When BHP announced an $840 million capital injection into Olympic Dam, the timing couldn’t have been more strategic. Just weeks after Indonesia’s Grasberg mine—the world’s second-largest copper producer—ground to a halt following a catastrophic mudslide, Australia’s mining giant positioned itself as the reliable supplier the world desperately needs.

This isn’t just another mining investment. It’s a calculated response to a global copper crisis that’s pushing prices to 16-month highs and exposing the fragility of concentrated supply chains.

The $840 Million Blueprint for Copper Dominance

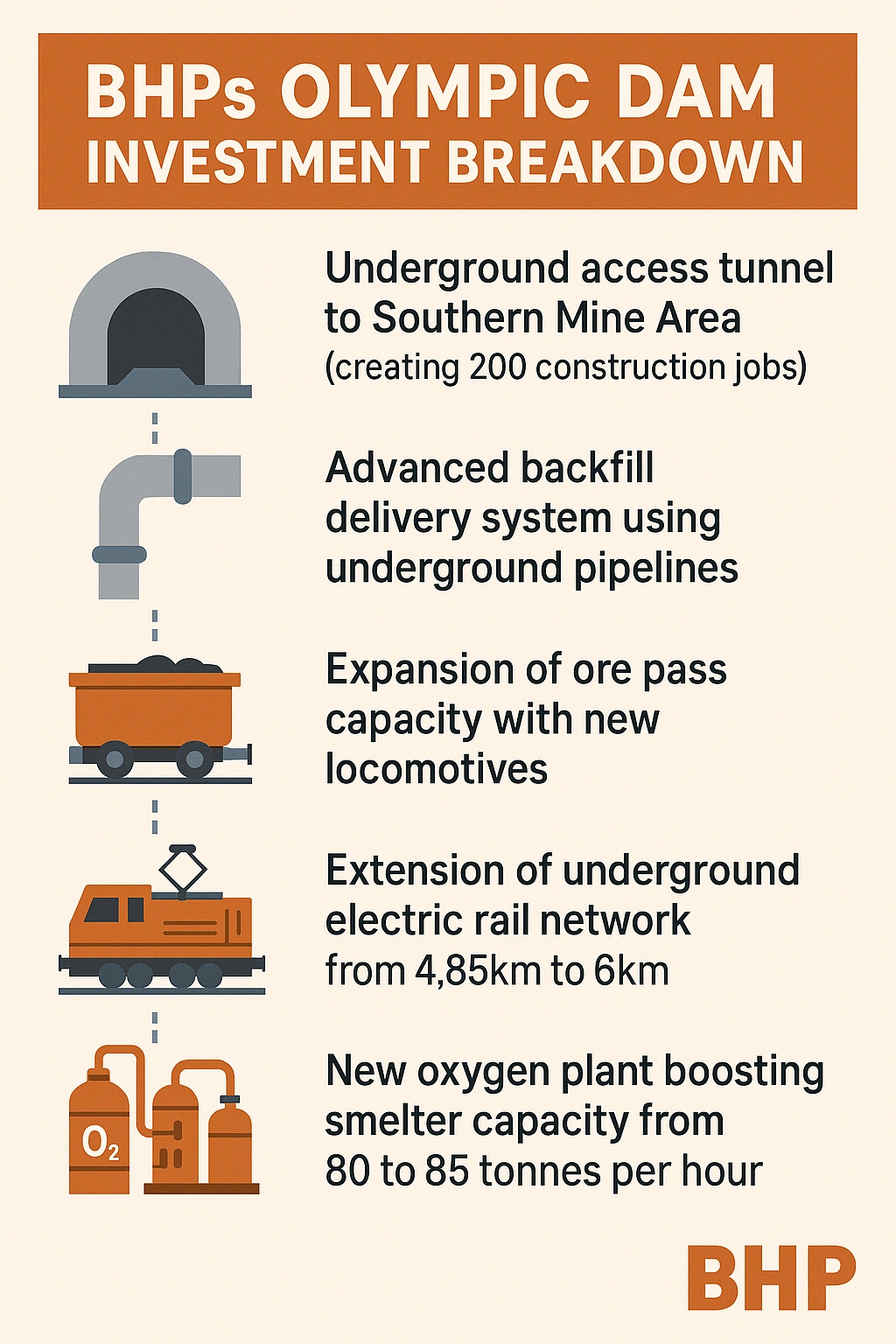

BHP’s investment package targets four critical areas that will fundamentally reshape Olympic Dam’s operational capacity. The centrepiece is a new underground access tunnel into the Southern Mine Area, unlocking previously untapped sections of one of the world’s most valuable polymetallic deposits.

The oxygen plant alone represents a 6.25% jump in processing capability. That might seem modest on paper, but at Olympic Dam’s scale, it translates to thousands of additional tonnes of refined copper annually.

Edgar Basto, BHP’s chief operating officer, framed the ambition clearly: “We expect to grow our copper base from 1.7 million tonnes to around 2.5 million tonnes per annum.”

Global Supply Crunch Creates Perfect Storm

The copper market entered crisis mode in September 2025 when Freeport-McMoRan declared force majeure at Grasberg following the deadly mudslide. The incident—which involved 800,000 metric tonnes of mud flooding underground levels—immediately removed 3% of global copper supply from markets.

Freeport’s guidance paints a sobering picture: no significant Grasberg production through Q4 2025, limited output through 2026, with normal levels not returning until 2027.

Goldman Sachs responded by slashing its 2025 global copper forecast, pushing the market from a projected surplus of 105,000 tonnes into a deficit of 55,000 tonnes. By 2026, they expect a shortfall of 200,000 tonnes.

Copper prices reacted predictably. London Metal Exchange three-month futures jumped to $10,485 per tonne—the highest level since May 2024. Spot prices in some Asian markets topped $11,000.

The disruption exposed uncomfortable truths:

- Supply is increasingly concentrated in geopolitically complex regions

- Ageing mines face declining ore grades and operational challenges

- New projects take 10-15 years from discovery to production

- Climate-related disruptions are accelerating (mudslides, water shortages, extreme weather)

This context transforms BHP’s Olympic Dam investment from routine capital expenditure into strategic positioning. While competitors scramble to address supply gaps, BHP is methodically expanding capacity at a tier-one asset in a politically stable jurisdiction.

Australia’s Copper Advantage Strengthens

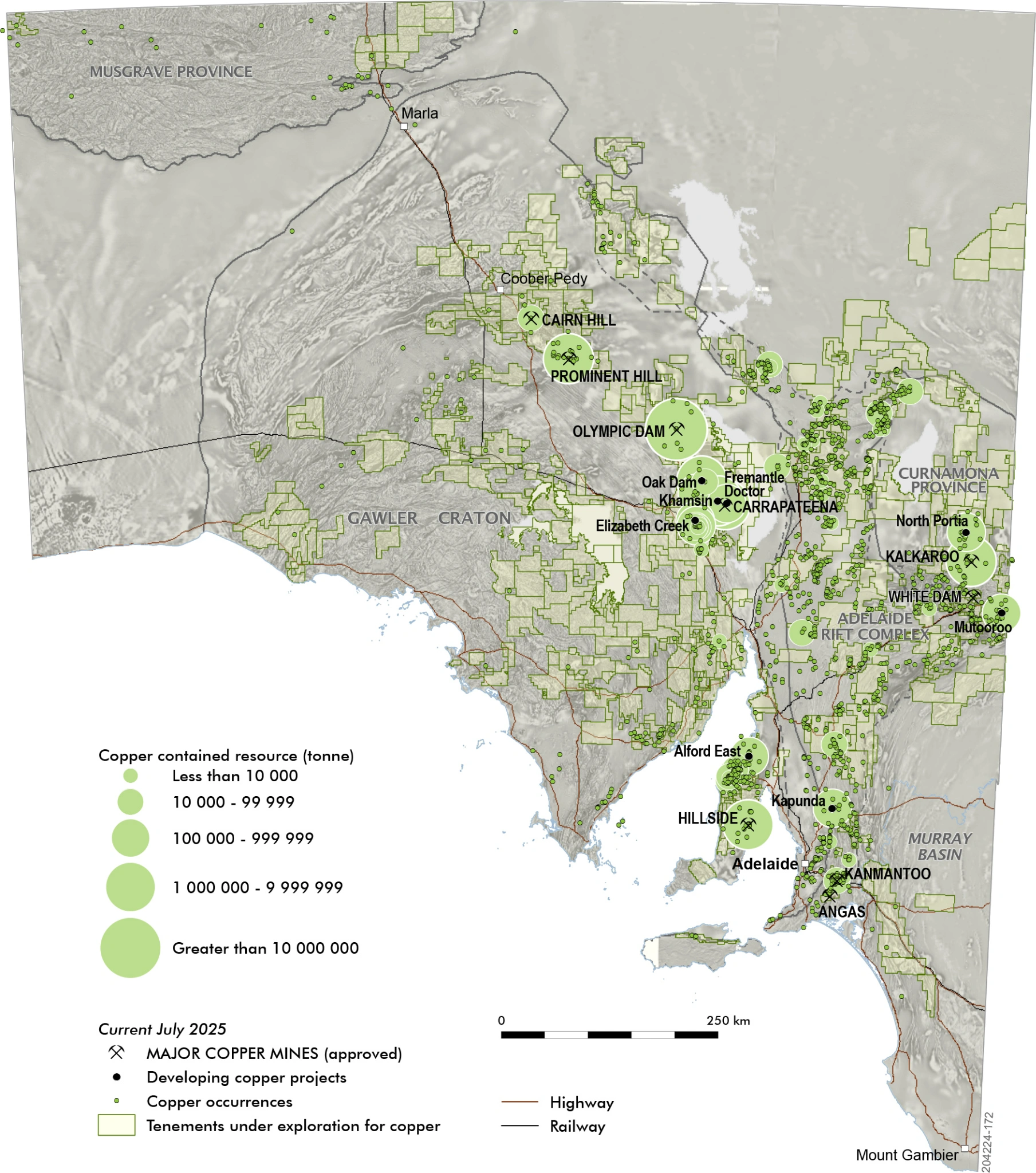

South Australia holds approximately two-thirds of Australia’s demonstrated copper resources. That geological endowment, combined with established infrastructure and skilled workforce, creates advantages competitors struggle to replicate.

Australia ranks third globally for copper reserves at 100 million metric tonnes, behind Chile and Peru. But unlike those nations, Australia offers political stability, established rule of law, and lower sovereign risk—factors increasingly valued by global manufacturers.

Olympic Dam itself represents one of the world’s largest copper-uranium-gold deposits. The mine has consistently delivered over 300,000 tonnes of copper annually for three consecutive years. BHP’s Copper South Australia division—which includes Olympic Dam, Prominent Hill, and Carrapateena—produced 316,000 tonnes in FY25.

BHP’s copper strategy increasingly defines the company’s future. Copper generated 45% of underlying earnings in FY25, up from less than 30% five years ago. This shift reflects management’s recognition that copper offers better long-term growth prospects than iron ore.

Premier Peter Malinauskas captured the strategic significance during the October announcement: “South Australia is at the epicentre of copper. BHP realises that, which is why it’s investing billions of dollars in South Australia.”

Map showing South Australia’s major copper occurences

The 2027 Production Target and What It Means

BHP’s timeline reveals a carefully sequenced expansion strategy. The underground tunnel project begins immediately, with construction jobs ramping up through early 2026. The backfill system installation runs parallel, enabling access to previously unreachable ore zones.

The extended rail network and new locomotives should be operational by mid-2026, reducing truck haulage distances and improving safety metrics. The oxygen plant—critical for smelter debottlenecking—targets commissioning in late 2026.

This phased approach serves multiple purposes:

- Minimizes operational disruption during construction

- Allows testing and optimization at each stage

- Spreads capital expenditure across fiscal years

- Builds workforce capacity gradually rather than creating labour bottlenecks

By 2027, these projects collectively should position Olympic Dam to sustainably produce at higher rates while maintaining or improving cost structures.

The broader Copper South Australia expansion plans are even more ambitious. BHP is progressing studies for a major smelter and refinery expansion that could boost copper cathode production from 200,000 tonnes to 650,000 tonnes annually—more than tripling current capacity.

That decision point comes in 2028, according to updated guidance. Whether BHP proceeds depends heavily on energy costs, regulatory approvals, and sustained copper prices above $9,500 per tonne.

Regional Economic Impact Beyond the Headlines

The $840 million investment creates approximately 250 construction and operational jobs directly. But the multiplier effects run deeper through South Australia’s economy.

Mining suppliers, contractors, accommodation providers, and service businesses all benefit from sustained activity at Olympic Dam. The mine’s location 560km north of Adelaide creates economic activity across regional centres including Roxby Downs, Port Augusta, and Whyalla.

BHP’s South Australian assets generated $1.9 billion in earnings (measured in US dollars) in FY25, up from $1.6 billion the previous year. That increase came despite softer copper prices for most of the period, highlighting improved operational efficiency.

South Australia collected over $4.3 billion in copper-related export earnings in 2024, making it the state’s largest mineral export by value. Government projections suggest copper could surpass iron ore in national economic contribution within five years as energy transition demand accelerates.

Demand Drivers: Why Copper’s Golden Age Is Just Beginning

Global copper demand is forecast to grow 40% by 2040, driven by three megatrends that show no signs of slowing:

- Electrification of transport: Electric vehicles require approximately 80kg of copper per unit compared to 20kg in conventional vehicles. With EV sales projected to reach 30 million units annually by 2030, that’s an additional 1.8 million tonnes of annual copper demand from this sector alone.

- Renewable energy infrastructure: Solar installations need 5.5 tonnes of copper per megawatt. Wind turbines demand up to 4.7 tonnes per megawatt. As countries race toward net-zero targets, renewable capacity additions are accelerating globally.

- Grid infrastructure and AI data centres: The digitalisation boom creates copper-intensive demand. Data centres require extensive copper for power distribution, cooling systems, and connectivity. Next-generation AI facilities are even more copper-intensive than traditional server farms.

India is emerging as a particularly important growth market, with the International Copper Association forecasting 7% compound annual growth rate through 2040—the highest of any major economy.

These structural demand drivers underpin copper’s long-term investment thesis. Unlike iron ore, which faces declining demand from China’s infrastructure slowdown, copper’s applications are diversifying and expanding.

What This Means for Investors and Markets

BHP shares (ASX: BHP) responded modestly to the October announcement, reflecting the market’s focus on near-term earnings over long-term strategic positioning. However, the investment signals management confidence in copper’s trajectory.

The company’s copper production grew 28% over three years through FY25, reaching 2 million tonnes for the first time. With Olympic Dam expansion, Escondida optimisation in Chile, and potential Resolution mine development in Arizona, BHP is positioning to maintain its crown as the world’s largest copper producer.

Key metrics investors should watch:

- Olympic Dam production rates (quarterly reporting)

- Copper price sustainability above $9,500 per tonne

- Capital expenditure efficiency versus guidance

- 2028 decision on major smelter expansion

- Australian energy policy developments (critical for processing economics)

Analysts at BMO Capital Markets maintain that BHP’s diversified production base—60% from North and South America—provides downside protection even if Olympic Dam expansion faces delays.

The bigger strategic question centres on whether Australia can maintain competitive energy costs. As BHP CEO Mike Henry warned recently, Australian electricity prices running 50-100% above US equivalents threaten long-term competitiveness in energy-intensive processing activities.

The Verdict: Strategic Necessity, Not Optional Growth

BHP’s $840 million Olympic Dam investment isn’t a bet on short-term copper prices. It’s recognition that the world needs reliable, ethically-sourced copper from politically stable jurisdictions—and that window of opportunity won’t stay open indefinitely.

The Grasberg disaster demonstrated how quickly supply can vanish. Chile faces ongoing water access challenges and community tensions. Peru battles political instability. The DRC carries execution risk and governance concerns.

Australia offers something increasingly rare in mining: predictability. Projects can be developed without nationalisation fears, expropriation risks, or sudden regulatory reversals.

For South Australia, the investment cements its position as Australia’s copper heartland. For BHP, it’s the foundation of a strategy to dominate copper production through the energy transition.

The real test comes in 2028 when BHP must decide whether to commit multi-billions to the smelter expansion. That decision will reveal whether management truly believes copper’s structural bull market is sustainable—or whether this represents the peak of the cycle.

Either way, the $840 million down payment is now locked in. The countdown to 2027 production ramp-up has begun.

Also Read: AI-Powered Commodities Trading: How Machine Learning is Shaping Metal Futures Markets

FAQs

1.How long will BHP’s Olympic Dam expansion take to complete?

The $840 million investment follows a phased timeline through 2027. The underground tunnel construction begins immediately with initial production access by late 2026. The oxygen plant should be operational by end of 2026, with full benefits flowing through 2027 as all systems integrate.

2.Why is Olympic Dam important for global copper supply?

Olympic Dam is one of the world’s largest copper deposits with decades of remaining mine life. Unlike many copper operations, it’s located in a politically stable jurisdiction with established infrastructure. With Grasberg offline until 2027, Olympic Dam becomes increasingly critical for reliable supply to global markets.

3.Will this investment impact copper prices?

Not immediately. The additional production capacity comes online gradually through 2027. However, it signals to markets that BHP is confident in long-term copper demand, which could support price floors. The bigger price impact comes from current supply deficits rather than future production additions.

4.How does Australia’s copper industry compare globally?

Australia ranks third worldwide for copper reserves (100 million metric tonnes) and produced 800,000 tonnes in 2024. South Australia alone holds two-thirds of national reserves. Australian copper operations benefit from higher ore grades (1.6% vs 0.7% global average), political stability, and established infrastructure—advantages that command premium valuations.

5.What are the main risks to BHP’s copper expansion plans?

Energy costs represent the primary risk. Australian electricity prices running 50-100% above US equivalents threaten processing economics. Other risks include regulatory changes, community relations, water availability for operations, and potential copper price corrections if global growth disappoints.