Introduction

Copper deficits are the most direct threat currently to the worldwide energy transition. The red metal, in high demand for its higher conductivity and anticorrosion properties, is an integral part of virtually all clean energy technology—electric vehicle (EV) motors, offshore windfarms, and new battery plans, just to name a few. As economies attempt to decarbonise and develop their energy infrastructure, copper demand is surging to record levels.

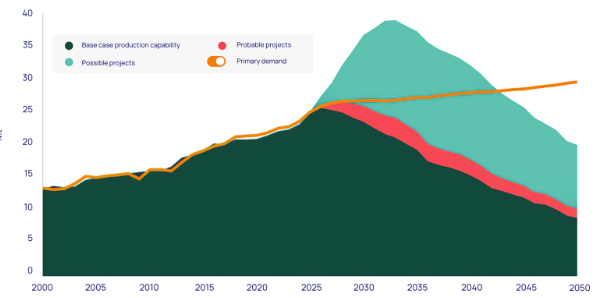

Projected copper supply-demand gap through 2035

Industry forecasts suggest that by 2035, the gap between demand and supply can increase up to 50 million tonnes annually. That is twice the amount of copper consumed globally from 1900 through to 2022, and that is a structural deficit which can result in delays in production, disruption in the supply chain, and volatile, high prices. It will require concerted effort through diversification of sources, expansion of recycling, technological breakthroughs, and global cooperation to fill this gap.

Growing Demand Drives the Supply-Demand Gap

Key sectors driving copper demand growth

The accelerating shift to electrification is the primary cause of the widening copper gap. S&P Global Market Intelligence puts the annual deficit in 2035 at tens of millions of tonnes, with demand outpacing supply. Several related trends are behind the imbalance.

- Renewable Energy Expansion: Wind farms, solar parks, and hydroelectric power plants require huge amounts of copper for cabling, inverters, and grid connections. A single offshore wind turbine utilizes up to eight tonnes of copper.

- Transport Electrification: Electric vehicles use anywhere from double to four times as much copper as internal combustion engine vehicles due to batteries, motors, and charging systems.

- Urbanisation and Infrastructure: Urbanisation of emerging economies is driving urbanisation at a fast pace, which in turn is driving the construction of new transportation networks, smart grids, and housing, all of which require copper cabling and wiring.

- Technological Advances: 5G telecommunication networks, data centers, and IoT devices are building new levels of copper demand.

This steady rise in demand, if not checked, may outpace existing capacity, compromising progress towards renewable energy targets.

Copper’s Role as the Backbone of Renewable Energy

Characteristics of copper make it unmatchable in applications in clean energy systems. Its superior electrical conductivity implies low power loss during transmission, and its strength ensures long life in severe conditions.

Major applications where copper plays an essential role are:

Copper components inside renewable energy systems

- Solar Power: Copper has applications in grounding and wiring, and inverters of the photovoltaic systems. Large-scale solar panels could contain tonnes of the metal in their makeup.

- Wind Energy: Generator coils and grounding systems on onshore and offshore wind turbines (as well as the power-carrying cables) are all based on copper.

- Energy Storage: Battery storage systems required to stabilize the variable generation of renewables rely on copper busbars and connectors.

- Power lines: The grid components, such as transformers and high-voltage transmission wires, are made of copper.

McKinsey & Company puts demand for copper in electrification at 25 million tonnes today to rise to 36.6 million tonnes by 2031. Supply projections, however, will lag at 30.1 million tonnes, creating a shortfall of 6.5 million tonnes. Goldman Sachs analysts further estimate that green applications will grow from 4% of total copper consumption in 2020 to 17% by 2030.

Geopolitical and Production Pressures

Global copper production map highlighting top suppliers

The copper value chain is heavily concentrated in a small number of production countries and, as such, is vulnerable to both production bottlenecks as well as geopolitical risk.

There is a virtual monopolization of world production in South America, and particularly Chile and Peru. Chile contributes approximately 27% of production, though its mining sector has been disturbed by dropping grades of ore, increasing water shortages, and political tensions. Uncertainty in labour and new royalty taxes have also disturbed production.

The second-largest world producer, Peru, has seen consecutive supply disruptions through social unrest and protests against mining.

Although Africa, and in particular the Democratic Republic of Congo (DRC), is entering the equation, it remains too small in tonnage to offset South American losses. The DRC boosted copper exports from 1 million tonnes in 2021 to 2.3 million tonnes in 2022, but it remains to have its infrastructure and governance problems sorted out.

In other areas, long permitting times, investment in exploration deficiencies, and local resistance have been slowing down project development.

Structural Factors Restraining Copper Supply

Several structural issues are responsible for sluggish demand for copper supply:

- Bleeding Ore Grades: Extraction of copper from mines with diminishing metal grades, increasing costs, and lowering production efficiency.

- Long Project Cycles: Commercial output normally takes about 17 years from discovery, limiting the ability of the industry to make quick adjustments to market demand.

- Environmental Restraints: Water usage, land rehabilitation, and carbon emissions due to mining are increasingly being held to account by governments and people.

- Investment Shortfalls in Capital: Some mining firms are afraid to invest massive amounts of capital in long-term projects due to volatile prices and speculative demand projections.

These constraints exert a continuous grip on supply even in the boom years of demand.

Strategic Responses to Shortages in Copper

Remediation to copper shortages entails a multi-faceted approach of short-run relief measures and long-run capacity building.

Solutions to address copper shortages

Diversification of Resources

Emerging new mining prospects in Canada, the United States, Zambia, and Mongolia have the prospect of reducing dependence on politically unstable suppliers. Sophisticated geological surveys and satellite data are finding previously untapped deposits.

Investment in technology enabling the economic processing of low-grade ores has the prospect of unlocking significant extra reserves.

Growth in Recycling

Current recycled copper meets approximately 32% of global needs. Increased recycling of e-waste, upgrading scrap collection networks, and refining capacity expansion can reduce demand for primary mining. Recycling of metals from e-waste and infrastructure waste, or urban mining, is full of unexploited potential.

Technological Breakthroughs

Technologies such as bioleaching, solvent extraction, and artificial intelligence-based mineral sorting can improve yield levels and assist in reducing environmental impacts. Substitution of copper with aluminium, wherever technologically possible, can reduce demand in non-critical applications like air conditioning coils and some transmission lines.

Public-Private Partnerships

Cooperation between government and industry will be needed to accelerate project schedules, establish regulatory certainty, and fund large-scale exploration and processing plans. Governments can entice investment through tax breaks, fast-track licenses, and infrastructure development.

Investment Opportunity in a Tight Market

The expected copper shortages are opportunities for clever investors. Higher prices, if the deficit occurs, can be advantageous to miners, recyclers, and technology companies.

Investors can focus on:

- Exploration and Expansion Programs: Companies that form new deposits or develop higher recovery grades at current mines.

- Recycling Technology Companies: Companies that find scalable, low-cost technology for copper recovery.

- Geopolitically Stable Regimes: Investments in stable nations with good mining laws and infrastructure.

- Nonetheless, high lead times in mine development guarantee that early capital investment is required to grab future market fashion.

The Role of Global Cooperation

There must be coordination between production nations, consuming economies, and international bodies to ensure a safe copper supply chain. International agreements can ensure good mining practices, improve trade transparency, and standardize environmental standards.

Immediate action is:

- Promoting traceability for copper from mine to market.

- Sharing research on sustainable mining methods and recycling technology.

- Creating instruments to finance development infrastructure in future mining regions.

- These measures can balance global copper demand and supply and reduce the environmental costs of Copper mining.

Also Read: https://colitco.com/esg-mining-growth-sustainability/

Conclusion

The impending ubiquitous Copper shortages in the coming decade threaten the cost and speed of the energy transition around the world. The action of many would slow the implementation of renewable energy, increase the cost of infrastructure development, and risk achieving climate goals.

Assuring the supply of Copper in the future will need advancement in all three areas, that is, exploration, recycling, and process technology, as well as secure regulatory systems and collaborations. Nevertheless, the governments, business leaders, and investors need to think long-term instead of short-term solutions.

Reliability of the next generation of energy technologies–from electric vehicles to clean generation and smart grids–will rest on today’s commitment to ensuring one of the world’s most important industrial metals.

Sustainable future powered by renewable energy and copper infrastructure