Rare Earths Move to the Centre of Global Strategy

Rare earth elements now stand at the centre of global energy and defence strategy as governments classify them as indispensable resources for modern economies. The International Energy Agency forecasts that demand for rare earths will increase fourfold by 2040 under pathways aimed at meeting net zero targets.

Geopolitical competition has magnified their importance. Clean energy sectors, advanced defence industries, and high-technology manufacturers now drive demand growth beyond expectations.

China continues to dominate supply. Western economies respond with urgent diversification strategies.

The Australian Government identifies rare earths as essential to protecting both the economy and national security.

Global Map of Rare Earths Projects

Defining Rare Earth Elements

Rare earths include 17 metallic elements on the periodic table. They are lanthanides plus yttrium and scandium. These metals are present in Earth’s crust but rarely appear in concentrated form. Separation and refining remain technically complex. Despite the name, rare earths occur abundantly. The challenge lies in economic extraction and processing.

Driving Clean Energy Applications

The structural demand in the rare earth sector is fuelled by clean energy development in a variety of technologies. It takes up to 600 kilograms of permanent magnets made out of neodymium, praseodymium and dysprosium to make one offshore wind turbine. WindEurope expects the number of global offshore turbines to be tripled by 2030, which results in regular pressure on the rare earth supply.

Assuming the balance ratio is one to two kilograms is how the International Energy Agency estimates the amount of rare earths found in the electric vehicles’ traction motors. Uptake of EVs in the globe might exceed 230 million units by 2030, which is a major pressure on the supply of resources. Efficiency is enhanced in solar panels by the use of coatings that contain terbium and europium and in green hydrogen, lanthanum and cerium are the most important catalysts. According to the Department of Industry in Australia, rare earths domestic demand is expected to increase by seven per cent yearly until 2035 due to the speeding up of renewable deployment.

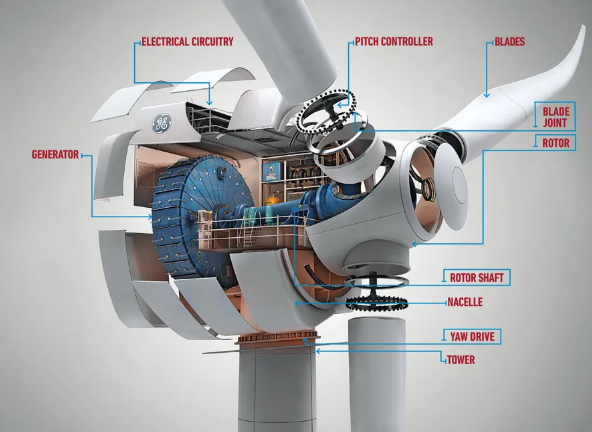

How a wind turbine generator works

Rare Earths in Defence Systems

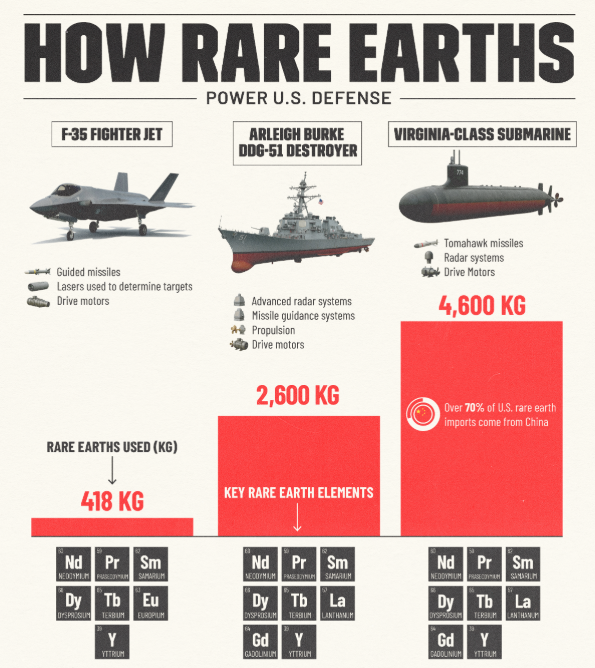

Defence establishments also depend on rare earths for core technologies that shape modern combat capabilities. The US Defence Department stresses that stealth technologies, radar, sensors, and missile guidance all require rare earth materials. A single-class Virginia nuclear submarine is approximated to have 4.2 tonnes of rare earth inputs and an F-35 fighter jet up to 417 kilograms of rare earth enabled components. Neodymium and praseodymium magnets also improve precision-guided munitions, and yttrium garnets improve radar magnetics.

With rare-earth-enabled sensors on board, the Royal Australian Air Force also has surveillance aircraft that guarantee operational robustness. Defence spending worldwide increased by more than US$2.4 trillion in 2024, as reported by the Stockholm International Peace Research Institute, which further justified the role of rare earth elements as essential facilitators of powerful defence systems.

Uses of Rare Earths in U.S. Defence

Australia’s Resource Strength

Australia possesses worldwide potent rare earth oxide reserves that are estimated to comprise almost 4.2 million tonnes, as per Geoscience Australia. Most of the known deposits are found in Western Australia and the Northern Territory, with Mount Weld in Western Australia being deemed as one of the richest deposits throughout the world. The Mount Weld project has 55 million tonnes of ore with average grades of about eight per cent rare earth oxide and as such, it is globally competitive in quality.

Lynas Rare Earths still remains the most significant producer outside of China and has long-term export strategies with Japanese, American and European buyers. The Nolans project in the Northern Territory should be able to yield 4400 tonnes per annum of neodymium-praseodymium oxide starting year 2026 and onwards. Being a non-Chinese supplier that produces on such a scale, Australia presents stability in the decades to come when demand doubles exponentially.

Aerial view of Mt Weld Project, Western Australia

St George Mining’s Emerging Role

Smaller Australian miners also pursue opportunities in critical minerals, with St George Mining advancing exploration at its Mt Alexander project in Western Australia. The Company, known for nickel and lithium, now investigates rare earth potential across its holdings. Management emphasises alignment with the clean energy transition, highlighting early signs of rare earth mineralisation alongside lithium exploration. Investors view such initiatives as part of Australia’s widening supply base beyond established producers.

St George Mining recently expanded internationally with its 100%-owned Araxá Project in Brazil, which holds a substantial JORC-compliant resource of over 40 million tonnes at 4.13% total rare earth oxides. The Araxá deposit is high in valuable magnet rare earths and sits near the surface, supporting future low-cost mining. Ongoing drilling continues to reveal further resource upside, firmly positioning St George as an emerging player in both Australian and global rare earths development.

Ongoing drilling operations at the Araxá Project in Brazil

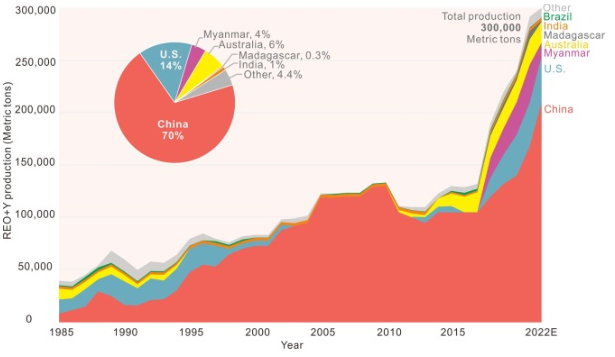

China’s Continuing Dominance

China is still the main force in the production and processing of Rare Earths, beating the other forces in production, notwithstanding the efforts of global diversifiers. In 2023, Chinese output would hit 240,000 tonnes or close to 70 per cent of the overall mining supply. The refining and separation capability is even more concentrated, with more than 85 per cent of processing in the world taking place in China. The Chinese policies on exports are not predictable, contributing to price fluctuations in the world and strategic unease among importers.

The Chinese export ban on its neighbour, Japan, in 2010 caused price spikes of 300 percent in a matter of a few months when they were in a maritime wrangle. Beijing imposed the ban on gallium and germanium in July 2023, which further strengthened the views of resource leverage in geopolitical environments. Western strategists point out the fact that China has an exorbitant amount of concentration of capacity, which constitutes an economic and a security vulnerability.

| Category | Rare Earth Elements | Applications | Key Details |

|---|---|---|---|

| Clean Energy | Neodymium, Praseodymium, Dysprosium | Wind turbine magnets, EV motors | Offshore turbines need up to 600 kg magnets each; EVs use 1-2 kg REEs each |

| Lanthanum, Cerium | Green hydrogen catalysts | Essential for clean hydrogen systems | |

| Terbium, Europium | Solar panel coatings | Improve efficiency of photovoltaic cells | |

| Defence | Samarium, Cobalt | Stealth fighter jet and submarine magnets | Enhance thermal tolerance and stealth capabilities |

| Neodymium, Praseodymium | Precision-guided munitions | Critical for weapon targeting and control | |

| Yttrium | Radar signal processing | Improves sensor performance | |

| Australian Players | — | Lynas Rare Earths, Arafura Rare Earths, St George Mining | Mining, refining, and exploration initiatives |

| Global Supply Leaders | — | China (~70% production), Vietnam, Tanzania, Canada | China holds refining dominance; others ramp up mining projects |

Table 1: Applications of Rare Earths

Diversification Strategies Worldwide

Nations worldwide pursue supply diversification to reduce dependence on Chinese supply chains. Japan imports approximately 10,000 tonnes annually of rare earth oxides from Australian mines, with Lynas committed to long-term supply agreements. The United States provided US$120 million to support Lynas’ Texas refinery, designed to process up to 5000 tonnes annually of rare earth oxides.

India also expanded bilateral cooperation with Australia under the Quad framework in 2022, targeting joint projects and co-financing opportunities. The European Union negotiated agreements with Greenland and Tanzanian developers, aligning policy frameworks to reduce import risks. These efforts reflect a growing commitment to diversifying supply at a pace consistent with expanding renewable and defence needs.

Environmental Implications

Environmental impacts remain a defining issue for rare earth mining and processing operations worldwide. REE refining produces significant radioactive waste that often contains thorium and minor uranium traces. China’s Inner Mongolian basin illustrates these consequences, with waste ponds near Baotou creating widespread soil and groundwater contamination. Villagers in nearby districts report crop impacts due to waste seepage and tailings exposure.

As a response, the Australian Government enforces strict tailings management rules and requires companies to submit rehabilitation plans prior to approval. Environmental organisations demand further guarantees of ecological safety from Australian projects. CSIRO experiments with greener refining processes show early potential for reducing chemical use and cutting risks of long-term damage.

Australia is moving towards sustainable mining

Advancing Processing Technology

Australia is at the forefront of innovation in cleaner technologies of refining, which seeks to overcome the obstacles in processing markets. CSIRO scientists collaborate with the ion-exchange membranes and a plasma separation system to limit dangerous chemical dependence. Others like Arafura Rare Earths are investing in integrated mine to oxide facilities, and are planning combined production of up to 14,000 tonnes a year. Northern Minerals intensifies beneficiation methods at Browns Range so that the heavy rare earths such as dysprosium and terbium, can be recovered. The partners have been putting in the effort in these projects, and Japanese and Korean partners see common ground in cleaner processing architectures. Analysts estimate that such technology has the potential to save the production cost to less than half in the future and save present waste management requirements.

Volatile Global Market

Price instability frequently disrupts rare earth market planning. In 2011, neodymium oxide surged from US$40 per kilogram to over US$400 within an eight-month period following disputes with China. Prices later fell almost 60 per cent but stabilised at levels well above earlier costs.

In 2020, the average price of Praseodymium was US$60 per kilogram and went beyond USD 100 towards the end of 2023, as the industry benchmarkers observed. Benchmark Mineral Intelligence expects the prices of the rare earths to grow at an estimated annual rate of close to 10 per cent up to 2035, mainly as a result of the demand in renewable magnets. Fluctuation in price causes pressure to financiers and difficulty during the development, but the long run expectations are healthy in terms of an increase in the demand growth curves.

Global REE production by country

Recycling and Circular Economy Prospects

Australia now examines recycling as a structural element of mineral security. CSIRO calculates that by 2040, recycled rare earth sources could meet 25 per cent of demand. Countries like Japan already demonstrate strong recovery rates that surpass 50 per cent for neodymium magnets extracted from discarded devices.

Australia targets production of over 300 tonnes annually from recycling by 2030 if investment growth sustains momentum. Policymakers incorporate circular economy principles into the Critical Minerals Strategy as they aim to offset both imports and environmental strain. The move further signals the potential of urban mining to play an expanding part in supply security.

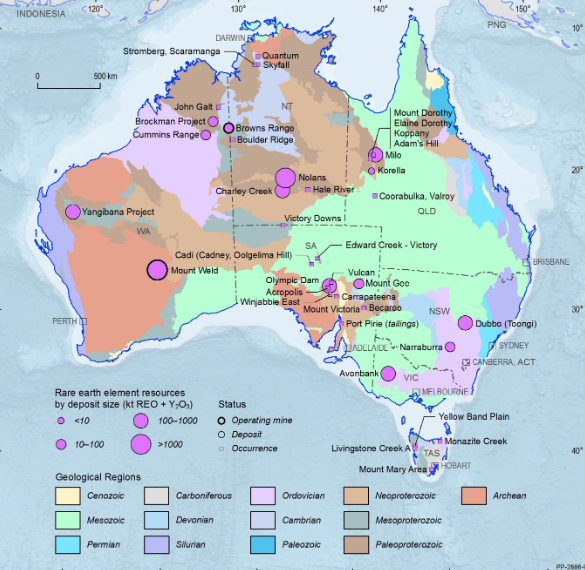

Australia’s Rare Earths Deposit as of 31 December 2018

Investment and Financing

Australian rare earth investment continues expanding. Bloomberg recorded fundraising by Australian exploration companies exceeding A$1.2 billion during 2023 alone. The Northern Australia Infrastructure Facility allocated more than A$500 million in concessional loans for strategic REE projects.

Foreign government-backed organisations such as Japan Oil, Gas and Metals and the US Export-Import Bank continue to fund projects including Nolans and Mount Weld. Private equity and listed companies demonstrate steady institutional interest in supporting large-scale resource initiatives. Analysts stress that financing remains challenging for early-stage ventures due to market uncertainty, but long-term global demand fuels investor commitment.

Indigenous Considerations

Mining projects proceed in areas tied to Indigenous heritage. The Nolans’ rare earth development involves agreements negotiated with the Anmatjere community in the Northern Territory. These agreements include employment plans, cultural respect mechanisms, and protections for heritage sites. The Minerals Council of Australia publishes frameworks encouraging transparent engagement with traditional owners.

Strong Indigenous participation is increasingly regarded as essential for legitimising projects and minimising legal or social opposition. Policymakers view Indigenous partnerships as necessary for building resilient and durable resource agreements into the coming decades.

Nolans Bore Rare Earth Project

Emerging Competitors

Global competitors broaden supply networks across multiple continents. Vietnam boosts output to around 30,000 tonnes annually while Myanmar contributes nearly 20,000 tonnes, mainly from heavy rare earth deposits. The Ngualla project in Tanzania reports reserves of 214 million tonnes grading at 2.4 per cent rare earth oxide.

Canada pursues projects in Quebec and Newfoundland with Ottawa allocating C$1.5 billion to critical mineral development initiatives. These producers contribute new supply yet face infrastructure, political, and financing challenges. Australia emphasises its advantage through regulatory stability, infrastructure networks, and strategic alignment with major international buyers.

Also Read: St George Mining Uncovers High-Grade Rare Earths 1km East of Existing Araxá Resource in Brazil

Security Dimensions

Strategic analysts reinforce that rare earths represent more than economic drivers by serving as direct enablers of security outcomes. The Pentagon identifies rare earths as highly prioritised under strategic materials policy. Canberra also emphasises that future defence readiness relies on secure mineral access. Quad declarations during summits highlight diversification of supply chains as part of Indo-Pacific regional stability frameworks.

NATO and the European Union also categorise rare earths as priority strategic resources with implications for security resilience. Australia’s position as a trusted producer builds its diplomatic influence across the Indo-Pacific.

Long-Term Prospects

The International Energy Agency forecasts global rare earth demand exceeding 1.5 million tonnes annually by 2040. CSIRO calculates that recycling and substitute technology could serve nearly 20 per cent of market demand by then.

Australia expects to meet at least 10 per cent of global supply by 2030 through expansion of projects across both WA and NT.

Forecasts highlight that new projects, advanced technology, and recycling will shape the balance of supply. Sustained global demand confirms that rare earths will continue defining the industrial landscape across energy, technology, and defence platforms.

Outlook for Rare Earths

Rare earth elements underpin the transition to renewables and the advancement of next-generation defence systems. Nations worldwide now pursue stable and responsible supply strategies. Australia emerges as a central stable supplier outside China with strong reserves, projects, innovations, and governance frameworks that strengthen its strategic importance. With demand levels rising across electric vehicles, renewable energy grids, military technology, and advanced electronics, rare earths now mark a decisive frontier between industrial transformation and national security.