Australian defence tech pioneer DroneShield (ASX: DRO) dropped a bombshell this week. The company launched its most ambitious software platform yet and secured a major European contract. But instead of celebrating, investors sent the stock tumbling more than 20%.

The Sydney-based counter-drone specialist revealed DroneSentry-C2 Enterprise on 15 October 2025. This cloud-based command system allows defence operators to manage multiple installations across entire countries from a single interface.

Within hours of the announcement, DroneShield confirmed its first paying customer. A European military client on NATO’s eastern flank ordered the platform for deployment in early 2026.

The Platform That Changes Everything

DroneSentry-C2 Enterprise connects geographically dispersed counter-drone installations into one operational network. Military bases, airports, energy infrastructure, and data centres can now be monitored from a single dashboard.

DroneShield’s DroneSentry-C2 Enterprise enables protection of multiple critical sites simultaneously.

DroneShield’s DroneSentry-C2 Enterprise enables protection of multiple critical sites simultaneously.

Key capabilities include:

- Centralised drone alert management across all connected sites

- Real-time health monitoring for instant operational readiness

- Remote verification through live camera feeds

- Seamless transition from enterprise oversight to local control

“C2E addresses the realities of modern airspace security,” said Angus Bean, DroneShield’s Chief Technology and Product Officer. “Governments and infrastructure operators must manage counter-drone operations across many distributed sites.”

The platform integrates DroneShield’s ThreatAI software. This provides intelligent prioritisation of drone activity and improves operator confidence in dynamic battlefield conditions.

NATO Contract Validates Strategy

The European order represents a critical proof point for DroneShield’s enterprise strategy. The customer will deploy the system across an existing and growing cluster of DroneSentry installations on NATO’s eastern flank.

This region has become a focal point for counter-drone technology. Rising tensions and increased drone activity have driven demand for coordinated defence systems.

CEO Oleg Vornik outlined the company’s three-tier software approach. Embedded-level software optimises each device’s ability to track and defeat drones. Site-level software handles sensor fusion and target handover. Enterprise-level software provides multi-site threat awareness.

“C2E represents the last part of this software strategy,” Vornik explained. “Together, the three layers will provide maximum value to customers and assist in driving DroneShield’s goal of getting to 30-40% of revenue from SaaS over the medium term.”

The Share Price Paradox

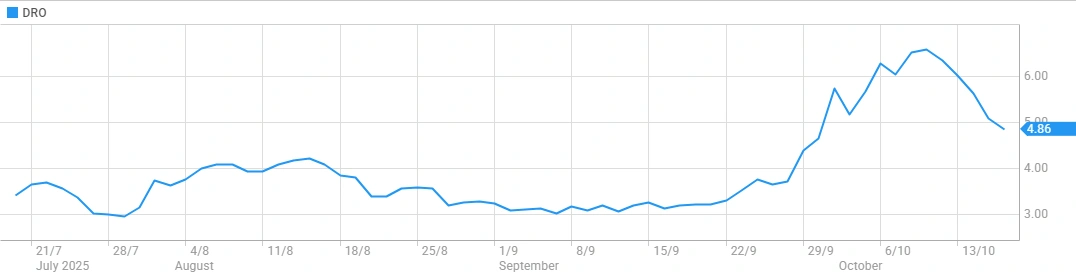

Despite the positive developments, DroneShield shares plunged from $6.71 to $5.10 between 9 October and 15 October. The stock closed at $5.10 on the day of the announcement, down 9.57%.

Market analysts attribute the decline to profit-taking after an extraordinary run. The stock has soared more than 600% in 2025 alone. DroneShield’s market capitalisation now exceeds $4.9 billion.

“After months of relentless gains, profit-taking and fading market euphoria often lead to natural consolidation phases,” noted market observers at Stocks Down Under.

Trading volumes surged during the sell-off. On 15 October, 19 million shares changed hands for approximately $96.48 million. Volume increased by 4 million shares compared to the previous day.

DroneShield share price volatility reflects investor psychology after massive 2025 gains.

DroneShield share price volatility reflects investor psychology after massive 2025 gains.

Revenue Transformation Underway

The SaaS strategy could fundamentally reshape DroneShield’s business model. Software-as-a-Service revenue reached $1.9 million in Q2 2025, up 161% year-on-year.

Second quarter revenue hit $38.8 million, a 480% increase from the $6.7 million posted in Q2 2024. Year-to-date figures have reached $72.3 million.

Purchase orders totalling $176.3 million for 2025 delivery had been secured by 22 July. The company’s current sales pipeline stands at $2.34 billion.

DroneShield is aggressively scaling operations. The workforce has grown to 363 staff, including 285 engineers. Plans call for expansion to 400 employees by year-end 2025.

Production capacity is expanding from $500 million annually to $2.4 billion by end-2026. A new $13 million Sydney facility will boost near-term capacity to $900 million by mid-2026.

Global Defence Spending Drives Demand

The counter-drone market is experiencing explosive growth. The global unmanned aerial systems sector is forecast to reach US$15-20 billion by 2030.

Europe’s €800 billion “ReArm Europe” defence initiative is a major tailwind. The eastern NATO flank has become a priority region for counter-drone deployments.

DroneShield’s recent achievements include a $61.6 million European contract in June 2025. This single order exceeded the company’s entire 2024 revenue of $57.5 million.

The company has also released an RfPatrol plugin for the TAK ecosystem. This integration delivers seamless situational awareness without standalone systems.

What’s Next for DroneShield?

The DroneSentry-C2 Enterprise launch marks a pivotal moment in DroneShield’s evolution. Success in the SaaS segment could provide high-margin, recurring revenue streams.

However, the 22% share price decline demonstrates investor nervousness about valuation. The stock trades at a P/E ratio exceeding 744, reflecting sky-high growth expectations.

Near-term catalysts include further contract wins, especially in Europe and the United States. The U.S. market already accounts for 20% of 2025 revenue and 29% of the sales pipeline.

For now, DroneShield continues to ride the wave of global defence spending. Whether the stock can maintain its momentum depends on execution and sustained demand for counter-drone solutions.

The company has proven it can deliver technology and win contracts. The real test is whether the SaaS transformation can justify one of the ASX’s most aggressive valuations.