Canadian gold and critical mineral miners listed on the CSE and TSXV exchanges are navigating dual market forces in 2025. These companies face increasing safe-haven demand for gold alongside surging supply chain requirements for critical minerals. The convergence creates unprecedented opportunities for diversified mining operations across Canada’s leading junior exchanges. The mining sector directly employs 430,000 workers across Canada while supporting 281,000 indirect positions throughout the supply chain. Total employment reaches 711,000 jobs, contributing $159 billion to the national GDP.

Market Dynamics Drive Dual Demand Patterns

Gold Reaches Historic Performance Levels

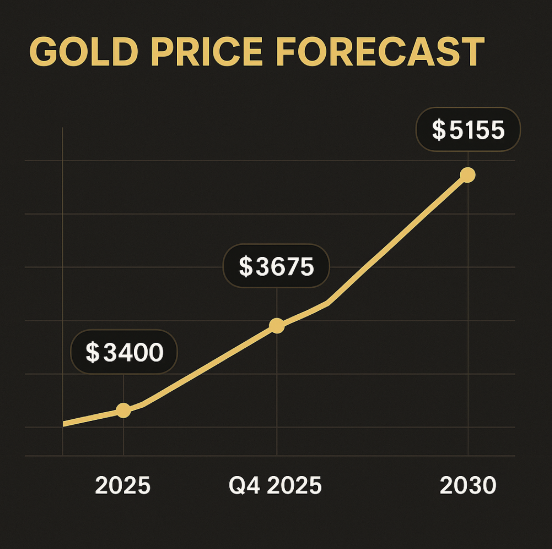

Gold rose by 26% points by mid-2025 to historic levels of over 3400 dollars per ounce. According to the World Gold Council, 40% is the potential annual increase in the event of bullish projections to take place in 2025. JPMorgan Research forecasts that prices will average out to $3,675 a troy ounce by the fourth quarter of 2025. Hence, HSBC has increased its projection of the average price in 2025 to 3,215 dollars per ounce and that of 2026 to 3,125 dollars per ounce. Gold appears bullish short-term and, in long-term forecasts, shows that the asset might go up to $5,155 by 2030.

Central banks bought 53 tonnes of gold in November 2024, the latest addition in a 15-year-old buying pattern. The National Bank of Poland introduced 21 tonnes and People’s Bank of China restarted buying. This institutional demand makes long term stability in the price of the Canadian gold producer. Central banks around the world have bought more than 700 tonnes within the last 12 months, showing confidence in the institutions.

Gold price forecast trajectory showing potential growth to 2030

Critical Minerals Market Expansion Accelerates

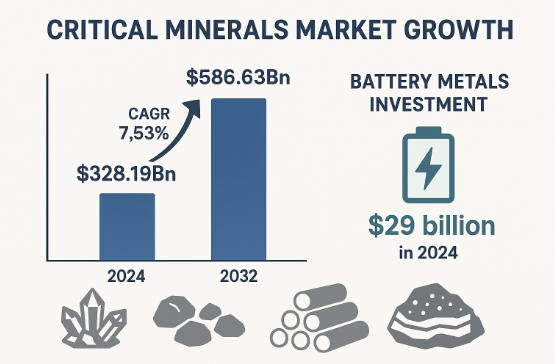

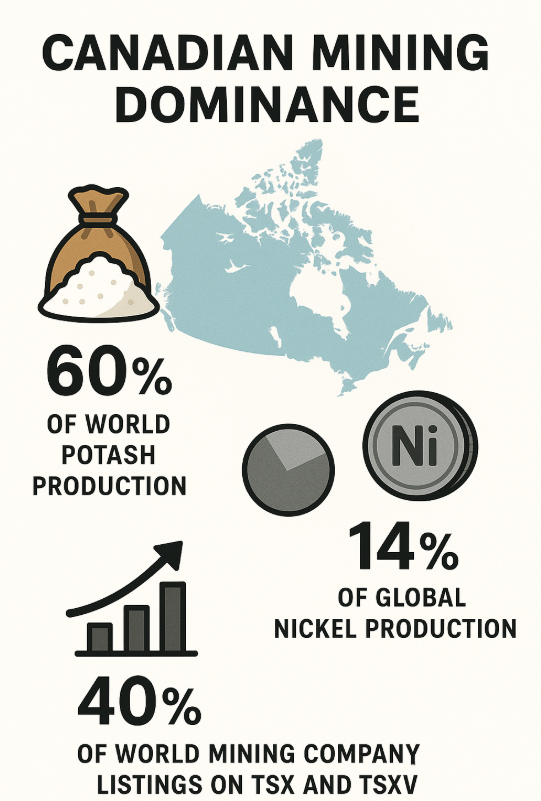

In 2024, the entire industry of critical minerals amounted to $328.19 billion. The industry’s predictions look promising with a growth to $586.63 billion in 2032 with a compound growth rate of 7.53. Canada is the world leader in the production of potash (60%) and to 14% of Nickel. The nation has over 60 minerals worth $55.5 billion in the year 2021 with an increase of 20% compared to the previous year.

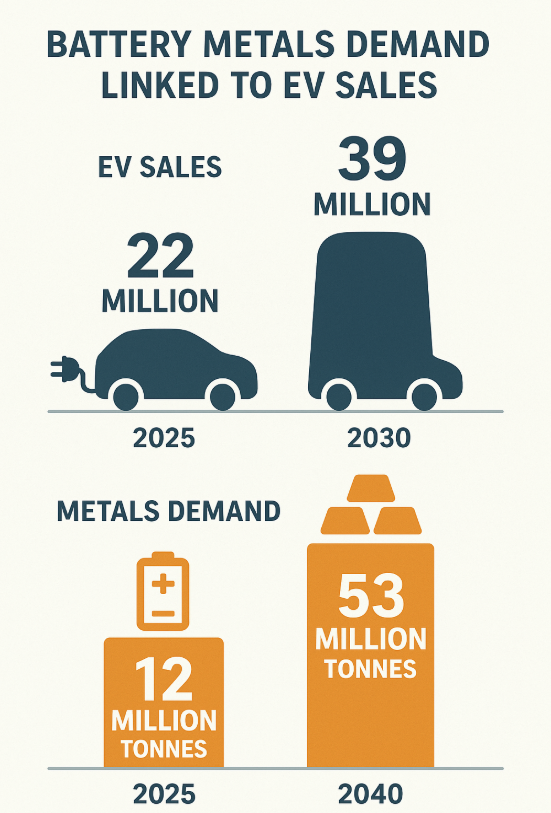

The demand in battery metals is forecasted to grow fourfold by 2040 on the back of electric vehicles. The lithium-ion battery will be meeting an increasing demand of metals, whereby the mass of metals utilised in lithium-ion batteries will increase from 12 million tonnes in 2025 to 53 million tonnes in 2040.

Copper, aluminium and lithium form the largest components by weight in this growth trajectory. Investment in battery metal mines and refineries jumped 80% year-on-year in 2024, reaching $29 billion.

Critical Minerals Market Growth

CSE Mining Companies Lead Innovation Charge

Exchange Performance Metrics Show Strong Growth

The Canadian Securities Exchange hosted 26 junior mining new issues in the first half of 2025. CSE-listed companies averaged 186% share price increases compared to 26% for TSXV listings. This performance differential highlights investor appetite for smaller-cap mining opportunities. The CSE now represents 34.5% of total operating Company listings on Canadian junior public markets. Total operating junior Company listings in Canada reached 2,239, effectively matching 2012 and 2021 levels.

Barranco Gold Mining emerged as the top-performing CSE new issue, rising 1,247% since its February listing. Highland Critical Minerals gained 300% following its May CSE debut, focusing on lithium exploration in Ontario. These companies demonstrate investor confidence in Canadian critical mineral prospects. The CSE’s share of total junior market capitalisation remains at 13.5% despite strong listing growth.

Strategic Positioning in Critical Mineral Supply Chains

StrategX Elements advanced its Nagvaak project in Nunavut, discovering high-grade graphite mineralisation. The Company reported 15% graphitic carbon over 32 metres, including 22% graphitic carbon over 17 metres. The discovery supports potential multi-mineral systems including nickel, copper and silver. The Company completed a $296,960 private placement for working capital requirements.

Highland Critical Minerals holds lithium projects in Ontario’s Quetico District. The Company’s Church Lithium Project sits near Rock Tech Lithium’s 10.6 million tonne Georgia Lake Project. Initial exploration defined five pegmatites containing up to 1.18% lithium oxide. This proximity provides strategic advantages for infrastructure and processing development.

TSXV Gold Producers Navigate Market Volatility

Production Trends Reflect Operational Excellence

TSXV-listed gold companies demonstrated resilience throughout 2025’s market fluctuations. Tudor Gold, Thesis Gold and Spanish Mountain Gold maintained exploration momentum despite commodity price volatility. These companies represent the exchange’s commitment to advancing Canadian gold resources. The TSXV operates 1,459 operating Company listings as of 2024. Mining companies comprise 65% of total TSXV listings and 49% of total market capitalisation.

Max Resource gained 62.5% in weekly trading, reaching a market capitalisation of $12.59 million. The Company’s Sierra Azul copper and silver project spans 188 square kilometres in northeastern Colombia. Freeport-McMoRan agreed to fund $50 million over 10 years for up to 80% project ownership. This partnership validates the Company’s exploration potential and development strategy.

Maple Gold Mines Expands Quebec Operations

Maple Gold Mines increased 50% in weekly trading, achieving a $45.6 million market capitalisation. The Company’s Douay project covers 357 square kilometres in Quebec’s Abitibi greenstone belt. The site hosts indicated resources of 511,000 ounces from 10 million tonnes at 1.59 g/t gold. The resource provides substantial exploration upside within established mining infrastructure.

Strategic investor Michael Gentile led a $5 million private placement for Maple Gold. Agnico Eagle Mines indicated participation to maintain its pro rata ownership interest. This institutional support validates the Company’s exploration strategy and resource potential. The participation demonstrates confidence in Quebec’s mining jurisdiction and regulatory framework.

Junior Mining Market Demonstrates Resilience

TSX Venture 50 rankings identify top-performing companies across multiple sectors. Mining companies achieved 142% average share price performance and 255% average market cap increases in 2025. The methodology considers share price performance, trading value and market capitalisation changes. Mining companies consistently feature among leading performers due to commodity price sensitivity.

Daura Gold emerged as the second-best performing new issue, rising 322% since its January qualifying transaction. The Company acquired the Cochabamba Project in Peru’s Ancash Region, including the 900-hectare Antonella Gold Project. The property sits adjacent to Highlander Silver’s San Luis Gold Project, recently acquired for up to $42.5 million.

Major Gold Producers Set Performance Benchmarks

Barrick Mining Corporation Delivers Strong Results

Barrick Mining finished 4 Q-2025 with 758,000 gold ounces. The Company has a target of 3.15-3.5 million ounces in production of the entire year, excluding the help of production of the Loulo-Gounkoto operations. The second-quarter output rose 5% to 797,000 ounces because of Nevada Gold Mines’ performance. The Company anticipates that 54% of the 2025 output will be realised in the second half of the year with the highest output in Q4.

The operating cash flow of the Company increased by 32% in the first six months to account to the sum of $2.5 billion dollars. Free cash flow increased over two-fold to $770 million. The Company paid shareholders cash dividends and through share buybacks to the tune of $753 million. These are operational excellence and shareholder value creation metrics.

Newmont Corporation Maintains Strategic Focus

Newmont reported 1.54 million gold ounces in the first quarter of 2025. The Company completed strategic divestments of non-core assets following its Newcrest acquisition. Full-year production guidance remains at approximately 5.9 million ounces despite portfolio optimisation. The Nevada Gold Mines joint venture with Barrick delivered 11% sequential production increases.

This partnership represents the world’s largest gold mining complex, employing over 7,000 people. Combined operations include 10 underground and 12 opencast mines across Nevada. The joint venture structure maximises operational synergies while reducing capital requirements for both partners.

Critical Minerals Investment Reaches Record Levels

Battery Metals Command Premium Valuations

Investment in battery metal mines and refineries jumped 80% year-on-year in 2024, reaching $29 billion. This represents the highest annual investment total on record for the sector. Copper emerged as a supply bottleneck, with analysts warning of lagging supply growth relative to EV demand projections. Supply growth may lag demand as new mines become harder to develop under current regulatory frameworks.

Nickel overtook lithium as the most valuable EV battery metal in 2025. Battery nickel deployment reached $2.20 billion compared to $2.15 billion for lithium. This shift reflects changing battery chemistry preferences and relative price movements. Employment in rare earth elements mining projected to grow 21.2% by 2025. Green jobs in mining sectors are projected to grow 18% by 2025.

Battery Metals & EV Demand Growth

Lithium Sector Shows Development Progress

Canada secured two projects among the top 15 lithium producers worldwide at the end of 2024. The Galaxy project, owned by Rio Tinto, ranked eighth globally with 57,621 tonnes LCE forecasted production. North American Lithium, operated jointly by Sayona Mining and Piedmont Lithium, ranked 13th with 31,078 tonnes LCE. Combined Canadian projects represent nearly 7% of global LCE among top 15 sites.

NOA Lithium Brines gained 58.82% year-to-date, focusing on Argentina’s Lithium Triangle. The Company’s Rio Grande project targets 20,000 metric tonnes LCE annually production. Patriot Battery Metals’ Shaakichiuwaanaan project in Quebec outlines potential for competitive high-grade lithium production. The preliminary economic assessment targets up to 800,000 tonnes per annum spodumene concentrate.

Rare Earth Elements Development Accelerates

Canadian Companies Establish Global Presence

Canada Rare Earth expanded operations by acquiring a 70% stake in a Northern Laos refinery. The facility has 3,000 tonnes annual production capacity for rare earth oxides. Commissioning is expected by Q4 2025, providing crucial midstream processing capabilities. This strategic positioning addresses supply chain bottlenecks outside Chinese-controlled operations.

Torngat Metals develops the Strange Lake rare earth project in northern Quebec. The project has potential to become a leading heavy rare earths supplier and foremost dysprosium source. The diversity and quality of mineral deposits offer alternatives to Chinese rare earth production. This positioning supports North American supply chain independence objectives.

Strategic Research Consortium Formation

Appia Rare Earths, Commerce Resources, Defense Metals and Vital Metals formed a strategic research consortium. The collaboration includes March Consulting Associates and mineral processing centre Corem. The initiative accelerates establishment of national rare earth elements industry development. Partnership sharing promotes know-how expertise and state-of-the-art pilot laboratories.

Ucore Rare Metals received $500,000 from Ontario’s Critical Minerals Innovation Fund. The Company plans to advance improvements at its RapidSX commercial demonstration facility. Subsequent private placement raised additional $2.16 million through 3.6 million shares at $0.60 each. These funding mechanisms support technology development and commercial scaling.

Government Support Drives Sector Development

Federal Investment Programs Expand

Canada launched its Critical Minerals Strategy in 2022, targeting 22 of 34 identified critical minerals. The government announced $43.5 million in February 2025 through the Critical Minerals Infrastructure Fund. Investment covers six energy and transportation projects supporting critical minerals development. These programmes address infrastructure gaps limiting sector growth potential.

Germany and Canada deepened critical minerals cooperation through a declaration of intent. The agreement emphasises midstream technologies including processing, refining and recycling. Joint initiatives promote collaboration between enterprises and financial organisations. International partnerships strengthen North American supply chain resilience objectives.

Provincial Support Mechanisms

The G7 Critical Minerals Action Plan outlines coordinated international response to supply chain vulnerabilities. Member countries commit to diversifying supply sources and reducing dependencies. Canada positions itself as a reliable supplier within allied nation frameworks. This approach creates preferential access to Western markets for Canadian producers.

Investment tax credits support battery-electric equipment deployment in mining operations. Large-emitter trading systems incentivise technology adoption across operations. Foran Mining, Glencore Canada and Newcrest Mining implement battery-electric systems. These policies accelerate decarbonisation while maintaining production competitiveness.

Supply Chain Resilience Becomes Strategic Priority

Domestic Production Capacity Requires Expansion

Canada risks losing $12 billion annually in critical minerals production by 2040 without increased mining activity. Investment of $30 billion over 15 years would meet domestic critical minerals potential. Meeting global demand growth requires $65 billion investment during this timeframe. These investment levels exceed current sector capacity, requiring government-industry partnerships.

Canada is the second-largest minerals producer, earning $55.5 billion in 2021. This is the 20% increase compared to the previous year, and this has shown industry resilience. The demand for Canadian mineral products is steadily increasing on the basis of the energy transition needs. Indigenous personnel made up 17,300 work positions in the mining industry, offering economic choices to the locals in remote areas.

Canada’s Global Mining Leadership

Technological Innovation Supports Efficiency Gains

Canadian mining firms use battery-electric equipment in underground work. Technology adoption is favoured by investment tax credits and large-emitter trading systems. The technological improvement, automation, and AI surveillance have led to a change in employment. Metal mining – Mapping and automated systems are expected to increase the employment associated with metal mining by 5.9% by 2025.

Brunswick notices Greenland’s lead in exploring lithium following the success of the 2024 discovery. The Company holds 165,000 hectares across multiple projects, representing the largest mineral licence position. Rapid exploration techniques using portable XRF testing enable efficient target evaluation. The 2025 summer exploration plans include the Paamiut lithium project expansion.

Exchange Dynamics Support Sector Growth

Market Capitalisation Trends Reflect Investor Confidence

The Toronto Stock Exchange reached $5.06 trillion market capitalisation in March 2025. This represents a slight decrease from February’s record high of $5.15 trillion. Mining companies contribute significantly to overall exchange value through resource development activities. TSX and TSXV mining companies raised $6.8 billion in the first six months of 2024. This represents 62% growth compared to $4.2 billion in 2023’s same period.

TSX Venture 50 rankings identify top-performing companies across multiple sectors. The methodology considers share price performance, trading value and market capitalisation changes. Mining companies consistently feature among leading performers due to commodity price sensitivity. The exchanges facilitate 40% of the world’s public mining Company listings.

Mining companies and services being showcased at an exhibition hall, relevant to the Toronto Stock Exchange mining sector

Financing Activities Enable Project Development

Junior mining companies raised $43 billion through 6,600 financings over five years. This represents 47% of global public mining financing activity. The TSX and TSXV exchanges facilitate 40% of the world’s public mining Company listings. Mining represents TMX’s largest sector by capital raising, listed stocks and volume traded.

The 2024 figures mark mining sector rebound from 2022’s low-point of $4 billion raised. Equity capital raised was $6 billion in 2021, showing cyclical recovery patterns. Private placement activities support exploration and development programmes across the sector. StrategX Elements completed a $296,960 placement for working capital requirements.

Employment Generation Drives Regional Development

Workforce Expansion Meets Growing Demand

Mining jobs remain in high demand across Canada in 2025. Demand surge derives from electric vehicle battery production, renewable energy and high-tech industries. The Mining Industry Human Resources Council forecasts Canada’s mining sector needs 80,000 new workers between 2020 and 2030. Many experienced workers approach retirement, creating workforce renewal opportunities.

Employment generation in mining sectors spans direct and indirect opportunities. Direct employment includes excavation, processing, quality control and transportation activities. Indirect employment covers equipment manufacturing, maintenance services and logistics support. Mining offers higher wages compared to agriculture or informal sectors, improving livelihood standards.

Canadian Mining Employment Impact

Regional Economic Impact

Mining continues serving as direct and indirect employer across Canada. Remote locations in northern regions feature fly-in, fly-out arrangements and rotational schedules. Northern territories including Yukon, Northwest Territories and Nunavut focus on diamonds, rare earth elements and gold. British Columbia features challenging terrains with copper and gold operations.

Regions with abundant mineral reserves leverage mining to reduce unemployment significantly. Alternative employment options remain limited in remote and rural areas. Mining stimulates indirect jobs through demand for goods and services supporting sector activities. Economic benefits spread across regions through supply chain multiplier effects.

Inflation Hedge Characteristics Drive Investment Demand

Gold Maintains Safe-Haven Asset Status

Gold demonstrates effectiveness as an inflation hedge during periods of economic uncertainty. Research suggests gold remains crucial for portfolio protection in 2025’s challenging environment. The metal’s low correlation with stock markets provides diversification benefits for investors. Central bank diversification away from US dollar holdings supports long-term demand.

Agnico Eagle Mines represents a preferred Canadian gold stock for inflation protection. The Company’s Toronto headquarters and $82.44 billion market capitalisation provide stability. Recent acquisition of Kirkland Lake enhanced competitive positioning against Barrick Gold. These characteristics attract investors seeking domestic exposure to gold price movements.

Central Bank Diversification Continues

Emerging markets diversify reserves away from US dollar holdings amid de-dollarisation trends. This structural shift supports long-term gold demand from institutional buyers. Central bank purchases provide price floor support during market volatility periods. The Currency Composition of Official Foreign Exchange Reserves shows continued diversification.

US dollar share decreased 0.62% points despite modest fourth-quarter increases. Gold purchases offer alternative reserve assets for central bank portfolios. Institutional demand patterns support sustained price momentum beyond traditional safe-haven cycles. This trend creates fundamental support for Canadian gold producers’ revenue streams.

Future Outlook Reflects Structural Demand Growth

Production Guidance Supports Sector Optimism

Barrick expects 54% of 2025 production to occur in the second half. The Company anticipates strongest output in the fourth quarter, targeting 940,000 ounces. Pueblo Viejo expansion and Nevada Gold Mines improvements support production growth. These operational enhancements demonstrate sector confidence in sustained demand fundamentals.

Global passenger EV sales approach 22 million units in 2025, representing 25% growth from 2024. Annual sales should surpass 39 million vehicles by 2030. China maintains dominance with two-thirds of global EV sales, driving battery metals demand. This structural growth trajectory supports long-term investment in critical mineral projects.

Investment Requirements Drive Sector Consolidation

The sector faces persistent risks around permitting, geopolitical tensions and commodity price fluctuations. Copper supply growth may lag demand as new mines become harder to develop. Lithium and aluminium markets expect tightening if EV adoption exceeds forecasts. These supply constraints support premium valuations for established producers with operational assets.

Canadian mining companies that invest in climate solutions position themselves for long-term success. Low-carbon mineral producers gain competitive advantages through sustainable finance products. Newmont and Anglo American issued sustainability-linked bonds worth $1 billion and €745 million respectively. Environmental, social and governance criteria increasingly influence investment decisions across the mining sector.

Conclusion

CSE and TSXV gold and critical mineral miners successfully balance dual market demands in 2025. Safe-haven gold investment combines with supply chain critical mineral requirements to create diversified opportunities. Canadian exchanges facilitate access to global resources essential for energy transition and economic security. Strategic positioning enables these companies to benefit from structural demand growth across multiple commodity sectors.

Investment continues flowing into Canadian mining operations that demonstrate operational excellence and environmental responsibility. The sector’s performance reflects Canada’s strategic importance in global resource supply chains and economic stability. Government support programmes accelerate development while maintaining environmental standards and Indigenous community engagement.

Employment generation provides economic opportunities across urban, rural and remote regions throughout Canada. Technological innovation drives efficiency gains while creating specialised job opportunities in data analytics and environmental management. The mining sector’s contribution of $159 billion to GDP and 711,000 jobs demonstrates its fundamental importance to Canadian economic prosperity.

Future growth depends on continued investment in exploration, development and processing capabilities. International partnerships strengthen supply chain resilience while reducing dependencies on single-source suppliers. Canadian miners positioned at the intersection of safe-haven demand and critical mineral requirements maintain competitive advantages in evolving global markets.

FAQ: Canadian Gold & Critical Minerals on CSE and TSXV

Market Fundamentals & Exchange Structure

What’s the difference between TSX, TSXV, and CSE exchanges?

TSX: Senior companies with market caps exceeding $75 million. Major producers like Barrick and Newmont trade here.

TSXV: Junior miners and smaller companies. 1,459 listings with 65% being mining companies. Companies graduate to TSX upon meeting requirements.

CSE: Most flexible listing requirements for emerging companies. Represents 34.5% of Canadian junior listings. CSE companies averaged 186% gains vs 26% for TSXV in 2025.

How significant is Canada’s role in global mining?

Canada dominates with 60% of world potash, 14% of global nickel, and 40% of world’s public mining companies. The sector employs 711,000 people and contributes $159 billion to GDP.

Investment Strategies & Market Access

How do I invest in Canadian gold and critical mineral stocks?

Open account with Canadian broker offering TSX/TSXV access. Start with established producers, then explore juniors. Consider 5-15% portfolio allocation and dollar-cost averaging for volatility.

What factors drive mining stock valuations?

Commodity prices, all-in sustaining costs (AISC), reserve quality, management track record, and ESG compliance. Market conditions and geopolitical stability also matter.

Gold Investment Fundamentals

Why is gold considered a safe-haven asset in 2025?

Gold provides inflation protection, currency devaluation hedge, and low correlation with stocks. Central banks bought 700+ tonnes recently. Prices hit record $3,400+ with forecasts reaching $5,155 by 2030.

Should I buy physical gold or gold mining stocks?

Physical gold: Direct exposure, no counterparty risk, requires storage.

Mining stocks: Operating leverage, dividend potential, professional management. Choice depends on risk tolerance and objectives.

Which Canadian gold companies offer the best opportunities?

Producers: Barrick (797k oz Q2), Newmont (1.54M oz Q1), Agnico Eagle ($82B market cap).

Juniors: Tudor Gold, Spanish Mountain Gold, Maple Gold (511k oz resource).

Critical Minerals & Supply Chain Dynamics

What are critical minerals and why are they strategically important?

50 elements essential for clean energy and technology. China dominates processing (90% rare earths, 70% graphite). Market growing from $328B (2024) to $587B (2032).

How does the green energy transition affect mining investments?

EV sales rising from 22M (2025) to 39M (2030). Battery metals demand quadrupling by 2040. Nickel overtook lithium as most valuable battery metal. Investment hit $29B in 2024.

What government support exists for critical minerals development?

$43.5M Critical Minerals Infrastructure Fund, investment tax credits, G7 Action Plan, and international partnerships with Germany and UK.

Market Performance & Investment Timing

How have Canadian mining exchanges performed in 2025?

CSE companies gained 186% vs TSXV’s 26%. Miners raised $6.8B in H1 2024 (62% growth). Top performers: Barranco Gold (+1,247%), Highland Critical Minerals (+300%).

When is the optimal time to invest in mining stocks?

During commodity downturns for value opportunities. Use dollar-cost averaging for volatility. Consider structural trends: safe-haven demand and critical minerals supply diversification.

Risk Management & Due Diligence

What are the primary risks of investing in junior mining companies?

High volatility, limited operating history, exploration uncertainty, significant dilution risk, and dependence on commodity prices. Liquidity constraints during market stress.

How should investors evaluate junior mining companies?

Assess management track record, geological reports, cash position, infrastructure access, and permitting status. Consider proximity to processing facilities and community relations.

Regulatory Framework & Compliance

What regulatory requirements govern Canadian mining operations?

Provincial mining acts, federal environmental assessments, Indigenous consultation requirements, and securities regulations. Flow-through share tax benefits available.

What challenges face new mine development in Canada?

5-15 year permitting timelines, Indigenous consultation, environmental assessments, remote infrastructure needs, and capital requirements of $100M-$10B+.