Australia’s Treasury released the eagerly anticipated Final Budget Outcome (FBO) for 2024/25, delivering a fiscal picture that surprised many economists. The actual deficit came in significantly better than initial forecasts, though it marked a decisive shift from the previous year’s surplus.

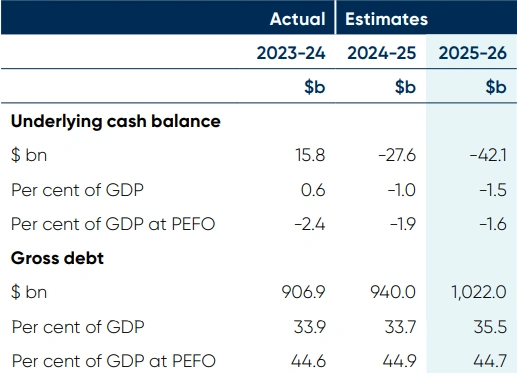

The government recorded a deficit of $27.6 billion for the 2024-25 financial year, representing 1% of GDP. While this marks a return to deficit territory after two consecutive surpluses, the outcome proved far superior to the $47.1 billion shortfall projected at the Pre-Election Economic and Fiscal Outlook (PEFO).

The Numbers That Tell the Story

The FBO reveals several key shifts from budget forecasts released throughout the year.

Final Budget Outcome 2024-25 vs Initial Projections

Revenue collections reached $734.2 billion, driven primarily by stronger-than-expected company tax receipts and elevated income tax revenue. This represented a $12.3 billion improvement compared to the Mid-Year Economic and Fiscal Outlook (MYEFO) projections from December 2024.

Total expenses climbed to $761.8 billion, reflecting increased spending on:

- Cost-of-living relief measures ($8.4 billion)

- Healthcare system pressures ($6.7 billion)

- Defence capability enhancements ($4.2 billion)

- Natural disaster response and recovery ($3.8 billion)

The fiscal improvement of nearly $20 billion compared to PEFO demonstrates how quickly economic conditions can shift governmental finances.

Mining Sector Impact

The mining sector’s performance played a crucial role in shaping the final outcome.

Despite earlier warnings of a $100 billion downturn in mining export earnings, commodity prices held up better than anticipated throughout the fiscal year. Iron ore averaged $148 per tonne, while coal prices remained elevated amid continued global energy security concerns.

The Resources Minister noted that mining royalties contributed an additional $4.8 billion beyond forecasts, providing critical budget support during a challenging economic period.

Labour Market Resilience

Employment growth exceeded expectations, with over 285,000 new jobs created during 2024-25.

The unemployment rate averaged 4.1%, lower than the 4.5% forecasted in the May 2024 Budget. This labour market strength translated directly to higher income tax receipts, contributing approximately $7.2 billion more than projected.

Participation rates reached record levels at 67.3%, with women’s workforce engagement hitting all-time highs. These employment trends supported consumer spending and helped maintain economic momentum despite headwinds.

Inflation’s Double-Edged Sword

Inflation moderated faster than anticipated, returning to the Reserve Bank’s 2-3% target band by December 2024.

The Consumer Price Index averaged 2.8% for the financial year, down from 4.1% in 2023-24. This decline eased cost pressures on households and businesses while reducing some government expenditure indexed to inflation.

However, the inflation trajectory influenced several key budget areas. Interest payments on government debt came in $2.1 billion lower than forecast as bond yields declined more rapidly than expected.

Energy bill rebates provided to all households and eligible small businesses totalled $3.5 billion, directly contributing to the inflation decline while adding to expenditure.

GDP Growth and Economic Performance

Economic growth proved more resilient than pessimistic forecasts suggested.

Real GDP expanded 1.8% over the fiscal year, slightly ahead of Treasury’s 1.75% projection. The June quarter delivered a particularly strong 0.6% quarterly increase, driven by:

- Household consumption growth of 0.9%

- Improved trade performance

- Government infrastructure spending

- Services sector recovery

Per capita GDP remained weak, however, growing just 0.3% as population growth from migration continued to outpace economic expansion.

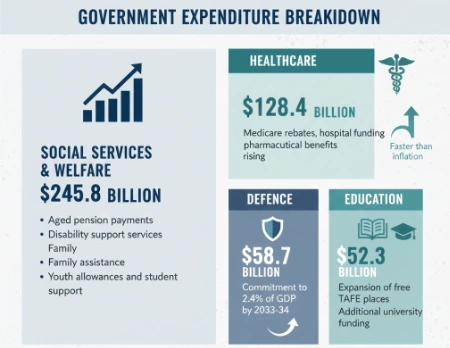

Where the Money Went

Social services and welfare consumed the largest share of expenditure at $245.8 billion, including:

- Aged pension payments

- Disability support services

- Family assistance

- Youth allowances and student support

Healthcare spending reached $128.4 billion, with Medicare rebates, hospital funding, and pharmaceutical benefits scheme costs all rising faster than inflation.

Defence expenditure climbed to $58.7 billion, reflecting the government’s commitment to raising defence spending to 2.4% of GDP by 2033-34.

Education funding totalled $52.3 billion, including the expansion of free TAFE places and additional university funding announced during the year.

Debt and Interest Costs

Net debt rose to $556 billion, or 19.9% of GDP, up from $501 billion at June 2024.

This increase was lower than projected due to the improved underlying cash balance. Gross debt reached $940 billion, still well below many comparable developed economies.

Interest payments on government debt totalled $27.8 billion, representing 3.8% of total expenditure. The weighted average interest rate on Commonwealth Government Securities fell to 2.96%, reflecting earlier issuance at lower rates.

Credit rating agencies maintained Australia’s AAA rating, with stable outlooks across all three major agencies.

Policy Measures That Made a Difference

Several key policy decisions influenced the final outcome.

Stage 3 tax cuts, which commenced July 2024, cost $20.7 billion for the full financial year. These cuts delivered relief to 13.6 million Australian taxpayers while reducing revenue collections.

The Energy Bill Relief Fund extended for an additional year provided $300 per household in electricity bill credits. This measure cost $3.5 billion but helped moderate inflation by 0.75 percentage points.

Commonwealth Rent Assistance increased by 15%, providing additional support to 1.2 million renters at a cost of $2.8 billion. This represented the largest increase in more than 30 years.

The Future Made in Australia initiative saw initial outlays of $1.9 billion, supporting clean energy manufacturing, critical minerals processing, and green hydrogen development.

State and Territory Transfers

GST distributions to states and territories totalled $88.6 billion, with the ‘no-worse-off’ guarantee adding $6.8 billion to support Western Australia’s transition to a new distribution formula.

Infrastructure grants reached $14.2 billion, funding projects including:

- Urban rail developments

- Road upgrades

- Water security projects

- Regional connectivity improvements

Health funding transfers to states climbed to $32.4 billion under various hospital funding agreements.

Looking Forward

The FBO provides crucial baseline data for future budgetary planning.

With the 2025-26 Budget projecting a $42.1 billion deficit, fiscal consolidation remains challenging. The government faces competing pressures to maintain essential services while managing debt levels.

Treasury forecasts suggest deficits will persist throughout the medium term, with surpluses not returning until 2034-35 under current policy settings.

FAQs

1.What is the Final Budget Outcome?

The Final Budget Outcome is the government’s official report on actual revenue and expenditure for the completed financial year, replacing earlier estimates and forecasts.

2.Why was the 2024-25 deficit smaller than forecast?

Stronger commodity prices, resilient employment, and lower interest costs contributed to a $19.5 billion improvement compared to pre-election forecasts.

3.How does this compare to previous years?

The $27.6 billion deficit followed surpluses of $22.1 billion (2022-23) and $15.8 billion (2023-24), marking a return to deficit but at a much lower level than projected.

4.What drove the revenue improvements?

Higher company tax receipts from mining, stronger income tax collections from employment growth, and elevated GST revenue from consumer spending all contributed.

5.When will Australia return to surplus?

Current forecasts don’t project a return to surplus until 2034-35, though this depends heavily on global economic conditions and policy decisions.