Introduction: A Changing Landscape for Global Mining

The mining sector occupies the hub of the world economy. From lithium for electric cars to copper for sustainable energy grids, minerals continue to be the foundation of a low-carbon world. But the industry is subject to unprecedented pressure. Investors, regulators, and host communities increasingly expect accountability over more than just financial returns.

This change is captured in Environmental, Social, and Governance (ESG) standards. What was once an ancillary add-on, ESG has become the driver of how firms raise capital, mitigate risks, and safeguard reputations. On exchanges such as the ASX in Australia and the TSXV in Canada, miners are increasingly under pressure.

The issue is straightforward: how can resource firms provide growth while keeping their credibility on sustainability commitments?

ESG now drives capital, risk control, and reputation in mining.

Why ESG Matters More Than Ever

Mining operators used to judge success in terms of production, exploration yields, and profits. Investors now want more, however. ESG metrics evaluate how an enterprise is affecting the world, employees, and governance structures.

For mining, the relevance of ESG is self-evident. Land disturbance, power consumption, water usage, and community interaction are part of the business. Anything that goes awry here can erode trust and even cause projects to be shut down.

Institutional investors like BlackRock and Norway’s sovereign wealth fund increasingly factor ESG ratings into portfolio decisions. Regulators are tightening disclosure rules, particularly around carbon emissions. Consumers, too, demand that electric vehicles, solar panels, and batteries use responsibly sourced materials.

This generates pressure and opportunity. Miners who incorporate ESG can draw in lower-cost capital, mitigate legal risks, and guarantee sustained growth. Those that do not run the risk of being excluded from funding and reputational failure.

How ESG Standards Apply Across Key Exchanges

The ASX: Australia’s Resource Backbone

The Australian Securities Exchange (ASX) hosts several hundred mining companies, ranging from exploration juniors to large producers such as BHP and Rio Tinto. ESG reporting has emerged as an issue of prime importance for them.

The ASX Corporate Governance Principles also mandate listed entities to report significant environmental and social risks. Shareholder activism has also gained momentum, especially in climate change. Major superannuation funds urge miners to adopt net-zero goals, while Indigenous land rights are still a priority topic.

High-profile scandals, including Rio Tinto’s destruction of Juukan Gorge, have highlighted the price of bad ESG management. Consequently, ASX-listed miners are under relentless pressure to show community involvement, emissions cuts, and careful water use.

ASX miners face pressure on community ties, emissions cuts, and water use.

The TSXV: Canada’s Exploration Hub

The TSX Venture Exchange (TSXV) is a junior mining leader on a global scale. With operations covering Africa, South America, and Asia, TSXV-listed miners have complicated ESG issues to contend with.

The Canadian government promotes sustainable resource development, while guidance on ESG disclosure comes from the Toronto Stock Exchange. Yet juniors have restricted budgets, which challenge them to make thorough ESG reports.

Does this lead to a question: can small exploration companies achieve the same level of ESG expectations as international majors? More and more investors require even early-stage companies to show commitment to safety, diversity, and community relations. Those that manage to accomplish that can secure financing from ESG-dedicated funds.

Global Markets and Convergence

Except for ASX and TSXV, global exchanges and regulators are converging on ESG frameworks. The International Sustainability Standards Board (ISSB) is to develop harmonised reporting rules. The EU’s Corporate Sustainability Reporting Directive (CSRD) and the US SEC’s climate disclosure rule proposals put more pressure on it.

For global miners, the convergence implies that ESG reporting can no longer be an exercise in box-ticking. Investors demand standardised information, quantifiable targets, and clear governance across jurisdictions.

Can Expansion and Sustainability Coexist?

The essence of the argument is here: are mining firms capable of providing expansion and sustainability? The response is complicated.

The Resource Boom and Tension Over ESG

Critical minerals demand is exploding. The International Energy Agency predicts lithium demand may increase 40-fold by 2040. Copper, nickel, and cobalt will follow with record growth.

In order to achieve these goals, miners need to increase exploration, extraction, and processing. However, each operation threatens new environmental and social consequences. Mining expansions tend to conflict with Indigenous land rights, biodiversity conservation, and water shortages.

This poses a paradox: the green transition needs increased mining, but the world needs cleaner and more accountable mining.

Opportunities Through Technology

Technology provides solutions. Miners are embracing renewable energy at mines, powering haul trucks electrically, and using AI for optimisation. Tailings management, among the industry’s biggest environmental threats, is being enhanced with dry-stack technology and real-time monitoring.

Firms such as BHP are making significant investments in carbon capture, and juniors are increasingly powering remote operations with solar and wind.

Such technology reduces emissions and lowers long-term costs.

Miners adopt renewables, electric haul trucks, and AI to optimise operations.

Partnerships and Community Engagement

Sustainability is not just technology but also confidence. Most companies today construct collaborative ventures with Indigenous peoples, offer open revenue-sharing deals, and engage in local development.

Australian lithium miners, for instance, have collaborated with Traditional Owners to develop cultural heritage safeguards. Canadian explorers typically collaborate with First Nations to obtain permission before drilling.

Strong local partnerships decrease project delays and increase social licence to operate. In the current market, that licence is worth more than any mineral resource.

The Investor Perspective: Risk and Reward

Institutional investors see ESG as core to risk management today. For them, not performing on ESG can result in stranded assets, litigation, and reputational harm.

Access to Capital

ESG funds have expanded exponentially. Bloomberg puts ESG assets at potentially over US$40 trillion by 2030. Miners that meet ESG standards are able to raise funds at reduced costs, while laggards will find it difficult to attract capital.

For juniors, meeting ESG standards can provide access to strategic alliances with majors and government-backed funds. For majors, good ESG scores lower financing costs and enhance shareholder retention.

Bloomberg sees ESG assets topping US$40 trillion by 2030.

Scrutiny

Proxy advisers and activist investors more frequently confront boards on ESG deficits. Climate disclosure, Indigenous rights, and gender diversity resolutions appear with regularity at AGMs.

Those that do not engage risk shareholder uprisings. Those that showcase credible ESG progress, on the other hand, enjoy valuation premia.

Regional Case Studies

Australia: Balancing Heritage and Growth

Australia shows the premium risk of ESG blunders. The destruction of the Juukan Gorge in 2020 sparked international outrage, resignations, and lasting damage to the reputation of Rio Tinto. Miners have since revamped heritage preservation policies.

Presently, ESG systems in Australia focus on Indigenous consultation, water stewardship, and climate action. Miners extracting lithium and rare earths must now prove that their extraction of critical minerals won’t repeat the errors of the past.

Canada: ESG as a Financing Tool

ESG increasingly informs access to exploration capital in Canada. Many of the TSXV-listed juniors rely on joint ventures with majors to push forward their projects. Robust ESG frameworks enhance such arrangements.

The Canadian government also ties its critical minerals strategy to ESG, with the intent to make Canada a responsible supplier to world markets. For explorers operating in off-mainstream regions, Indigenous community partnerships are not negotiable.

TSXV juniors lean on majors for project growth.

Africa and Beyond: Global Responsibility

Several ASX and TSXV-listed miners have operations in Africa and Latin America. These areas have their own set of ESG challenges, such as governance risks, security risks, and infrastructure shortages.

Investors do not differentiate between geography when they expect miners to maintain global standards. Projects that are subpar in terms of ESG standards risk being excluded from worldwide supply chains, especially in Europe and North America.

Governance: The Forgotten ESG Pillar

While the environment and social concerns take centre stage, governance is still essential in mining. Poor governance undermines ESG credibility and investor confidence.

Board Oversight

Boards are also supposed to incorporate ESG into corporate strategy. This comprises establishing climate objectives, managing safety standards, and guarding cultural heritage. Lack of accountability at the board level tends to give rise to reputation crises.

For instance, after the Juukan Gorge collapse, Rio Tinto’s board was in the limelight. The message was clear: corporate governance should go beyond the compliance regime to active leadership.

Transparency and Anti-Corruption

Numerous mining initiatives have operations located in areas of high corruption risk. Investors expect clear financial disclosure, whistleblower safeguards, and robust anti-bribery regimes. Good governance failures can result in sanctions, project delays, and being shut out of capital markets.

With intensified enforcement by regulatory agencies such as the SEC and the EU, miners need to have governance systems matched to international best practice.

Indigenous Rights and Community Engagement

The confluence of mining and Indigenous rights is an identifying ESG issue. In nations such as Australia and Canada, indigenous land is protected in law, though on-the-ground outcomes differ.

Free, Prior, and Informed Consent (FPIC)

FPIC is a foundational element of global norms, such as the UN Declaration on the Rights of Indigenous Peoples. Miners should obtain true consent before exploration and development.

Not doing so can suspend projects forever. In contrast, firms that join fairly and early on can establish long-term relationships.

Case Study: First Nations Partnerships

A number of Canadian juniors have led the charge on revenue-sharing arrangements with First Nations. The arrangements yield financial advantages, employment, and cultural safeguards. Consequently, projects flow more unproblematically, with less litigation.

The Australian Context

In Australia, Traditional Owners and miners are working together more frequently to incorporate cultural heritage protection into project planning. It’s more than just compliance; it’s collaboration and mutual advantage.

The success of such cooperation confirms that respecting Indigenous rights is not only morally good but also financially advisable.

ESG and Critical Minerals: A Global Race

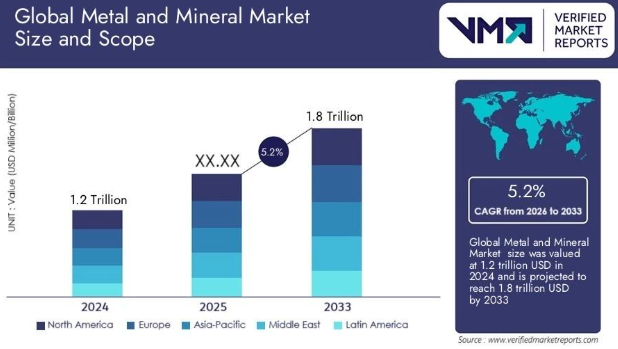

The transition to clean energy has brought minerals such as lithium, cobalt, nickel, and rare earths into the strategic list. Governments see an assured supply as part of economic security. The global metal and mineral market was estimated at USD 1.2 trillion in 2024 and is forecast to expand to nearly USD 1.8 trillion by 2033. This growth reflects a projected compound annual growth rate (CAGR) of 5.2% between 2026 and 2033.

National Strategies

Australia has positioned itself as a secure provider of critical minerals, with ESG as a differentiator.

Canada markets its critical minerals strategy based on responsible extraction and Indigenous partnerships.

The US and EU are now demanding traceability in mineral supply chains in order to ensure responsible sourcing.

Supply Chain Pressure

End-users like Tesla, Apple, and automakers require ESG compliance that can be verified by suppliers. This pressure cascades down to the miners, who are required to demonstrate that their materials conform to ethical and environmental standards.

Firms that do not meet them risk being shut out of such profitable markets. For juniors, firm ESG commitments can be the advantage between locking in offtake deals or falling behind.

ESG Ratings: Power and Pitfalls

ESG ratings agencies today hold a lot of power. ESG ratings from MSCI, Sustainalytics, and ISS can influence share prices, capital access, and investor opinion.

Challenges with Ratings

ESG ratings are inconsistent, according to critics. Two rating agencies may give the same company very different ratings. This frustrates investors and miners.

Nevertheless, ratings are still an important ingredient in the allocation of capital. Companies that explain clearly and document ESG efforts tend to earn higher ratings.

The Investor’s Dilemma

Investors must weigh ESG ratings against the sector’s essential role in decarbonisation. Some funds exclude mining entirely, citing environmental harm. Others adopt a “best-in-class” approach, supporting miners who lead on ESG practices.

This duality reflects the broader paradox of mining: indispensable for a green future, yet fraught with sustainability challenges.

Regulatory Pressures on the Horizon

The regulatory environment for ESG disclosure is tightening globally.

ISSB Standards

The International Sustainability Standards Board has introduced a worldwide baseline for ESG reporting. The standards aim to introduce consistency into climate and sustainability disclosures.

For miners, this translates to more scrutiny of carbon, biodiversity effects, and social risks.

SEC Climate Rules

In the United States, the Securities and Exchange Commission has issued proposed mandatory climate disclosures. While final rules are on hold, the direction is certain: investors demand detailed, standardised information.

EU CSRD

The EU’s Corporate Sustainability Reporting Directive broadens ESG disclosure to thousands of firms. Even miners who are not European but have supply chain relationships with the EU will feel the impact.

They will compel mining firms to improve data gathering, audit claims of ESG, and include sustainability in financial reporting.

Technology as an ESG Enabler

Innovation is at the centre of it all when reconciling mining expansion with sustainability.

Renewable Power Integration

Miners are also investing more in on-site renewable power. Solar farms, wind turbines, and battery storage cut diesel generator dependence, emissions, and costs.

As an example, Western Australian gold miners run hybrid power stations, mixing renewables with gas. This delivers reliable, low-carbon power in remote areas.

Automation and Efficiency

Technologies such as drones, artificial intelligence, and automation minimise environmental impacts. Precision blasting minimises waste, and AI-led exploration minimises unproductive drilling.

Automation improves safety as well by lowering human exposure to risky environments.

Waste and Water Solutions

Tailings management is among mining’s biggest risks. Innovations like filtered tailings, paste backfill, and sensor monitoring minimise the risk of failures.

Technologies in water recycling and desalination enable miners to perform in water-scarce areas, solving both environmental and social issues.

Investor Outlook: ESG as a Value Driver

Ahead, investors see the integration of ESG not as an expense but as a driver of value.

Valuation Premiums

Research indicates that firms with good ESG performance tend to have higher valuations. In mining, in particular, this is true due to the high levels of risk and the thinness of reputation.

Green Financing

Access to green bonds and sustainability-linked loans is increasing. These financing tools incentivise firms to achieve ESG goals at the cost of borrowing.

For instance, a number of miners have issued emission reduction or safety performance-linked bonds, directly connecting financial performance to sustainability metrics.

Green bonds and ESG-linked loans grow, rewarding firms with lower borrowing costs.

Capital Flight Risks

On the other hand, those who do not care about ESG risk face capital flight. Investors increasingly divest from poorly governed, environmentally controversial, or socially conflicted companies.

This bottom-line fact serves to strengthen the business case for adopting ESG.

Balancing Short-Term Costs with Long-Term Benefits

Critics also contend that ESG programs have upfront costs. For juniors with low budgets, installing full-scale ESG schemes can be cost-pressing.

Cost-Benefit Dynamics

Although it is true in the near term, ESG tends to realise long-term benefits. They are lower project delays, better community relationships, and cheaper energy.

Not investing in ESG can have much higher costs, such as lawsuits, reputational loss, and stranded assets.

Collaboration Models

Industry groups are increasingly supplying ESG toolkits specifically for juniors. Collaboration with NGOs as well as government agencies further facilitates affordable sustainability measures for small companies.

Through this synergy, ESG is not restricted to big producers but is made available throughout the industry.

Also Read: MinRex Reports Critical Mineral Finds at Fraser Range Project, WA

The Future of ESG in Mining

In the future, ESG will only strengthen. Clean energy transition relies on mining, but then that has to be sustainable.

Net Zero Mining

Businesses are implementing net-zero targets, with a view to reducing Scope 1, 2, and ultimately Scope 3 emissions. That means taking up renewable energy use, low-carbon processing, and supply chain cooperation.

Transparency and Digital Reporting

ESG reporting is moving away from static year-end reports towards live digital dashboards. Investors are demanding clear data, not showy assurances. Blockchain can have a part to play in the authentication of responsible sourcing.

Regulatory Convergence

Where ISSB standards are adopted, global standardisation will rise. This results in both majors and juniors having to hit similar benchmarks, irrespective of listing venue.

The Balancing Act

Mining firms cannot shirk the ESG discourse. Australia’s ASX to Canada’s TSXV, investors, regulators, and communities are all clamouring for evidence of good practices.

The sector is confronted with a paradox: the globe requires more minerals for the energy shift, but it needs cleaner and more equitable mining. The future is in technology, collaborations, and governance that is transparent.

Those who adopt ESG as an opportunity for growth rather than a constraint will come out on top. But can the industry reconcile growth with sustainability? The answer will determine the future of mining itself.

Conclusion: Mining’s Defining Test

The mining sector is at a fork in the road. Demand for minerals is skyrocketing, fueled by the transition to clean energy. However, the same process requires responsible and sustainable practices.

Markets such as the ASX and TSXV demonstrate the international pressure to incorporate ESG into each phase of mining. Ranging from reforms in governance and Indigenous peoples’ rights through renewable energy adoption, the sector has to adjust or else suffer atrophy.

The contradiction persists: mining is both integral to the problem and a key to the solution. The industry’s capacity to reconcile growth and sustainability will determine not just its future but the success of the world’s green transition.

Investors, regulators, and communities are paying close attention. For miners, the way ahead is certain: approach ESG not as compliance, but as strategy. Those who execute will lead the next generation of responsible resource development.