The Australian supermarket sector is witnessing its most significant shake-up in decades.

Two international players, Costco and Aldi, have quietly amassed over $22 billion in combined annual revenue. They’re chipping away at the ironclad dominance of Coles and Woolworths.

The impact is forcing the traditional giants to rethink everything from pricing to store formats.

The Numbers Tell a Compelling Story

Costco Australia reported approximately $11.37 billion in revenue for the year ending September 2024, with annualised sales now reaching $5 billion.

Aldi generated $10.86 billion in total revenue during 2023, cementing its position as a genuine alternative to the big two.

Together, these international chains now command meaningful territory in Australia’s $199 billion supermarket and grocery sector.

The growth trajectory shows no signs of slowing. Costco confirmed plans to open its 16th Australian warehouse in Pakenham, Victoria, by 2027. Aldi operated 595 stores across Australia as of September 2024, with continued expansion underway.

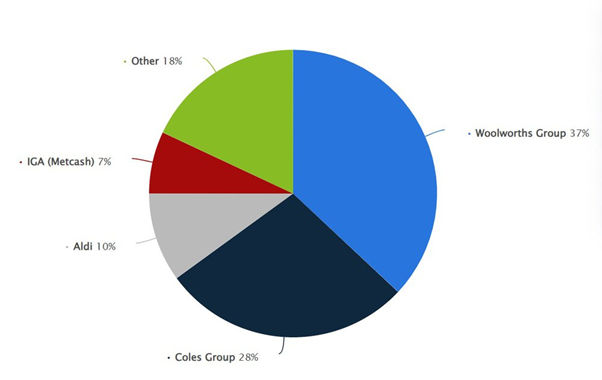

Market share distribution among major Australian supermarket chains. Source: Statista

Breaking the Duopoly Grip

For years, Coles and Woolworths operated in comfortable territory.

The Australian Competition and Consumer Commission found Woolworths holds 38% of supermarket grocery sales while Coles commands 29%. Combined, they control approximately 67% of the market.

But the landscape is shifting.

Aldi has captured 9% of the market, while Metcash sits at 7%. More importantly, consumer sentiment is turning towards value-focused retailers.

The ACCC’s supermarket inquiry revealed something crucial. The oligopolistic structure limits Coles’ and Woolworths’ incentive to compete vigorously on price.

Why Costco’s Model Works Down Under

Costco operates differently from traditional supermarkets.

The membership-based warehouse club generates significant revenue from its $65 annual membership fees. Membership fees accounted for 65.5% of Costco’s 2024 net operating income globally.

This model allows aggressive pricing on products. Profit doesn’t come from massive markups on groceries but from the steady stream of membership renewals.

Industry insiders estimate each Costco warehouse attracts around 100,000 paid subscribers, giving the company a base of approximately 1.5 million members across Australia.

The expansion strategy is measured but deliberate. Costco now operates 15 warehouses across Australia, with a 16th planned for 2027.

UNSW Professor Nitika Garg noted Costco’s model targets the “monthly pantry load” rather than weekly shopping trips. This positions them outside direct competition with Coles and Woolworths for now.

But that could change, Costco’s recent partnership with DoorDash allows non-members to shop via delivery, potentially expanding their reach into more frequent shopping occasions.

Aldi’s Steady March Continues

Aldi entered Australia in 2001 and has been methodically building market share ever since.

The German discount chain operates on an everyday low pricing model. Aldi maintained a 12.6% market share as of early 2016 and has continued growing.

As of September 2024, New South Wales was home to 203 Aldi stores, the highest concentration in Australia. Victoria followed closely, with the total network spanning 595 locations nationally.

The formula is straightforward: limited product range, private label focus, and aggressive pricing.

YouGov research confirms the strategy works. Australians view Aldi as the supermarket chain offering the best value compared to other chains.

Aldi stores across Australia.

The Pressure on Coles and Woolworths

The traditional players aren’t standing still. Coles has nearly completed a five-year investment turnaround initiative focused on refurbishment and customer experience. Woolworths management has pointed to neutralising Coles while containing Aldi on pricing.

Both chains are expanding their online presence. Coles partnered with Ocado for automated distribution centres, while Woolworths is developing micro-fulfillment centres.

But maintaining margins while competing on price presents a challenge.

The ACCC found that regardless of the metric applied, Coles and Woolworths are among the most profitable supermarket businesses among their global peers.

That profitability is being squeezed as consumers gravitate toward lower-cost alternatives amid cost-of-living pressures.

What This Means for Australian Shoppers

Competition benefits consumers. Recent data shows seven banners emerged as double-digit performers in retail growth, including Guzman y Gomez, Costco, Aldi, Kmart, Chemist Warehouse, Coles and Woolworths.

The increased competition is forcing innovation across the sector:

- Loyalty programs are becoming more sophisticated

- Store formats are diversifying

- Online grocery shopping is expected to generate US$8.95 billion in revenue in 2024, growing annually at 9.25% to reach US$13.93 billion by 2029

- Private label offerings are expanding

Aldi introduced a convenience-focused “Corner Store” format, while Costco continues reviewing new warehouse opportunities.

Looking Ahead: More Disruption Expected

The transformation of Australia’s supermarket landscape is far from complete.

The ACCC noted that entry or expansion would more likely occur via differentiated offerings such as subscription warehouses like Costco, hard discounters like Aldi, or premium gourmet retailers.

Cost-of-living pressures continue driving consumers toward value. UBS analysis suggests both Coles and Woolworths will lose market share to Aldi, with Coles expected to suffer the most.

The growth of Costco and Aldi represents more than just two successful retailers. It signals a fundamental shift in how Australians approach grocery shopping.

Value, transparency, and simplicity are winning over brand loyalty and convenience.

Also Read: Two Gold Miners Just Created West Africa’s Next Billion-Dollar Powerhouse

Frequently Asked Questions

Q: How much market share do Costco and Aldi have in Australia?

A: Aldi holds approximately 9% of the Australian supermarket market. Costco holds about 1% of the grocery market, though this is growing rapidly.

Q: Why are Costco and Aldi so successful in Australia?

A: Both chains offer significantly lower prices than traditional supermarkets. Costco’s membership model and bulk buying power allow aggressive pricing, while Aldi’s everyday low price strategy and private label focus deliver consistent value.

Q: Will Costco open more stores in Australia?

A: Yes. Costco plans to open its 16th Australian warehouse in Pakenham, Victoria, by 2027. The company continues reviewing opportunities for additional locations.

Q: How do Coles and Woolworths respond to this competition?

A: Both chains are investing in refurbishments, enhancing online capabilities, and working to maintain price competitiveness while protecting margins.

Q: What’s the total size of Australia’s supermarket market?

A: The Australian supermarket and grocery sector was valued at approximately $199 billion in 2024.