The counter-drone specialist just dropped results that make most ASX growth stories look pedestrian. Revenue didn’t just climb. It exploded.

Droneshield (ASX: DRO) reported quarterly revenue of $92.9 million for the three months ending September 30, 2025. That’s an eye-watering 1,091% increase compared to the same period last year.

Cash receipts hit an all-time high of $77.4 million. Operating cashflow turned positive at $20.1 million. A year ago, the company was burning $19.4 million per quarter. Now it’s printing cash.

The Sydney-based company has gone from promising startup to serious defence contractor in under 12 months. Year-to-date committed revenues now sit at $193.1 million, already crushing the entire 2024 full-year result.

DroneShield’s AI-powered counter-drone systems.

DroneShield’s AI-powered counter-drone systems.

The Numbers Behind the Surge

The Droneshield Q3 revenue performance wasn’t driven by a single mega-deal. Multiple contracts across different geographies are firing.

Key metrics from the quarter:

- Revenue: $92.9 million (up 1,091%)

- Cash receipts: $77.4 million (up 751%)

- Operating cashflow: $20.1 million (vs -$19.4 million loss)

- SaaS revenue: $3.5 million (up 400%)

- Cash and equivalents: $212.8 million

The company completed a $62 million European defence contract during the quarter. It also secured an $11.7 million research agreement with the U.S. Department of Defense.

These wins validate Droneshield’s technology at the highest levels of global defence procurement. The Australian defence sector continues to demonstrate strong export potential.

Software Pivot Gaining Momentum

Software-as-a-service revenue grew 400% year-on-year to $3.5 million. That might sound small. But it represents a strategic shift towards recurring, high-margin revenue.

The company launched two new platforms during the quarter. DroneSentry-C2 Enterprise targets military and government customers. SentryCiv aims at civilian infrastructure like airports and stadiums.

Both products run on subscription models. They integrate with Droneshield’s existing hardware portfolio. The AI-powered software receives quarterly feature upgrades, keeping customers locked into the ecosystem.

Industry watchers note that SaaS attach rates are climbing. That’s a positive signal for long-term profitability. Defence contracts are lumpy. Software subscriptions smooth the revenue curve.

Manufacturing Footprint Expands

Droneshield opened a new research and development facility in South Australia during the quarter. The company also expanded its U.S. operations.

Manufacturing capacity now supports annual production of $400 million. Plans are in place to push that to $500 million. Current inventory sits at $240 million, allowing for rapid delivery on new orders.

The company employs 373 people as of August 2025, up from 250 at the end of 2024. Engineering headcount reached 285. That’s an 85% engineering ratio rarely seen outside pure-play tech firms.

This heavy engineering focus supports quarterly AI software releases. It also enables rapid product iteration based on field feedback from active conflict zones.

DroneShield Sydney Warehouse

DroneShield Sydney Warehouse

Market Context and Competition

Global defence spending continues to climb. The counter-drone market is forecast to reach $7.05 billion by 2029, expanding at a 26.7% CAGR from $2.16 billion in 2024.

Droneshield faces competition from defence giants like Raytheon and Lockheed Martin. It also competes with specialists like Dedrone and Israel Aerospace Industries.

The company’s edge lies in its portable, software-driven approach. Traditional defence contractors favour integrated systems. Droneshield offers modular solutions that deploy faster and cost less.

The technology sector on the ASX has seen strong performance this year, with defence tech emerging as a standout category.

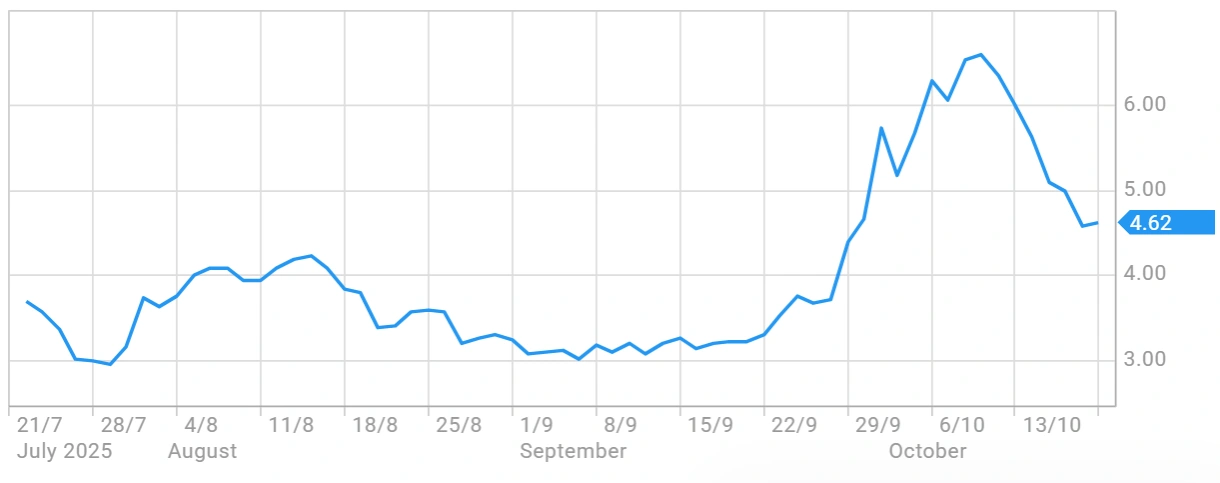

Share Price and Market Performance

Droneshield shares have delivered exceptional returns over the past 12 months. The stock is up 337% year-on-year, significantly outpacing the broader ASX 200 which rose around 9%.

The company entered the S&P/ASX 200 Index during the September rebalance. That inclusion brings automatic inflows from index funds and increased institutional coverage.

Current market capitalisation stands at approximately $4.01 billion. The stock trades in a 52-week range of $0.585 to $6.705. Recent trading shows some volatility, typical for high-growth defence stocks.

Investment firm Bell Potter ranks Droneshield among its top buying ideas. The analyst community generally maintains positive coverage, citing strong order pipeline and margin expansion potential.

DroneShield Share Price

DroneShield Share Price

Pipeline and Forward Guidance

Droneshield reports a project pipeline of $2.3 billion with 284 active opportunities. Not all will convert. But the pipeline provides visibility into potential future revenue.

The company doesn’t provide formal guidance. However, year-to-date committed revenue of $193.1 million suggests full-year 2025 will comfortably exceed $250 million.

Contract backlog sits at approximately $33 million expected to deliver in the first half of 2026. That provides a strong starting point for next year’s performance.

Management continues to invest heavily in R&D. Quarterly spending on research and capital expansion hit $5.3 million this quarter. That reinvestment supports the technology moat required to compete with larger defence contractors.

Strategic Positioning

The geopolitical environment favours counter-drone technology. Conflicts in Ukraine and the Middle East demonstrate the threat posed by small drones.

State and non-state actors increasingly deploy UAVs for surveillance, reconnaissance, and direct attack. Traditional air defence systems struggle with small, slow-moving targets.

Droneshield’s systems fill this gap. The technology works across multiple domains: dismounted infantry, vehicle-mounted, and fixed installations.

The U.S. market represents approximately 70% of revenue. European and Asia-Pacific regions are growing. Regulatory changes in the U.S. may enable broader adoption across federal agencies and critical infrastructure.

Investment Considerations

The Droneshield Q3 revenue performance demonstrates strong execution. The company has transitioned from loss-making startup to cash-positive operation.

Several factors support continued growth:

- Increasing global defence budgets

- Rising UAV threats across multiple theatres

- Expanding product portfolio with high-margin software

- Limited competition in the portable counter-drone segment

- Strong contract pipeline across multiple geographies

Risks remain. Defence contracts are unpredictable. Budget cuts could impact future orders. Competition from larger contractors may intensify. The current valuation prices in significant future growth.

The Australian market has shown appetite for defence technology stocks, particularly those with international reach and proven contract execution.