Winning a massive Powerball jackpot presents winners with financial decisions that could reshape their entire future. However, the payout options available depend entirely on which version of Powerball you’re playing – and the differences are more significant than most people realise.

For Australian players, understanding how Powerball prize payouts work becomes crucial when jackpots reach extraordinary heights. Recent draws have pushed prizes beyond $200 million, making payout knowledge essential for strategic play.

Australian Powerball: Lump Sum Only

Australian Powerball operates fundamentally differently from its American counterpart when it comes to prize distribution. Winners always collect in lump sum parimutuel winnings, meaning there’s no annuity option available for Australian players.

When you win Australian Powerball, you receive the entire advertised jackpot amount immediately. The $200 million record jackpot shared by two winners in February 2024 was paid out in full, with each winner receiving $100 million upfront.

Key features of Australian Powerball payouts:

- Immediate lump sum payment only

- Full advertised amount paid out

- Tax-free winnings for Australian residents

- No federal or state deductions

- Money available for immediate investment or use

International Powerball: The Lump Sum vs Annuity Decision

International lotteries, particularly US Powerball, offer winners a critical choice between two payout methods that can dramatically affect your total winnings.

The Annuity Option

The annuity option provides one immediate payment, followed by 29 annual payments that increase by 5% each time until the full advertised jackpot is reached over 30 years.

| Annuity advantages | Annuity disadvantages |

| ● Guarantees the full advertised jackpot amount

● Built-in inflation protection through 5% annual increases ● Provides long-term financial security ● Reduces temptation for impulsive spending ● Offers steady income stream for three decades |

● Money tied up for 30 years

● Limited immediate investment opportunities ● Inflation may outpace the 5% increases ● Estate planning complications |

The Lump Sum Option

The cash value payout is about 52 percent of the total jackpot amount before taxes, providing immediate access to a substantial but reduced prize.

| Lump sum advantages | Lump sum disadvantages |

| ● Immediate access to full available cash

● Maximum investment flexibility ● No long-term payment uncertainties ● Can potentially earn higher returns than annuity growth rate |

● Significantly less money upfront (typically 50-60% of advertised amount)

● Higher immediate tax burden ● Greater risk of mismanagement ● No guaranteed future payments |

Tax Implications on Lottery Wins: A Critical Factor

The taxation landscape creates a stark contrast between Australian and international lottery wins.

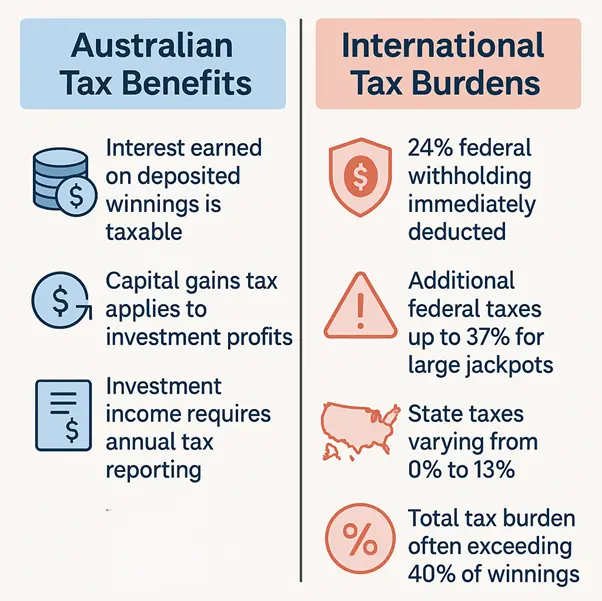

Australian residents face zero taxes on lottery winnings, classified as “windfall gains” by the Australian Taxation Office (ATO). This means every dollar of a $200 million jackpot stays in your pocket. US Powerball winners face substantial taxation regardless of payout choice.

Tax implications comparison between Australian and US lottery winnings.

When to Choose Lump Sum vs Annuity

Virtually everybody who wins the lottery picks the lump-sum distribution, but financial experts suggest this isn’t always optimal.

Lump Sum Makes Sense When:

- You have strong financial discipline

- Professional investment team available

- You can consistently earn more than the annuity’s assumed 4.3% return

- Immediate major purchases needed (debt elimination, property)

- Advanced age makes 30-year payments impractical

Annuity Preferred When:

- Concerns about overspending exist

- Limited financial infrastructure to manage large sums

- Desire for guaranteed income protection

- Long-term wealth preservation concerns

- Estate planning complexities with large lump sums

Investment Strategy Considerations

The critical ingredient is financial discipline from both budgeting and investment standpoints. Professional lottery winner management typically involves three strategic “buckets”:

Lifestyle Bucket

Covers annual living expenses through capital preservation investments:

- Government and municipal bonds

- High-yield savings accounts

- Money market funds

- Interest-based income generation

Growth Bucket

Focuses on capital appreciation through:

- Diversified stock portfolios

- Real estate investments

- Commodities exposure

- Critical minerals and mining opportunities

Legacy Bucket

Designated for family transfers and charitable giving:

- Estate planning vehicles

- Trust structures

- Tax-efficient gifting strategies

Working with a financial advisor to help manage your money is the best way to ensure your money lasts for years to come, particularly for winners unfamiliar with large-scale investment management.

Professional Team Assembly

Lottery winners require immediate professional support across multiple disciplines:

Essential team members:

- Certified financial planner for investment strategy

- Tax specialist for jurisdiction-specific implications

- Estate planning attorney for wealth protection

- Chartered accountant for ongoing compliance

Building a team of experts is typically recommended before claiming major prizes, allowing for strategic claiming approaches including trust structures for privacy protection.

Common Pitfalls to Avoid

The average lottery winner comes from a socioeconomic background where they usually don’t have the infrastructure set up to handle massive payouts.

Frequent mistakes include:

- Immediate lifestyle inflation without budgeting

- Poor investment decisions due to inexperience

- Inability to refuse financial requests from others

- Inadequate tax planning leading to penalties

- Lack of estate planning for wealth preservation

The Bottom Line

Powerball lump sum vs annuity decisions fundamentally depend on your financial sophistication, age, and long-term goals. Australian players enjoy the simplicity of tax-free lump sum payments, while international lottery winners face complex taxation and payout choice considerations.

For Australian residents, the tax advantages make lottery winning particularly attractive, with every dollar remaining in your possession. However, the responsibility for investment management and long-term financial planning rests entirely with the winner.

Key takeaways:

- Australian Powerball offers lump sum only (tax-free)

- International lotteries provide choice but with heavy taxation

- Financial discipline determines long-term success regardless of payout method

- Professional guidance is essential for major wins

- Investment planning should begin before claiming prizes

Understanding how Powerball cash option vs annuity works empowers players to make informed decisions should fortune smile upon them. Whether facing a $200 million Australian jackpot or a billion-dollar US prize, the fundamentals of disciplined financial management remain the same.