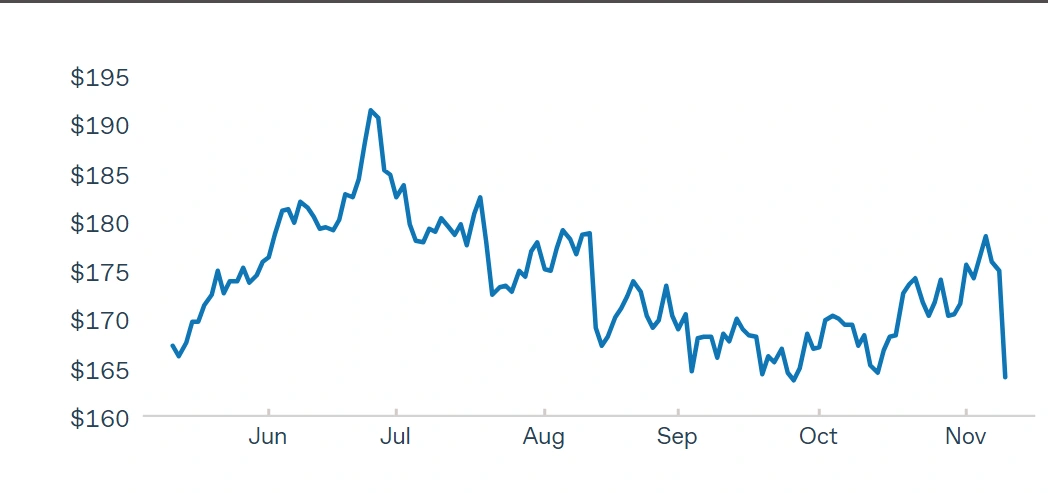

Commonwealth Bank of Australia (ASX: CBA) shares took a beating on Tuesday morning, sinking 5% to $166.31 despite the banking giant delivering a solid quarterly profit of $2.6 billion.

The market’s reaction highlights growing investor unease about Australia’s largest bank. CBA’s premium valuation and shrinking profit margins are now under the microscope.

The selloff came immediately after the bank released its first quarter FY26 trading update before market open. While the numbers looked respectable on paper, they failed to justify the stock’s eye-watering price tag.

Profit Growth Fails to Impress Market

CBA reported cash net profit after tax of $2.6 billion for the three months ending 30 September 2025. This represented a modest 2% increase compared to the same quarter last year and just 1% higher than the second half FY25 quarterly average.

Operating income climbed 3%, driven by:

- Lending volume growth of $9.3 billion in home loans

- Strong household deposit growth of 9.5%

- Business lending expansion of 10.5%

The bank also benefited from 1.5 additional trading days in the quarter. Yet investors were not convinced the growth momentum justified current share prices.

CEO Matt Comyn acknowledged the challenging environment. “We are closely watching the increased competitive intensity and implications across the financial system,” he said in the quarterly statement.

The Valuation Problem That Won’t Go Away

CBA shares currently trade at a price-to-earnings ratio exceeding 28 times. This compares to a banking sector average of just 20 times and makes CBA almost twice as expensive as rivals like ANZ Group (ASX: ANZ).

The Australian banking sector has faced scrutiny over elevated valuations in recent months. CBA stands out as the most expensive, trading at a premium that analysts struggle to justify through fundamentals alone.

IG Markets analyst Tony Sycamore noted that CBA’s net interest margin contraction caused particular concern. The margin measures the difference between what banks pay depositors and charge borrowers.

“Even after its pullback from the $192.00 high of late June, the stock remains expensive on some metrics,” Sycamore told reporters.

CBA hit an all-time high of $192 per share in June 2025. The current price of $166.31 represents a decline of roughly 13% from that peak. Many analysts believe further falls are likely.

What’s Squeezing CBA’s Margins

The quarterly update revealed a headline net interest margin reduction due to mix effects. Strong growth in lower-yielding liquid assets and institutional repos dragged down the bank’s overall margin.

Excluding these factors, the underlying margin only declined slightly. However, three headwinds continue to apply pressure:

- Deposit switching by customers seeking better rates

- Intense competition for home loans

- Lower cash rate environment following RBA cuts

The bank maintained its lending grew at 1.1 times system for home loans during the quarter. This indicates CBA is still capturing market share despite competitive pressures.

Home loan arrears have also stabilised, with 85% of customers now ahead of scheduled repayments. Credit quality metrics improved, with troublesome loans falling to 0.94% from 0.97% in June.

Analysts Sound Valuation Alarms

Multiple investment houses have flagged CBA shares as overvalued. S&P Global analysts project a potential 23% decline over the next 12 months based on consensus price targets.

Bloomberg Intelligence compiled forecasts suggesting CBA faces the weakest return potential among global banking stocks. Researchers see shares tumbling 26% in the next year.

Bell Potter maintains a price target of $120 per share, indicating roughly 30% downside from current levels. The firm cites no fundamental support for CBA’s premium valuation.

“It is purely a function of passive flows into Australia,” explained Matthew Wilson, analyst at Jarden Research Division.

As Australia’s largest company by market capitalisation, CBA holds significant weight in major indices. This forces index-tracking funds to buy the stock regardless of valuation, creating artificial demand.

The bank remains the most shorted among major Australian banks. About 1% of shares outstanding are currently on loan to short sellers betting on price declines.

How CBA Stacks Up Against Rivals

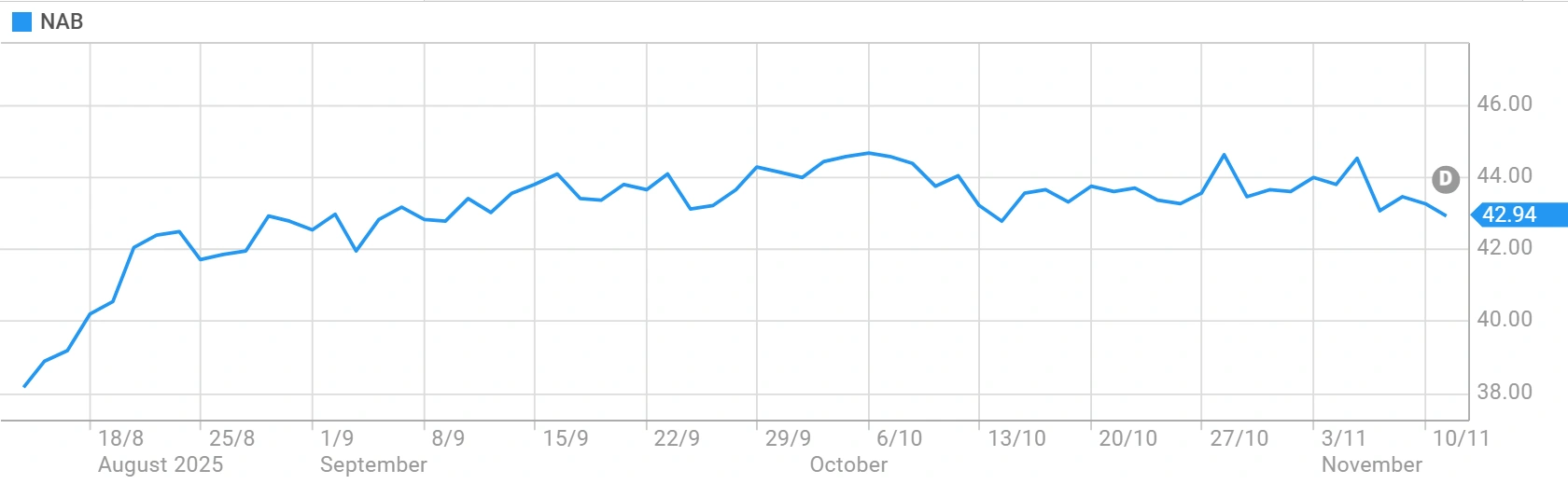

The Big Four banks have delivered mixed results in recent reporting seasons. NAB shares tumbled more than 4% after its full-year results, while Westpac gained 3.6%.

ANZ shares climbed almost 5% to record highs following its report. The smallest of the Big Four benefited from tough executive bonus decisions and playing catch-up with competitors’ valuations.

CBA’s market capitalisation exceeds $281 billion, dwarfing its nearest banking rival. The bank employs around 50,000 people and dominates Australian mortgage markets with over 20% market share.

Despite premium pricing, CBA’s dividend yield sits below 3%, making it less attractive than peers for income investors. The bank paid out total dividends of $4.85 per share in FY25, fully franked.

Competitive Pressures Mount

The Australian banking sector faces several structural challenges heading into 2026. Rising competition for deposits and mortgages continues squeezing margins across the industry.

Digital challengers and non-bank lenders are capturing market share from traditional banks. This forces the Big Four to compete more aggressively on pricing, reducing profitability.

Global economic uncertainty also weighs on the sector. Geopolitical tensions, trade disputes, and uneven economic growth create headwinds for banks’ international operations.

CEO Matt Comyn acknowledged these challenges while maintaining an optimistic outlook. “Despite escalating geopolitical and macroeconomic uncertainty, we are optimistic on the outlook for the country,” he stated.

The bank highlighted its strong balance sheet settings, with CET1 capital well above regulatory minimums at 12.4%. Deposit funding represents 79% of total funding, providing stability.

CBA has raised $16 billion in long-term wholesale funding for FY26 requirements to date. This demonstrates the bank’s ability to access capital markets despite market volatility.

The Reality Check Investors Needed

Today’s share price drop may represent an overdue reality check for CBA investors. The bank has defied valuation critics for years, rocketing around 90% between October 2023 and June 2025.

Many retail investors show fierce loyalty to CBA shares, making them reluctant to take profits despite lofty valuations. Financial planners report clients resist selling CBA even when portfolios become overweight.

The question now is whether this marks a temporary setback or the start of a sustained decline. With a P/E ratio still above 30 after today’s fall, CBA remains expensive by historical standards.

Analysts warn that mean reversion could drive shares significantly lower. Using sector-average multiples, fair value estimates range from $100 to $143 per share depending on methodology.

Australian financial stocks continue facing scrutiny as investors question the source of future growth. With margins under pressure and competition intensifying, earnings expansion looks challenging.

The RBA’s recent rate cuts provide some relief by reducing credit risk. However, lower rates also compress the profit margins banks earn on their loan books over time.

Also Read: Commonwealth Bank of Australia Reports Capital Adequacy and Risk Disclosures as at 30 September 2025

What This Means for Investors

Current CBA shareholders face a decision about whether to hold through volatility or realise profits after strong gains. New investors considering entry must weigh the bank’s quality against its valuation premium.

CBA offers stability, market leadership, and reliable dividends. The bank’s strong capital position and conservative lending standards provide downside protection during economic downturns.

However, paying 28 times earnings for single-digit profit growth tests the limits of rational valuation. The risk-reward equation looks unfavourable unless you believe CBA deserves a permanent premium to peers.

Alternatives exist within the banking sector for investors seeking exposure. ANZ, NAB, and Westpac trade at more reasonable multiples while offering similar or better dividend yields.

Some analysts suggest regional banks like Bendigo and Adelaide Bank offer better value for growth-oriented investors. These smaller players can potentially gain market share from the Big Four.

Today’s 5% decline wipes billions from CBA’s market value but barely dents its year-to-date gains. The stock remains up significantly over 12 months despite recent weakness.

Whether CBA shares have further to fall depends largely on earnings momentum in coming quarters. If margin pressure intensifies or credit quality deteriorates, the premium valuation will face increased scrutiny.

For now, the market has delivered its verdict on this quarter’s results. Solid performance is no longer enough to justify Australia’s most expensive bank stock.