Australia’s international insurance giant strengthens its capital base with a strategic debt issuance. QBE Insurance Group (ASX:QBE) has successfully priced USD 300 million of fixed-rate resetting subordinated notes, marking a calculated move to enhance Tier 2 capital under regulatory requirements.

Figure 1: QBE Insurance Group Headquarters

The QBE USD subordinated notes pricing announcement arrives as the company executes its ongoing funding and capital management strategy, replacing older, higher-cost debt with more attractive terms for the insurer.

USD 300 Million Fixed-rate Notes Due 2037

QBE Insurance Group announced on 5 November 2025 that it has successfully priced the QBE Insurance Group subordinated notes offer with institutional investors. The notes will mature in November 2037, providing a 12-year term for the debt instrument.

Key terms of the USD subordinated notes investment QBE include:

- Initial fixed interest rate of 5.239% per annum

- Semi-annual interest payments until November 2032

- Interest rate resets in 2032 to US Treasury five-year yield plus 1.35%

- Eligible as Tier 2 Capital under APRA’s capital adequacy standards

- Callable by QBE from November 2032 with APRA approval

The USD 300 million issuance, equivalent to approximately AUD 462 million, forms part of QBE’s Note Issuance Programme and targets institutional investors rather than retail participants.

QBE Insurance Group Subordinated Notes Offer Includes Regulatory Conversion

The QBE Insurance Group subordinated notes offer includes standard regulatory conversion provisions. The subordinated notes will be convertible to QBE ordinary shares in full or part if APRA determines QBE is, or would become, non-viable.

This conversion mechanism provides an additional capital buffer during periods of financial stress, aligning with APRA’s capital requirements for regulated insurers. The provision aims to absorb losses and recapitalise the company before taxpayer funds become necessary.

Figure 2: Generic Representation of Capital Growth

QBE highlighted that investors should not expect APRA’s approval for early redemption of the notes, except under specific tax or regulatory circumstances. Any early redemption would require prior written approval from APRA, which may or may not be provided.

The notes rank behind senior creditors but ahead of ordinary shareholders in the capital structure. Upon completion of redemption of any notes, they will be cancelled and delisted from relevant exchanges.

USD Subordinated Notes Investment QBE Enhances Tier 2 Capital

The proceeds from the USD subordinated notes investment QBE will support the company’s Tier 2 capital position under APRA’s capital adequacy framework. Tier 2 capital provides a secondary layer of protection against losses for policyholders and creditors.

QBE’s regulatory capital position at 30 June 2025 showed an APRA PCA Multiple of 1.85 times, sitting at the top end of the company’s 1.6 to 1.8 times target range. The interim dividend reduced capital by approximately 4 percentage points.

Figure 3: QBE Insurance Representatives at a Global Financial Conference

Following the subordinated notes issuance and the redemption of older debt, QBE expects to maintain regulatory capital comfortably above the S&P ‘AA’ level. Debt to total capital stood at 25.2% as at 30 June 2025, within the company’s 15% to 30% target range.

The company’s strong capitalisation supports its ability to write new business, withstand catastrophe events and maintain financial flexibility across market cycles.

What This Means for Investors

The QBE USD subordinated notes pricing demonstrates prudent capital management as the company refinances higher-cost debt whilst maintaining regulatory buffers. The transaction reduces annual interest costs whilst extending debt maturity, improving financial flexibility.

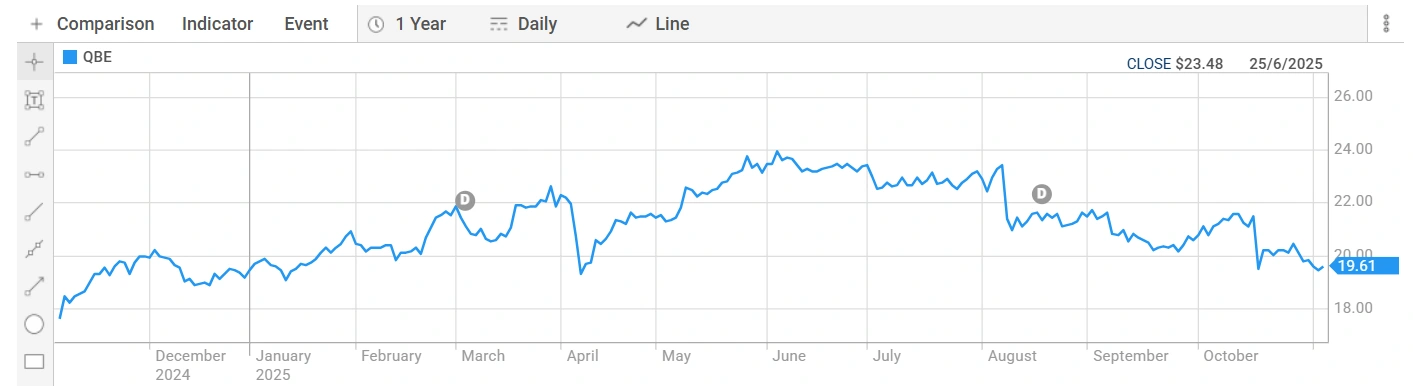

QBE currently trades at AUD 19.625 per share, with a 52-week range of AUD 16.810 to AUD 24.200 per share. The stock maintains average daily trading volume of 3,677,172 shares, providing liquidity for institutional and retail investors.

The subordinated notes issuance supports QBE’s capital position without diluting existing shareholders. The company maintains regulatory capital above S&P ‘AA’ level whilst delivering improved returns, with adjusted return on equity of 19.2% for 1H25.

Figure 4: QBE Insurance Group (ASX: QBE) Share Price Trend

Analysts maintain positive outlooks on QBE, with the stock trading within its 52-week range and demonstrating resilient underwriting performance. The combined operating ratio of 92.8% positions the company competitively within the global P&C insurance sector.

The successful debt refinancing at 5.239% versus the 6.10% cost of redeemed notes translates to approximately USD 2.6 million of annual interest savings, supporting profitability and returns to shareholders.

FAQS

- What are the key terms of QBE’s subordinated notes?

QBE priced USD 300 million of subordinated notes due November 2037 with an initial interest rate of 5.239%. The rate resets in 2032 to US Treasury five-year yield plus 1.35%. Notes are callable from November 2032 with APRA approval.

- Why is QBE issuing these notes?

QBE is refinancing USD 300 million of 6.10% notes due in 2045, reducing annual interest costs by approximately USD 2.6 million. The new 5.239% rate offers significantly better terms whilst strengthening Tier 2 capital.

- What was QBE’s 1H25 financial performance?

QBE reported adjusted net profit of USD 997 million, up 28% on 1H24. Adjusted ROE reached 19.2% and combined operating ratio improved to 92.8%. The company paid an interim dividend of 31 per share.

- What is QBE’s current share price and FY25 outlook?

QBE trades at AUD 19.625 per share with a 52-week range of AUD 16.810 to AUD 24.200. The company expects FY25 combined operating ratio of 92.5% and mid-single digit GWP growth.