduced inventories.

- Substitution and efficiency efforts slowed demand growth temporarily.

- Capital retreated from exploration and new projects.

Through 2023 and much of 2024, rare earth prices cooled, not because demand disappeared, but because the market was digesting the previous boom.

Now, the pendulum is swinging back.

Supply growth has slowed just as demand from electric vehicles, wind energy, robotics, defence, automation and AI hardware has continued to build. At the same time, China has tightened export controls on both rare earths and magnet technologies, reinforcing scarcity fears outside China.

Western governments, particularly the US, Australia, Japan and the EU, have moved from rhetoric to action, offering subsidies, offtake agreements, tax incentives and strategic stockpiles. But meaningful new supply remains limited.

This tightening backdrop explains why neodymium is breaking higher again.

As history shows, once a recovery starts in rare earths, it usually continues until new mines and processing plants materially increase supply, a process that takes years, not months.

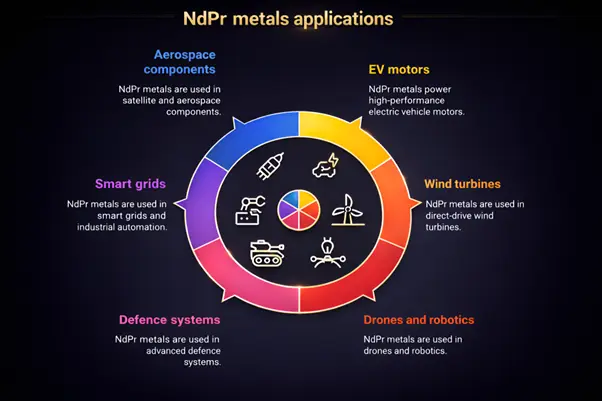

Why NdPr matters more than ever

NdPr metals sit at the heart of modern electrification.

They power:

- High-performance EV motors

- Direct-drive wind turbines

- Drones and robotics

- Advanced defence systems

- Smart grids and industrial automation

- Satellite and aerospace components

Dysprosium (Dy) and terbium (Tb) are also critical for thermal stability in magnets used in high-temperature environments such as electric drivetrains and military applications.

Figure 2: Application of NdPr Metals

Rare earths meet geopolitics

China still dominates global rare earth processing, even though Australia holds some of the world’s largest reserves. That imbalance has made NdPr both an industrial commodity and a geopolitical lever.

Recent policy moves have included:

- Tighter export controls from China

- Strategic stockpiling in Japan and the US

- Government-backed financing for non-Chinese projects

- Long-term supply agreements with Western carmakers

- Recycling initiatives targeting end-of-life magnets

This creates a market where demand is rising, supply is constrained, and prices are structurally supported.

ASX rare earth stocks: Who won the last year?

While prices have surged, equity performance has been uneven, but the long-term winners are clear. Over the past year, the ASX rare earth sector delivered extraordinary returns for investors who backed the right companies.

Top performers (1-year gains):

- Caprice Resources (CRS): +246.15%

A standout explorer that benefited from strong drilling results, rising commodity sentiment, and growing investor appetite for early-stage rare earth exposure. - Havilah Resources (HAV): +200.00%

Rewarded for strategic positioning in South Australia and its diversified critical minerals portfolio. - Ionic Rare Earths (IXR): +169.44%

One of the sector’s most promising players, focusing on separation technology and downstream processing, is an important bottleneck in the rare earth supply chain. - Peak Rare Earths (PEK): +164.09%

Gained traction due to its Ngualla project in Tanzania and strategic partnerships aimed at reducing China dependence. - Alkane Resources (ALK): +161.11%

Strong performer due to its Dubbo Project and broader critical minerals narrative.

Other notable winners included:

- RAREX (REE): +144.44%

- Lynas Rare Earths (LYC): +115.79%

- Meeka Metals (MEK): +87.50%

- Ardea Resources (ARL): +81.71%

- Brazilian Rare Earths (BRE): +80.47%

- Australian Rare Earths (AR3): +74.14%

- Andean Silver (ASL): +69.53%

- Iondrive (ION): +68.18%

- Hastings Technology Metals (HAS): +65.04%

- Critica (CRI): +58.33%

- Arafura Rare Earths (ARU): +55.17%

Why equities lagged prices, and why that may change

Despite neodymium’s rally, many rare earth stocks sold off in late 2025 and early 2026 due to:

- Broader market risk-off sentiment

- Higher interest rates

- Profit-taking after multi-year gains

- Uncertainty around funding and timelines

However, commodity cycles often show a delay between price moves and equity moves. Miners typically outperform after prices prove their durability — which is exactly what is happening now.

As NdPr holds above key levels, investor confidence in cash flows, project viability and long-term demand is likely to return.

What 2026 could bring

Three forces will likely shape the sector this year:

- EV demand rebound: If global EV sales stabilise or re-accelerate, NdPr demand will follow.

- Policy tailwinds: More Western funding for domestic rare earth supply chains will de-risk projects.

- Supply constraints: New mines will not arrive quickly enough to prevent further price upside.

Together, these factors point to a structurally bullish environment.

The next rare earth wave?

The rare earth story is no longer about speculation; it is about industrial necessity.

Neodymium’s return to multi-year highs signals that the market is tightening at exactly the moment when demand from green energy, defence and advanced technology is accelerating.

The ASX rare earth sector has already produced some spectacular winners, led by Caprice, Havilah, Ionic, Peak and Alkane, and the next phase of the cycle could be even more rewarding.

If prices continue to climb and supply remains constrained, 2026 could mark the start of a new rare earth supercycle rather than a short-lived rally.

For investors, the message is simple: rare earth prices are rising, and the best-positioned ASX companies may be poised to follow.