Asian Battery Metals PLC (ASX: AZ9) has capped a productive December 2025 quarter with a series of technical milestones across its Mongolian exploration portfolio. The Company delivered impressive metallurgical test results showing copper recoveries of 89-95% at its flagship Oval Cu-Ni-PGE Project, while due diligence drilling at the Maikhan Uul Cu-Au acquisition target returned high-grade copper and gold intercepts that validate the project’s potential.

The December quarter also saw the Company complete scout drilling at its Tsagaan Ders Lithium Project, successfully complete a $6 million equity placement, and maintain a strong cash position of $5.965 million heading into 2026.

Oval Cu-Ni-PGE Project: Metallurgical Excellence Meets Exploration Success

The 100%-owned Yambat Project, anchored by the Oval Cu-Ni-PGE deposit, remains Asian Battery Metals’ primary value driver. During the quarter, metallurgical test work completed at ALS Metallurgy in Perth returned excellent copper recovery rates across three composite samples representing different mineralisation styles:

- Low Cu-Ni composite (disseminated): 89.3% copper recovery, 55.4% nickel recovery

- High Cu-Ni composite (massive sulphide): 95.0% copper recovery, 46-64.7% nickel recovery

- Medium Cu-Ni composite (net textured): 94.9% copper recovery, 41.6-77.2% nickel recovery

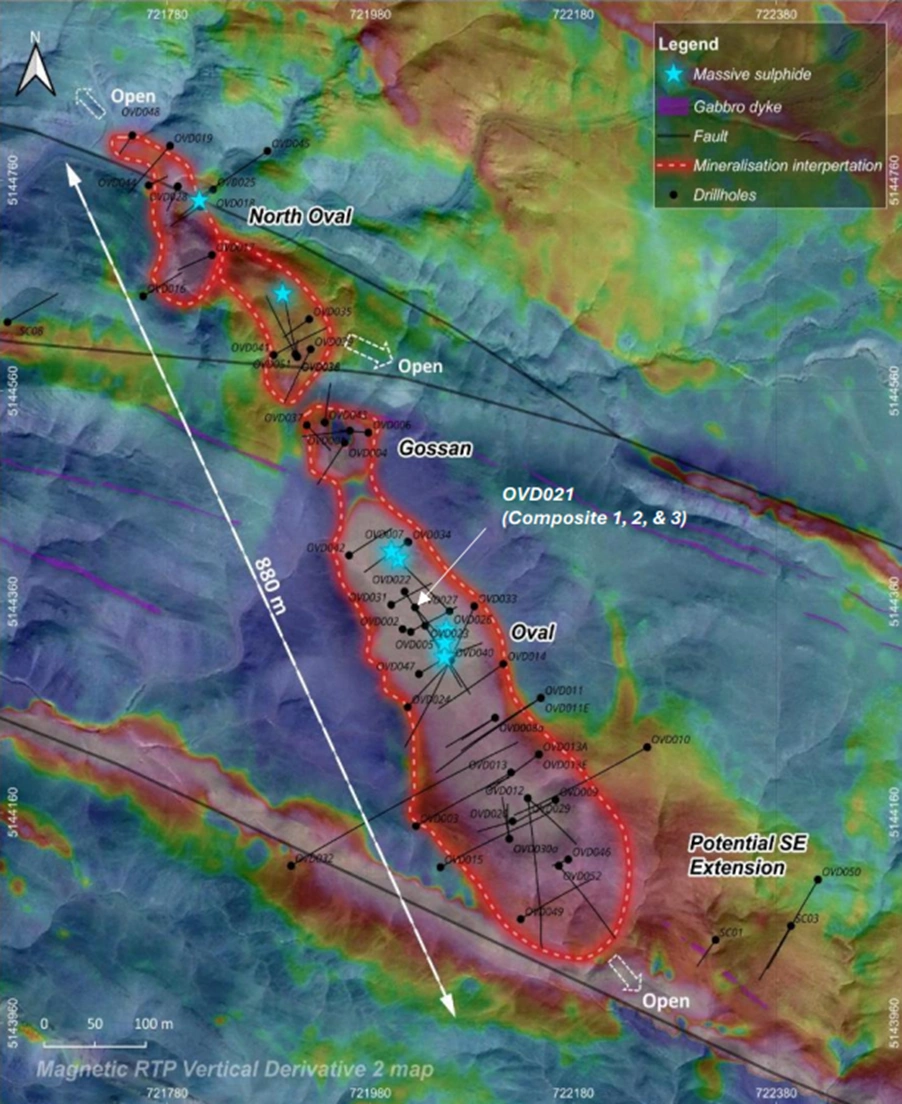

Figure 1: Location map showing drillholes at Oval Cu-Ni-PGE Project [Asian Battery Metals]

The metallurgical analysis confirmed chalcopyrite as the sole copper-bearing mineral, with pentlandite and violarite representing the major nickel-iron sulphides. Significantly, around 70% of the mineralisation was classified as “well liberated,” indicating straightforward processing characteristics that could translate into a low-cost operation.

Latest results of Phase 3 drilling delivered last 6 drillholes of 2026 exploration work, with assay results confirming extensions of mineralisation along strike to the southeast. Key intercepts included:

- OVD049: 16.8m @ 0.39% Cu, 0.41% Ni from 155.3m (including 1.9m @ 1.03% Cu, 1.33% Ni)

- OVD051: 9.3m @ 1.06% Cu, 0.48% Ni from 108.2m (including 3.8m @ 1.46% Cu, 0.66% Ni)

- OVD047: 44m @ 0.28% Cu, 0.28% Ni from 29m (including 26m @ 0.40% Cu, 0.37% Ni)

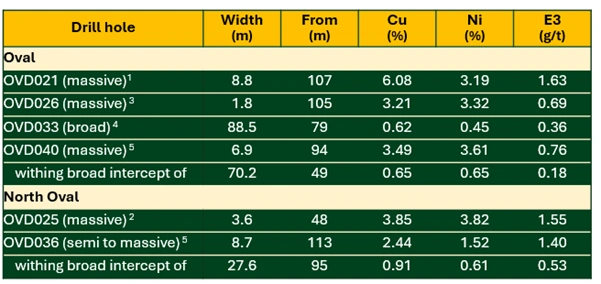

The past drilling campaigns have delivered multiple zones of high-grade intercepts of massive and semi-massive sulphide mineralisation across both the Oval and North Oval zones. These intercepts demonstrate the high-grade potential of the discovery, with several drillholes returning exceptional copper, nickel and PGE values over substantial widths.

Figure 2: Summary of significant high-grade intercepts from Oval and North Oval zones [Asian Battery Metals]

Maikhan Uul Acquisition: High-Grade Copper-Gold Validates Strategic Move

Due diligence drilling at the Maikhan Uul Cu-Au VMS Project delivered compelling results that confirm the project’s high-grade potential. Drill hole MU2501, a twin of historic hole MU_DH1204, intersected:

Strongly mineralised massive sulphide zones:

- 14.5m @ 2.23% Cu and 0.73g/t Au from 132.5m, including:

- 4.8m @ 2.80% Cu and 0.88g/t Au from 132.5m

- 6.3m @ 2.58% Cu and 0.82g/t Au from 139.7m

- 2.6m @ 2.28% Cu and 0.49g/t Au from 154.1m

Shallow high-grade gold and silver mineralisation:

- 5.2m @ 6.54g/t Au and 126.40g/t Ag from 36.9m, including:

- 2.1m @ 13.33g/t Au and 227.81g/t Ag from 37.9m

- 4.8m @ 2.02g/t Au and 35.39g/t Ag from 28.2m

- 3.0m @ 1.16g/t Au and 0.07% Cu from 45m

Figure 3: Maikhan Uul drillhole and rock chip sample locations [Asian Battery Metals]

The massive sulphide lens strikes east-southeast to west-northwest and sits below the historic resource estimate, indicating potential for deeper vertical extensions. Subject to satisfactory due diligence outcomes, the Company plans to complete settlement of the Maikhan Uul acquisition and commence fieldwork focused on shallow gold and silver mineralisation in Q1 2026.

Market Context: Strategic Timing in a Bullish Commodities Environment

Asian Battery Metals’ exploration momentum coincides with favourable market dynamics across its multi-commodity portfolio.

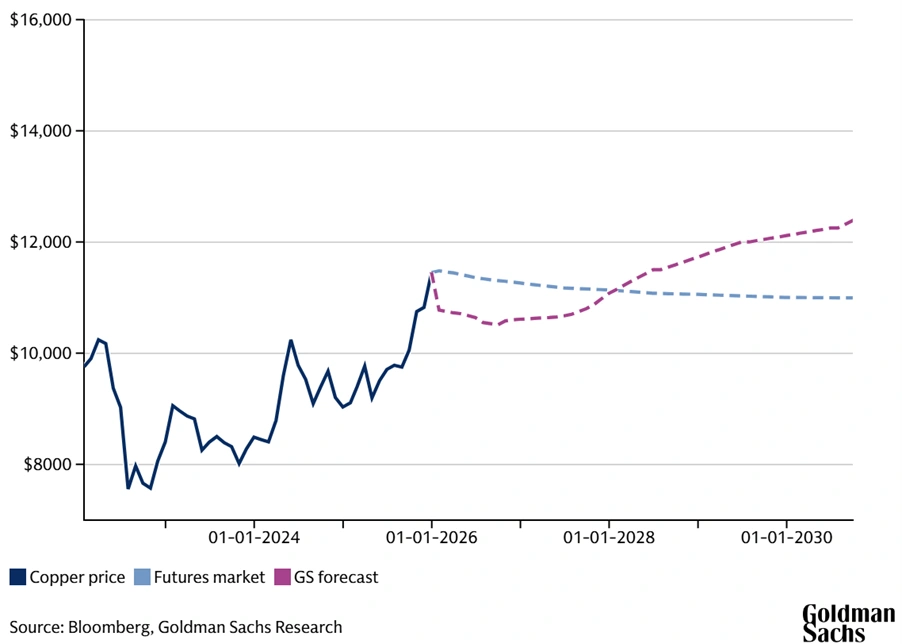

Copper Outlook Remains Constructive

Copper prices peaked at $11,771 per tonne in December 2025, reflecting structural demand growth from AI data centres, grid infrastructure, and electrification. While Goldman Sachs expects some near-term consolidation, the investment bank forecasts copper will average $10,000-$11,000 per tonne throughout 2026, with prices rising beyond 2027 as the market enters deficit conditions.

Figure 4: Copper Price Forecast [Goldman Sachs Research]

The bank’s research highlights that grid and power infrastructure investments will drive more than 60% of copper demand growth through 2030, adding the equivalent of another United States to global copper consumption.

Mongolia’s Investment Grade Momentum

A historic milestone for Mongolia’s financial standing was achieved in Q4 2025. S&P Global Ratings upgraded Mongolia’s sovereign credit rating to BB- from B+ with a stable outlook – the first time the country has reached the BB category. This was followed by Moody’s Ratings upgrading the country to B1 from B2.

These upgrades reflect a material reduction in the government debt-to-GDP ratio (forecast to drop to 31.2% in 2025) and the massive boost in copper exports from the Oyu Tolgoi underground expansion, which saw a 45% increase in production volume in 2025. The improved sovereign rating reduces financing costs and enhances Mongolia’s attractiveness as an exploration and mining jurisdiction.

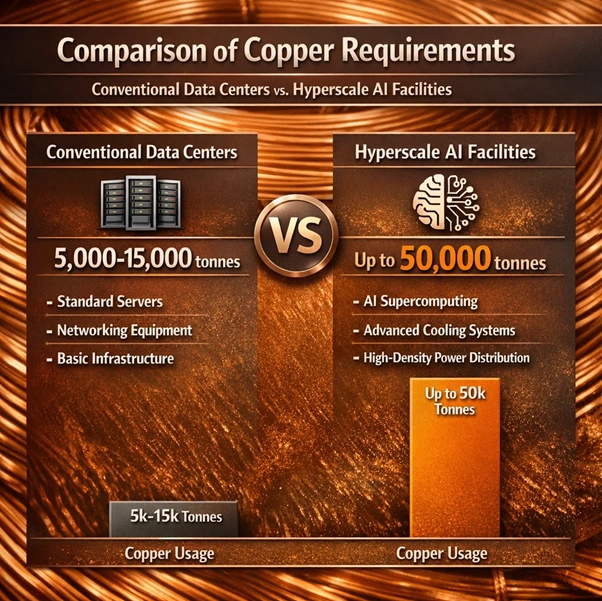

AI Data Centers Drive Structural Demand

Artificial intelligence data centers are emerging as a major new demand pillar. A conventional data center uses 5,000 to 15,000 tonnes of copper, while a hyperscale AI facility requires up to 50,000 tonnes.

Figure 5: Comparison of copper requirements – conventional data centres vs. hyperscale AI facilities

By 2030, data centers will consume between 330,000 and 1.1 million tonnes of copper annually, representing up to 3% of global demand.

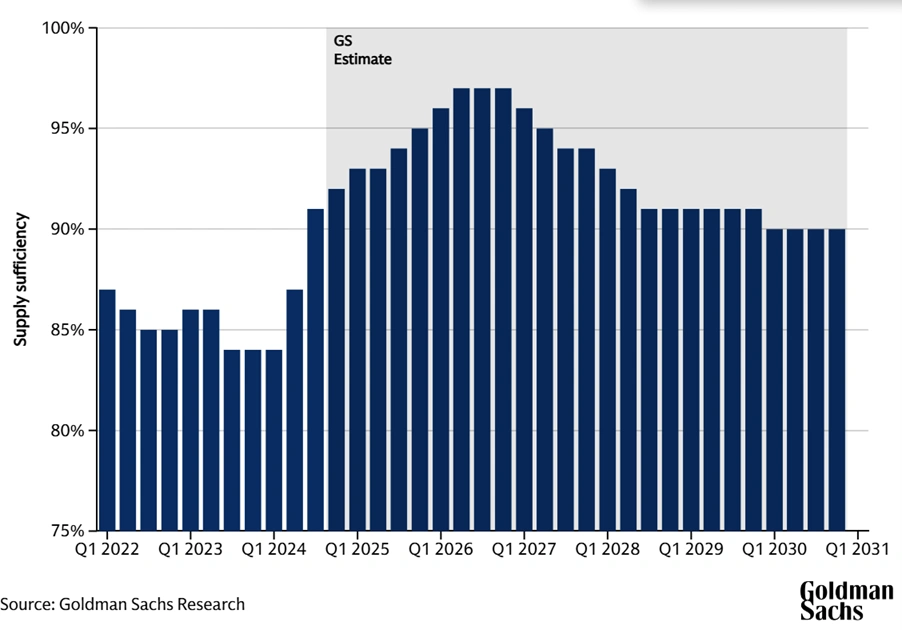

Goldman Sachs projects a 165% increase in data centre power demand by 2030, with massive copper requirements for cooling systems, power distribution, transmission lines and grid connections. North American data centre spending reached $50 billion in 2025, laying the groundwork for the material demands now defining 2026.

Figure 6: Estimates for data centre occupancy rates [Goldman Sachs Research]

Corporate Strength and Community Commitment

Asian Battery Metals closed the December quarter with $5.965 million in cash, providing an estimated 3.21 quarters of funding. The Company successfully completed a $6 million equity placement (before costs) in October 2025, demonstrating strong investor support for its exploration strategy.

Figure 7: Asian Battery Metals staff at a project site [Asian Battery Metals]

The Company maintained a strong ESG focus during the quarter, implementing Social Responsibility Agreements across multiple soums. Environmental rehabilitation works were undertaken at the Yambat, Maikhan Uul, and Tsagaan Ders project sites, with all 2025 Environmental Management Reports approved by local authorities.

Khukh Tag Graphite: Maintaining Strategic Optionality

While not the primary focus, the Company’s 100%-owned Khukh Tag Graphite Project retains a JORC 2012 Mineral Resource Estimate of 12.2 million tonnes @ 12.3% Total Graphitic Carbon (1,498,800 tonnes contained graphite). Minimum expenditure was maintained during the quarter to retain tenure.

Investor’s Outlook

Asian Battery Metals is executing a multi-pronged strategy targeting Mongolia’s diverse mineral endowment at a time when global markets are rewarding exposure to battery metals and base metals. The combination of excellent metallurgical results at Oval, high-grade discoveries at Maikhan Uul, and strategic lithium exposure at Tsagaan Ders positions the Company across key energy transition commodities.

The Company’s systematic approach, advancing Oval towards a definitive study while pursuing high-grade acquisition opportunities, reflects disciplined capital allocation in a jurisdiction that is rapidly gaining international credibility.

Key Catalysts for 2026:

- Updated 3D geological and geophysical model incorporating Phase 3 drilling data at Oval

- Planning and permitting of the 2026 exploration program

- Settlement of Maikhan Uul acquisition (subject to due diligence)

- Shallow gold and silver fieldwork at Maikhan Uul

- Potential restarts of exploration at Khukh Tag, given improved market conditions

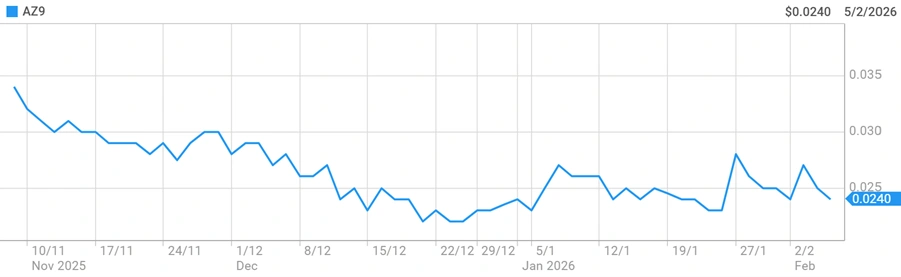

As of 5 February 2026, Asian Battery Metals’ shares are trading at $0.024 on the ASX within a 52-week range of $0.021 – $0.055. The Company’s current market capitalisation stands at approximately $20.51 million.

Figure 8: AZ9 Price Chart [ASX]

With a fully funded exploration pipeline, technical momentum across multiple projects, and improving market fundamentals for copper, gold, and lithium, Asian Battery Metals is positioning itself as a credible multi-commodity explorer in one of Asia’s most prospective mining jurisdictions.

Figure 9: Project locations in Mongolia [Asian Battery Metals]

For investors seeking leveraged exposure to the energy transition through early-stage exploration in a jurisdiction with improving sovereign risk metrics, Asian Battery Metals offers a compelling asymmetric opportunity anchored by solid technical fundamentals and disciplined project advancement.