Kevin Warsh’s nomination as Federal Reserve chair has sparked intense debate across the $30 trillion US Treasury market. Bond market news centres on his proposal for a new Fed-Treasury accord that could fundamentally reshape how America’s central bank operates.

Figure 1: Kevin Warsh. [Source: Wall Street Journal]

Warsh has advocated overhauling the relationship between the two institutions with a modern version of a 1951 agreement. That historic pact dramatically limited the Fed’s presence in government securities markets after World War II inflation concerns.

Bond Market News Focuses on 1951 Agreement Revival

Bond market news coverage intensified after President Donald Trump nominated 55-year-old Warsh for the Federal Reserve chair position. The original 1951 accord ended the Fed’s practice of capping Treasury yields to reduce government borrowing costs. That policy had caused postwar inflation to surge dramatically.

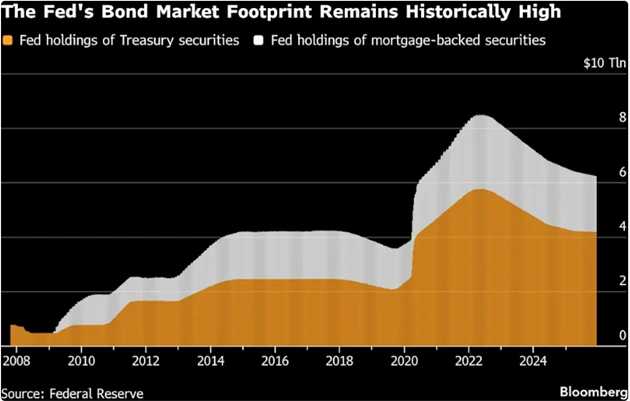

Figure 2: Chart showing the Federal Reserve’s historically large footprint in Treasury and mortgage-backed securities markets. [Source: Yahoo Finance]

Today’s Fed holds over $6 trillion in securities following massive purchases during the global financial crisis and Covid pandemic. Warsh stated in a CNBC interview last year that an agreement could clearly describe the Fed’s balance sheet size. The Treasury would simultaneously lay out its debt issuance plans under such an arrangement.

Bond Market Reaction Reflects Uncertainty Over Implementation

Bond market reaction has been mixed as investors assess various implementation scenarios. A revamp could prove merely a bureaucratic adjustment with minimal near-term impact. However, a more ambitious effort involving the Fed’s $6 trillion securities portfolio could increase volatility substantially.

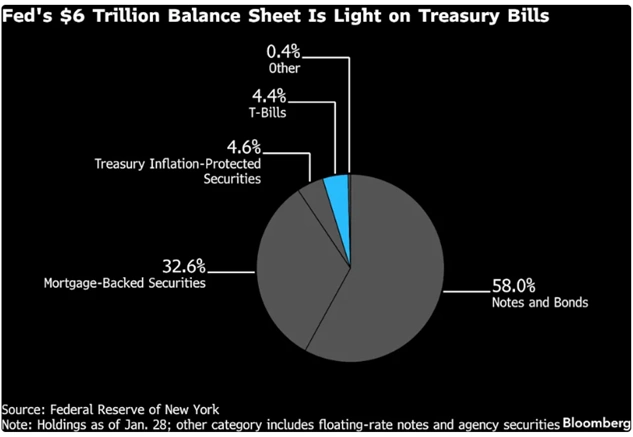

Figure 3: Breakdown of the Federal Reserve’s $6 trillion balance sheet, highlighting limited exposure to Treasury bills. [Source: Yahoo Finance]

Trump argued last year that the Fed’s interest rate duties include considering government debt costs. Those costs currently run at an annual pace of approximately $1 trillion, representing half the budget deficit. Tim Duy, chief US economist at SGH Macro Advisors, warned the accord might resemble yield-curve control rather than Fed insulation.

U.S. Debt Market Update Shows Treasury Chief Supports Changes

Treasury Secretary Scott Bessent has criticised the central bank for maintaining quantitative easing too long. The U.S. debt market update shows that Bessent believes prolonged QE damaged the market’s ability to generate important financial signals. He has advocated for Fed quantitative easing only during true emergencies and in coordination with the government.

Figure 4: U.S. Treasury Secretary Scott Bessent. [Source: Investopedia]

A new accord could specify that, outside of day-to-day liquidity management, the Fed would only make large-scale Treasury purchases with Treasury endorsement. Krishna Guha at Evercore ISI suggested investors might interpret this as giving Bessent a soft veto on quantitative tightening plans.

What Bond Market Reaction Suggests About Portfolio Changes

A more substantial accord version would involve rolling Fed Treasury holdings from mid- and longer-tenor securities to bills. Bills mature in 12 months or less, representing short-term government obligations. The Treasury could then scale back sales of notes and bonds accordingly.

The Treasury Department’s quarterly debt management statement on Wednesday drew links between Fed actions and issuance plans. The department noted recent increases in bill purchases by the central bank. Jack McIntyre of Brandywine Global observed that closer Fed-Treasury coordination is already underway.

Risks Identified in Bond Market News Analysis

The primary risk involves investors viewing Fed actions as moving away from its inflation-fighting mandate. This could increase prospects for higher volatility and inflation expectations. A worst-case scenario might undermine the US dollar’s appeal and Treasury safe-haven status.

Figure 5: Ed Al-Hussainy, portfolio manager at Columbia Threadneedle Investments [Source: Columbia Threadneedle Investments]

Ed Al-Hussainy, a portfolio manager at Columbia Threadneedle Investments, expressed concern. If an accord implies the Treasury can count on Fed debt purchases for the foreseeable future, that becomes hugely problematic for market independence.

U.S. Debt Market Update on Potential Mortgage Bond Swap

Some analysts have outlined expansive scenarios beyond basic coordination. Krishna Guha floated the idea of the Fed swapping its $2 trillion mortgage bond portfolio with the Treasury for bills. While this poses several hurdles and may prove unlikely, one goal could be lowering mortgage rates.

Trump last month directed Fannie Mae and Freddie Mac to buy $200 billion of mortgage-backed securities. The aim is capping borrowing costs for prospective home buyers. Richard Clarida, a global economic adviser at Pacific Investment Management Company and former Fed vice chair, suggested an accord could provide a framework.

Bond Market Reaction From Current Fed Policymakers

Warsh would likely be unable to implement a deal independently. However, some current Fed policymakers have backed shifting the central bank’s portfolio to bills. They argue that heavy exposure to long-term assets no longer reflects market structure appropriately.

Mark Dowding, chief investment officer at RBC BlueBay Asset Management, believes Warsh will keep the Fed separate. This does not rule out greater collaboration but makes a formal accord less likely in his assessment.

Cost Considerations in U.S. Debt Market Update

A shift by the Treasury to sell bills rather than interest-bearing securities would not be cost-free. With giant amounts of debt constantly rolling over, it would increase the volatility of Treasury borrowing costs significantly.

Figure 6: Visual representation of rising government debt and borrowing costs in the U.S. debt market. [Source: Freepik]

George Hall, an economics professor at Brandeis University and a former Chicago Fed researcher, warned about long-term risks. Outright coordination to dampen interest costs might work temporarily. However, investors have alternatives to US assets and will eventually take their money elsewhere.

Final Thoughts

Bond market news surrounding Warsh’s Fed-Treasury accord proposal reflects significant uncertainty about future monetary policy coordination. The bond market reaction demonstrates investors are closely watching for any signals about implementation details.

Whether the accord proves a minor administrative change or a major policy shift remains unclear. The U.S. debt market update will continue evolving as Warsh potentially takes the helm in May following confirmation. Market participants remain vigilant about preserving Fed independence while acknowledging coordination possibilities.

FAQs

Q1. What is Kevin Warsh’s proposed Fed-Treasury accord?

Ans. Warsh has advocated for a modern version of a 1951 agreement between the Federal Reserve and the Treasury Department. The proposal would clearly describe the Fed’s balance sheet size while the Treasury outlines debt issuance plans.

Q2. How has the bond market reaction reflected investor concerns?

Ans. Bond market reaction has been mixed with concerns about Fed independence and potential volatility. Investors worry the accord could shift the Fed away from its inflation-fighting mandate toward managing government borrowing costs.

Q3. What does the U.S. debt market update reveal about the Treasury’s position?

Ans. The U.S. debt market update shows Treasury Secretary Scott Bessent supports Fed quantitative easing only during true emergencies. He believes prolonged QE damaged the market’s ability to generate important financial signals.

Q4. Could the Fed shift its portfolio to short-term securities?

Ans. Yes. Analysts expect a Warsh-led Fed might roll Treasury holdings from longer-tenor securities to bills. Deutsche Bank predicts T-bills could rise to 55 per cent of Fed holdings from less than 5 per cent currently.