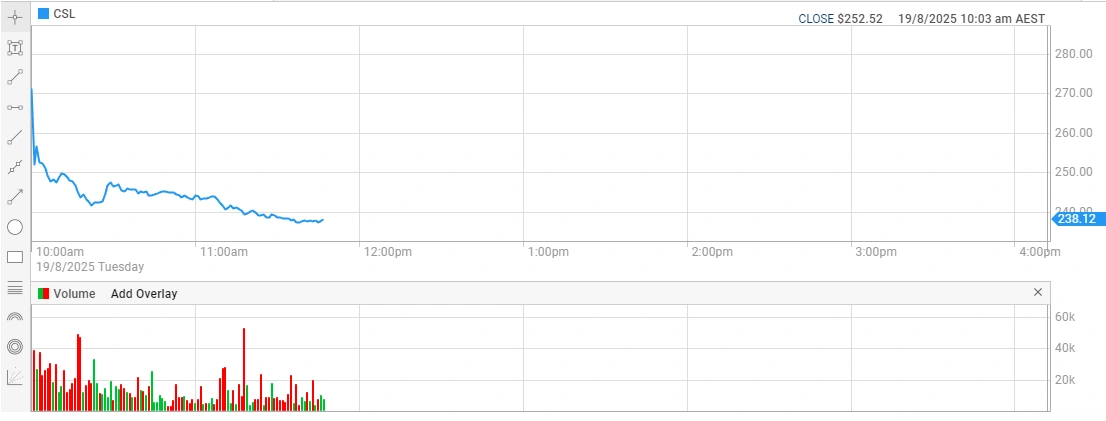

CSL Limited (ASX: CSL) shares experienced significant volatility on Monday following the biotechnology giant’s announcement of sweeping strategic changes, including plans to slash 3,000 jobs and spin off its influenza vaccine division CSL Seqirus as a separate ASX-listed entity.

CSL shares initially slumped 8% in early trading as investors digested news of the comprehensive restructuring program. However, the stock recovered some ground as analysts highlighted the long-term benefits of the transformation strategy.

Major Restructure to Drive $550 Million in Annual Savings

The pharmaceutical giant revealed plans to reduce its global workforce by nearly 15%, affecting approximately 3,000 positions across its 30,000-strong employee base. The restructuring forms part of a broader transformation initiative designed to simplify the business and enhance operational efficiency.

CEO Paul McKenzie stated the restructuring would deliver annualised cost savings of $500-550 million progressively over the next three years. “Our business has grown this year despite an unprecedented level of challenge and volatility in our external operating environment,” McKenzie said.

The company expects one-off restructuring costs of approximately $700-770 million (pre-tax) to be recognised in Financial Year 2026, with cash flow impacts of $400-450 million in FY26 and a further $100 million in FY27.

CSL Seqirus Demerger Creates New Vaccine Powerhouse

Perhaps the most significant announcement was CSL’s intention to demerge its influenza vaccine division, CSL Seqirus, as a separate ASX-listed entity before the end of Financial Year 2026. The newly independent company will be chaired by Gordon Naylor, an experienced company director and former President of CSL Seqirus.

CSL Seqirus is described as a global leader in seasonal influenza vaccines, with a highly differentiated product portfolio centred on innovations in cell and adjuvant technologies. The demerger aims to reduce complexity while making both businesses more agile and efficient.

“This demerger of CSL Seqirus to our shareholders will create an ASX-listed, global influenza vaccine leader. The company has a great future that will be driven by its strong competitive position in an improving market,” McKenzie explained.

The remaining CSL group will continue to maintain leading market positions in multiple rare and serious diseases through its CSL Behring and CSL Vifor divisions.

Strong FY25 Results Underpin Strategic Transformation

The restructure announcement came alongside CSL’s FY25 financial results, which showed robust performance despite challenging market conditions. The company reported a 17% increase in full-year statutory profit to $4.6 billion, beating market consensus estimates of $2.94 billion.

Revenue grew 5% to $15.6 billion, while underlying profit (NPATA) increased 14% to $3.3 billion on a constant currency basis. The company declared dividends of $1.62 per share, representing a 12% increase from FY24’s payout and exceeding analyst expectations of $1.56 per share.

Today we shared our full-year results for FY25. Take a look at some of the key financial and operational highlights. For more details visit our Investor Centre: https://t.co/h6ywrrsTgq #CSL #FullYearResults pic.twitter.com/PGsoHyjafo

— CSL (@CSL) August 18, 2025

CSL’s three main divisions all contributed to the solid result:

- CSL Behring continued strong demand for life-saving plasma therapies

- CSL Seqirus demonstrated resilience despite challenging vaccine market conditions

- CSL Vifor delivered strong growth driven by iron business and nephrology portfolio momentum

$750 Million Share Buyback Program Announced

As part of its capital management strategy, CSL announced plans to recommence a multi-year, on-market share buyback program starting with $750 million in Financial Year 2026. The buyback is expected to progressively increase over the medium term, providing additional returns to shareholders alongside the regular dividend payments.

The buyback program signals management’s confidence in the company’s cash generation capabilities and commitment to enhancing shareholder value through the transformation period.

Also Read: Pacgold Secures Farm-In Agreement for St George Gold-Antimony Project

Analyst Outlook Remains Positive Despite Near-Term Volatility

Despite the initial share price decline, analyst sentiment towards CSL remains constructive. The overall consensus recommendation stands at “Buy,” with price targets averaging $310.22 according to recent broker research.

Analysts highlight several positive factors supporting the medium-term outlook:

- Completion of manufacturing platform rollouts (RIKA and iNomi) expected to improve margins

- Strong pipeline of new products including ANDEMBRY® and HEMGENIX®

- Demographic trends supporting long-term demand for CSL’s therapies

- Strategic focus on core competencies following the Seqirus demerger

For FY26, CSL expects group revenue growth of approximately 4-5% at constant currency, with continued robust demand for CSL Behring products and stabilisation in CSL Seqirus seasonal influenza revenue.