Australia stands at a crossroads. The country that built its economy on digging iron ore from the ground now faces a question that could redefine its industrial future: Can it become a green steel powerhouse?

The numbers tell a compelling story. With over $5 billion committed to green steel projects across the nation, Australia isn’t just talking about decarbonisation. It’s betting the house on it.

But here’s the twist nobody expected: The same companies that profited from coal-fired blast furnaces are now racing to install electric arc furnaces. The competition is fierce, the stakes are enormous, and the global market is watching.

The Electric Arc Furnace Revolution Sweeps Australia

Green Steel of Western Australia is leading the charge with a $400 million recycling mill in Collie. This facility, scheduled to begin production in 2026, will convert scrap steel into rebar using electric arc furnace technology powered entirely by renewable energy.

Western Australia’s first steel mill forges ahead

The mill’s capacity? 450,000 tonnes of green rebar annually.

That’s just the beginning. GSWA has another project in the pipeline: a massive $2.5 billion Direct Reduced Iron plant near Geraldton. This facility will initially run on natural gas before transitioning to green hydrogen, positioning Western Australia as a potential export hub for green iron products.

Liberty Steel’s Whyalla operations tell a similar story. The company has ordered a 160-tonne electric arc furnace from Italian supplier Danieli, aiming to phase out coal-based steelmaking by 2025. The planned installation includes a 1.8 million tonne per annum Direct Reduction Plant designed to process local magnetite ore.

If successful, Whyalla could achieve a 90% reduction in direct CO2 emissions from steelmaking.

InfraBuild currently operates as Australia’s only electric arc furnace steel producer. The company recycles approximately 1.4 million tonnes of scrap metal annually across its Victorian facilities, demonstrating the viability of EAF technology in Australian conditions.

Francisco Irazusta, InfraBuild’s CEO, points to steel’s crucial role in infrastructure resilience and decarbonisation efforts as the industry reshapes itself for a lower-carbon future.

ASX Giants Join the Green Steel Race

BlueScope Steel (ASX: BSL) isn’t sitting idle. The company’s FY2025 sustainability report revealed significant climate action progress, though challenges remain in achieving net-zero targets by 2050.

Modern electric arc furnaces like those being installed across Australia can reduce steelmaking emissions by up to 90% when powered by renewable energy.

Modern electric arc furnaces like those being installed across Australia can reduce steelmaking emissions by up to 90% when powered by renewable energy.

The company’s strategy focuses on Direct Reduced Iron technology using natural gas as a transitional pathway before switching to green hydrogen. BlueScope executives believe DRI represents “the most prospective technology” for decarbonising Australian steelmaking operations.

But BlueScope faces a dilemma. The Port Kembla blast furnace reaches end-of-life later this decade. Management previously indicated plans to reline the furnace for another 15-20 years rather than switching immediately to scrap-EAF technology.

That decision drew criticism from environmental analysts who argue Australia should move faster on decarbonisation.

Enter the NeoSmelt collaboration. In a groundbreaking partnership, Rio Tinto (ASX: RIO), BHP (ASX: BHP), and BlueScope announced plans to develop Australia’s first ironmaking electric smelting furnace pilot plant.

The pilot facility will be located in Western Australia’s Kwinana Industrial Area. If successful, it could demonstrate that production of molten iron from Pilbara ores is feasible using renewable power combined with DRI process technology.

Woodside Energy has joined the consortium as an energy supplier, subject to finalising commercial arrangements. The Western Australian government committed $75 million to support the project.

Tania Archibald, BlueScope’s Chief Executive Australia, described the collaboration as “truly transformative” for steel industry decarbonisation efforts.

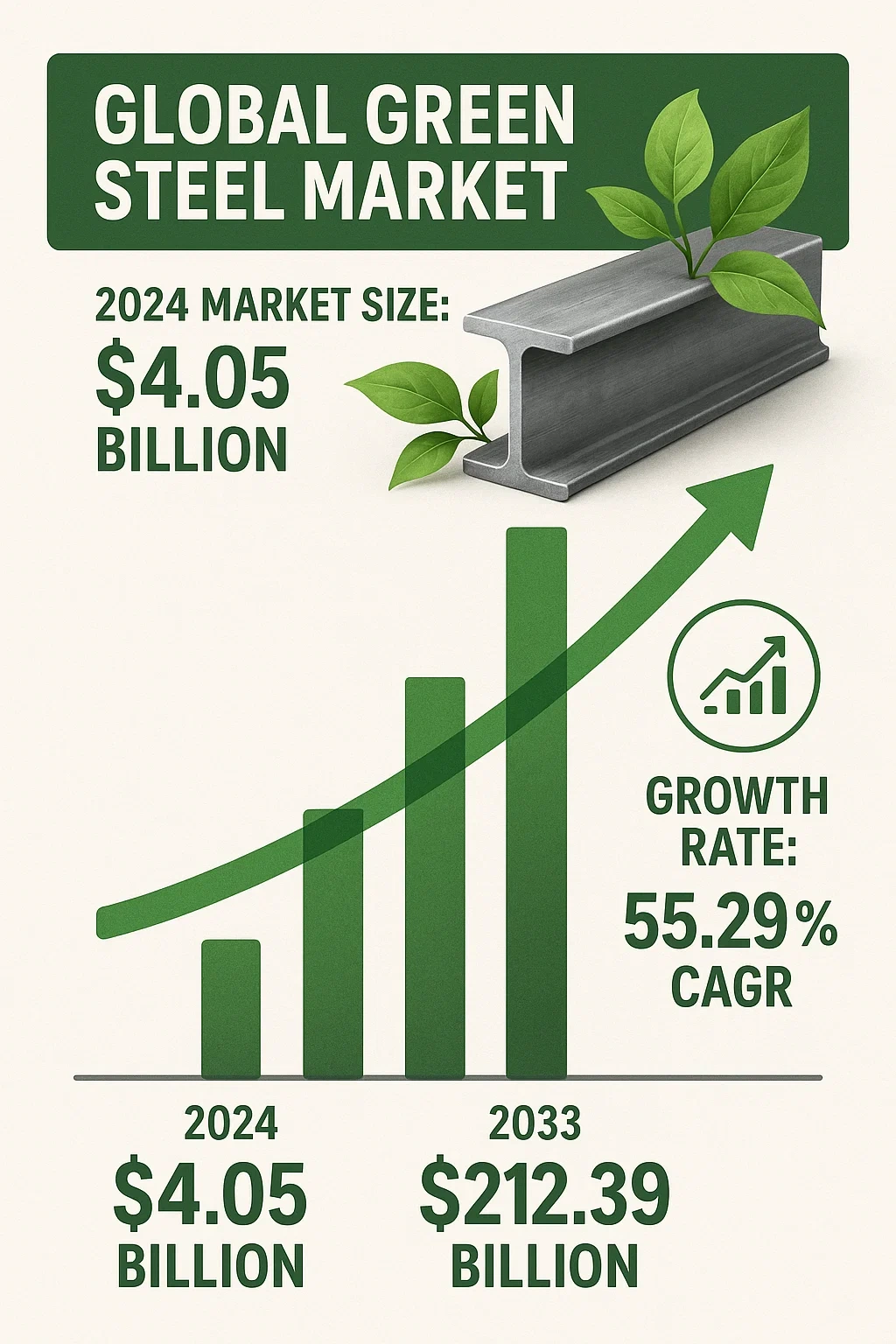

The Global Green Steel Market Explodes

The timing couldn’t be better. Global green steel market forecasts show explosive growth.

That’s not a typo. The market is expected to grow more than fifty-fold in less than a decade.

Europe currently dominates with 39.6% market share, but Asia Pacific follows closely with 32.2%. North America represents the fastest-growing region, with automotive manufacturers driving demand for low-carbon steel.

The automotive sector alone accounts for 39.2% of green steel consumption. As electric vehicle production accelerates globally, demand for specialised steel grades continues rising.

Construction represents another massive opportunity. Green building certifications like LEED and BREEAM increasingly require low-carbon materials, creating sustained demand for green steel in infrastructure projects.

Australia’s iron ore exports earned over $100 billion in 2023-24. The question now: Can Australia capture a meaningful share of the green steel export market?

Export Potential: Australia’s Competitive Advantages

Australia possesses several natural advantages for green steel production:

- Abundant magnetite resources – Approximately 24,251 million tonnes of economic demonstrated resources suitable for electric arc furnace processing.

- Renewable energy capacity – South Australia achieved 99.8% renewable supply over a seven-day period in October 2024, demonstrating grid readiness for energy-intensive steelmaking.

- Established infrastructure – Decades of iron ore mining created world-class logistics networks, deep-water ports, and skilled workforce availability.

- Trading relationships – Australia holds 56% of the Asian iron ore market, providing established customer relationships for potential green steel exports.

Christmas Creek is the second mine in Fortescue’s Chichester Hub

Fortescue’s Christmas Creek operations plan to produce 1,500 tonnes of green iron using hydrogen by year-end 2025. The company describes its approach as “pit to product” – integrating renewable energy, green hydrogen production, and iron processing in a single location.

Production costs remain a challenge. Studies by the Minerals Research Institute of Western Australia indicate that scaling power facilities for 1 million tonnes of crude steel capacity requires approximately $5.6 billion in solar, wind, and battery infrastructure.

That’s more than the combined investment needed for pelletising, DRI plants, and electric arc furnaces.

The Economic Reality Check

Rio Tinto’s chief technical officer Mark Davies delivered a sobering assessment at the International Mining and Resources Conference: “There is no economic incentive at the moment for hydrogen direct reduced iron production.”

Davies specifically identified carbon pricing as the missing piece. A carbon price of “a couple hundred dollars” would be necessary to create genuine economic incentives for green steel production in Australia.

Without such mechanisms, the cost differential between conventional and green steel remains prohibitive.

The Australian government has responded with significant funding:

- Future Made in Australia innovation fund: $1.7 billion

- Green Iron Investment Fund: $1 billion

- Green Metals Foundational Incentives: $18.1 million over six years

- Additional value-added resources support: $650 million

These programs support everything from pilot projects to commercial-scale facilities. Liberty Steel Australia secured $63.2 million from federal government and $50 million from South Australia for its Whyalla EAF installation.

The question remains whether government support can bridge the economic gap until carbon pricing mechanisms make green steel commercially competitive.

Technology Challenges and Solutions

Electric arc furnace technology is proven. Scrap-EAF powered by renewables provides a zero-carbon route that’s already cost-competitive in many markets.

The challenge? Australia produces limited scrap steel relative to global leaders. Unlike Europe where scrap-EAF accounts for significant production, Australian steelmakers historically relied on blast furnace routes.

Direct Reduced Iron technology offers an alternative pathway. By using natural gas initially and transitioning to green hydrogen, DRI-EAF can process iron ore directly without requiring large scrap volumes.

The technology isn’t commercially proven at massive scale yet. BlueScope’s investments in testing and development total $300-400 million through 2030, reflecting the substantial capital required for technology validation.

Hydrogen production presents another hurdle. Green hydrogen from renewable-powered electrolysis remains expensive compared to fossil fuel alternatives. South Australia’s planned 250 megawatt green hydrogen plant aims to use excess renewable energy that would otherwise be curtailed.

Using renewable power that would be wasted means the hydrogen could be competitively priced. But scaling to industrial volumes requires massive infrastructure investment.

Global Competition Intensifies

Australia isn’t alone in pursuing green steel opportunities. Sweden’s Stegra (formerly H2 Green Steel) has emerged as the global leader, with projects planned in Portugal, Brazil, and Canada.

Australian iron ore faces growing competition in the emerging green iron market

Notably, Australia doesn’t appear on Stegra’s expansion list. The company specifically seeks locations with “abundant access to renewable electricity and strong grid connections” combined with high-grade iron ore.

South Australia meets these criteria theoretically. Yet concerns about potential reliance on natural gas and carbon capture technology may have discouraged Stegra’s interest.

Canada’s green steel initiatives benefit from 94% hydro and 5% wind power grids. Brazil offers similar renewable advantages plus high-grade iron ore. Both countries present formidable competition for Australian projects.

China continues massive steel overcapacity issues, producing far more than domestic demand requires. Chinese subsidies run ten times higher than OECD countries, encouraging continued investment in capacity even when uneconomic.

This global oversupply creates persistent downward pressure on steel prices and profitability, making the premium pricing needed for green steel more difficult to achieve.

The Verdict: Can Australia Win?

Australia’s green steel race isn’t guaranteed to succeed. Economic challenges, technology risks, and fierce global competition create substantial headwinds.

But the country possesses genuine advantages. Abundant iron ore, world-leading renewable energy penetration in key states, established infrastructure, and strong trading relationships provide a foundation.

The $5 billion committed to green steel projects demonstrates serious intent. Major ASX companies including BlueScope, BHP, and Rio Tinto are investing significant capital and expertise in decarbonisation pathways.

Success depends on several factors aligning:

- Carbon pricing mechanisms creating economic incentives for green steel production and consumption.

- Technology validation proving DRI-EAF pathways work commercially at scale with Australian ores.

- Infrastructure development delivering renewable energy and green hydrogen at competitive costs.

- Market development establishing demand for Australian green steel exports in Asian markets.

- Policy consistency maintaining government support through multi-year development cycles.

If these pieces fall into place, Australia could capture meaningful share of a market growing from $6 billion to over $200 billion by 2033.

That’s the export revolution nobody saw coming. And it’s already underway.

Also Read: Australia’s Biggest Telco Slapped with $18 Million Penalty in Speed Scandal

Frequently Asked Questions

Q: What is green steel?

A: Green steel is produced using environmentally sustainable processes that minimise carbon emissions. This typically involves electric arc furnaces powered by renewable energy, with inputs from either scrap metal or iron ore processed using green hydrogen instead of coal.

Q: Why is Australia pursuing green steel?

A: Australia’s $100+ billion iron ore export industry faces long-term risks as global steelmakers decarbonise. By developing green steel production capabilities, Australia can capture value-added opportunities and secure future demand for its mineral resources.

Q: How much will green steel projects cost?

A: Major Australian projects range from $400 million (Green Steel WA’s Collie mill) to $2.5 billion (GSWA’s Geraldton DRI plant). The NeoSmelt pilot plant in Western Australia received $75 million in state government support, with total project costs yet to be disclosed.

Q: When will Australian green steel reach export markets?

A: Initial production timelines vary by project. Green Steel WA targets 2026 for its Collie mill. Liberty Steel’s Whyalla EAF aims for 2025 completion. The NeoSmelt pilot plant expects first operations in 2028.

Q: What are electric arc furnaces?

A: Electric arc furnaces use electric arcs to melt scrap steel or direct reduced iron. When powered by renewable energy, they can produce steel with minimal carbon emissions compared to traditional coal-fired blast furnaces.