The global energy transition hinges on three critical metals that power our electric future: lithium, nickel, and cobalt. These battery metals form the backbone of lithium-ion batteries, driving electric vehicles, renewable energy storage, and consumer electronics worldwide.

As governments push ambitious net-zero targets and electric vehicle adoption accelerates, companies listed across major stock exchanges, the Australian Securities Exchange (ASX), TSX Venture Exchange (TSXV), and New York Stock Exchange (NYSE), find themselves at the epicentre of unprecedented demand growth.

Yet 2025 presents a complex landscape. While lithium demand surged 29% in 2024 according to the International Energy Agency, prices have plummeted 80% from their 2022 peaks due to oversupply. This dramatic shift creates both challenges and opportunities for mining companies worldwide, reshaping investment strategies and forcing producers to adapt quickly to volatile market conditions.

The stakes couldn’t be higher. Battery metals now represent the new oil of the 21st century, with supply chains concentrated in just a handful of countries creating geopolitical vulnerabilities that governments and companies are scrambling to address.

The Critical Foundation: Why Battery Metals Matter in 2025

Understanding the Battery Chemistry Landscape

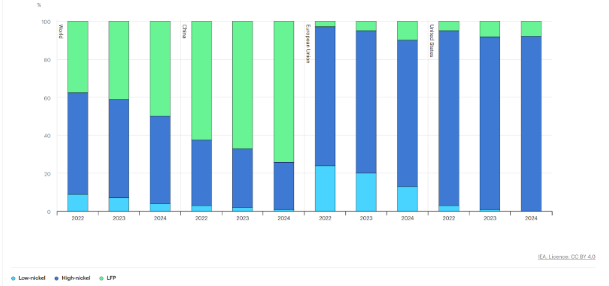

The battery chemistry revolution is reshaping metal demand patterns in ways few predicted just three years ago. Lithium Iron Phosphate (LFP) batteries now capture nearly 50% of the global electric vehicle battery market, surging from under 10% in 2020. This dramatic shift away from Nickel-Manganese-Cobalt (NMC) batteries carries profound implications for miners and investors alike.

LFP batteries eliminate cobalt entirely and drastically reduce nickel requirements, instead relying heavily on lithium, iron, and phosphorus. Tesla has embraced this technology for many of its vehicles, while Chinese manufacturers like BYD have made LFP their standard. The technology offers lower costs, approximately 30% cheaper per kilowatt-hour than NMC alternatives, though with slightly reduced energy density.

This chemistry shift has created winners and losers across the metals complex. Cobalt intensity in battery demand has dropped by two-thirds since 2020, while nickel intensity fell by nearly one-third over the same period. Meanwhile, lithium remains indispensable regardless of battery chemistry, cementing its position as the most critical battery metal.

Evolution of battery chemistry market share showing LFP’s rapid rise

2025 Market Dynamics and IEA Forecasts

The International Energy Agency’s Global EV Outlook 2025 paints a picture of explosive long-term growth tempered by near-term supply abundance. Lithium demand is projected to grow fivefold by 2040 under the Stated Policies Scenario, while nickel and graphite demand are expected to double.

However, the immediate outlook remains challenging. China’s lithium production has surged 55% since 2023, creating the oversupply conditions that have hammered prices. Current lithium carbonate prices sit at approximately 82,000 Chinese yuan per tonne, down from peaks exceeding 500,000 yuan in late 2022.

The supply concentration issue looms large over the entire sector. China refines 70-75% of global lithium, over 60% of nickel, and 78% of cobalt, while also controlling 90% of graphite processing. This concentration has prompted urgent supply chain diversification efforts, particularly following recent export restrictions on critical minerals technology.

Recent developments have added further complexity. In February 2025, the Democratic Republic of Congo announced a four-month suspension of cobalt exports to combat falling prices, while China imposed new export controls on lithium processing technology. These moves underscore the geopolitical dimensions increasingly shaping battery metals markets.

The IEA’s analysis reveals a sobering reality: excluding the largest supplier from global supply and demand balances shows that remaining supplies would cover only 35-40% of demand for graphite and rare earths, and less than 65% for lithium and cobalt. This “N-1” vulnerability highlights how seemingly well-supplied markets can become critically exposed to supply shocks.

Companies like St George Mining in Western Australia and other miners are responding by accelerating exploration programs to develop alternative supply sources, though these projects typically require years to reach production.

The paradox of 2025 is clear: while short-term oversupply pressures prices downward, long-term supply security concerns are driving unprecedented investment in new projects and technologies. This dynamic creates distinct opportunities for companies positioned across different parts of the cost curve and development timeline.

ASX-Listed Battery Metals Champions

Lithium Leaders on the ASX

Pilbara Minerals (ASX: PLS)

Pilbara Minerals

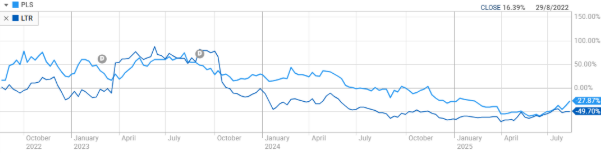

Australia’s lithium sector has endured a brutal reality check in 2025, with even the strongest producers feeling the pressure of collapsing prices. Pilbara Minerals (ASX: PLS), the nation’s flagship lithium producer, exemplifies both the sector’s potential and its current challenges.

Operating the massive Pilgangoora project in Western Australia’s Pilbara region, Pilbara Minerals has maintained its position as one of the world’s lowest-cost hard-rock lithium producers. The company’s operations deliver spodumene concentrate at approximately $578 per tonne, positioning it favourably even in the current downturn. Despite this competitive advantage, PLS shares have declined 58% since November 2022, reflecting the sector-wide carnage.

Recent quarterly results show the strain. While production volumes remain robust at over 180,000 tonnes per annum nameplate capacity, realised pricing has plummeted alongside global benchmarks. The company’s Battery Materials Exchange auctions, once fetching over $6,000 per tonne, now struggle to achieve $1,000 per tonne for similar-grade material.

Liontown Resources (ASX: LTR)

Liontown Resources

Liontown Resources (ASX: LTR) represents the next generation of Australian lithium producers, though its journey to profitability has proven rockier than anticipated. The company’s Kathleen Valley project achieved first production in 2024, reaching nameplate capacity of 500,000 tonnes per annum ahead of schedule, a rare bright spot in challenging conditions.

However, Liontown’s position in the 75th percentile of the global cost curve makes it particularly vulnerable to sustained low prices. Macquarie analysts recently warned that the company faces significant cash flow pressures if spodumene prices remain below $840 per tonne. The stock has surrendered 72% of its value since November 2022, despite securing offtake agreements with major players, including LG Energy Solution.

ASX lithium stocks performance showing the sector-wide decline

The sector’s struggles extend beyond the major players. Core Lithium (ASX: CXO) has placed its Finniss project in the Northern Territory on care and maintenance, despite having a Tesla offtake agreement in place. The decision underscores how even tier-one partnerships cannot shield producers from current market realities.

Yet institutional investors see opportunity in the wreckage. UBS analysts suggest Pilbara Minerals could deliver over 70% upside from current levels, citing its position in the 30th percentile of global cost curves and strong balance sheet with just 0.6x debt-to-EBITDA ratio.

Nickel and Cobalt Players

IGO Limited (ASX: IGO)

IGO Limited

The nickel sector presents an even more complex picture, with Indonesian supply domination creating oversupply conditions that have persisted through 2025. IGO Limited (ASX: IGO) has managed this environment better than most through its diversified portfolio approach.

IGO’s Nova operation produced 4,179 tonnes of nickel in Q3 2025, while the company’s 49% stake in the Greenbushes lithium mine provides crucial battery metals exposure. This diversification strategy has helped offset some nickel price weakness, though IGO shares remain down 70% from their 2022 peaks.

Ardea Resources (ASX: ARL)

Ardea Resources (ASX: ARL) offers a unique value proposition through its Kalgoorlie Nickel Project, which targets both nickel and cobalt production from the same resource base. The project’s 194.1 million tonne reserves could deliver 30,000 tonnes of nickel and 2,000 tonnes of cobalt annually, positioning Ardea to benefit from any recovery in either metal.

Smaller players like Pivotal Metals (ASX: PVT) continue advancing projects despite challenging conditions. The company’s Horden Lake project in Canada contains 72,000 tonnes of contained nickel, though development decisions await improved market fundamentals.

The Australian battery metals landscape in 2025 reflects a sector in transition, caught between long-term structural demand growth and near-term oversupply pressures that are reshaping the competitive landscape and testing even the strongest operators.

TSXV Innovation Hub: Canadian Battery Metals

Emerging Lithium Opportunities

Canada’s battery metals scene on the TSX Venture Exchange represents a fascinating blend of early-stage innovation and strategic geographic positioning. While lacking the production scale of Australian peers, TSXV-listed companies are carving out niches in recycling, processing, and emerging resource development that could prove crucial for North American supply chain security.

ION Energy (TSXV: ION)

ION Energy

ION Energy (TSXV: ION) exemplifies this next-generation approach through its diversified project portfolio spanning Mongolia and Canada. The company’s flagship Baavhai-Uul project covers 81,758 hectares in Mongolia’s lithium-rich region, targeting high-grade brine deposits that could deliver significantly lower production costs than hard-rock alternatives.

However, ION Energy’s journey reflects the broader challenges facing junior explorers in 2025. The stock has declined 41.67% over the past year, trading at just CAD 0.035 per share with a market capitalisation of approximately CAD 1.96 million. Despite this valuation compression, the company continues advancing exploration at both its Mongolian assets and the Bliss Lake pegmatite project in Canada.

Canada Nickel Company (TSXV: CNC)

Canada Nickel Company (TSXV: CNC) represents one of the most advanced nickel development stories on the TSXV, with its Crawford project in Ontario positioning Canada as a potential major nickel sulphate supplier for North American battery production. Recent drilling has delivered encouraging results, including 0.27% nickel over 452 metres, supporting the project’s resource base.

The company’s strategic value extends beyond raw nickel production. Crawford’s location in the stable, mining-friendly jurisdiction of Ontario offers a stark contrast to the geopolitical complexities surrounding Indonesian nickel operations. With a market capitalisation of approximately CAD 200 million, Canada Nickel trades at a significant discount to its international peers, reflecting both junior market conditions and development-stage risks.

Recycling and Processing Focus

Where TSXV companies truly differentiate themselves is in the emerging recycling and processing sectors, areas that could prove increasingly valuable as supply chain security concerns mount. RecycLiCo Battery Materials (TSXV: AMY) has positioned itself at the forefront of lithium-ion battery recycling technology.

The company’s proprietary process can recover over 95% of lithium, cobalt, nickel, and manganese from end-of-life batteries, creating a closed-loop system that reduces reliance on primary mining. With battery recycling projected to meet up to 80% of collection targets by 2040 in the IEA’s Net Zero Scenario, RecycLiCo’s technology could capture significant value from the growing waste stream.

Electra Battery Materials (TSXV: ELBM) operates one of North America’s few integrated cobalt and nickel refining facilities. Located in Ontario, the plant processes imported material into battery-grade chemicals for the North American market. This strategic positioning becomes increasingly valuable as automakers seek to comply with US Inflation Reduction Act requirements for domestic content.

The Canadian advantage extends beyond individual company merits. Political stability, established mining regulations, and proximity to major North American battery manufacturers create inherent value that current market conditions may underestimate. Companies like Patriot Battery Metals continue advancing projects despite challenging equity markets, betting on long-term supply chain restructuring.

However, the junior explorer landscape remains brutal. Many promising names have seen market capitalisations compress by 70-90% since 2022 peaks, creating potential opportunities for patient investors but also highlighting the sector’s inherent volatility and execution risks.

NYSE Giants: Global Scale and Integration

Established Lithium Producers

The New York Stock Exchange hosts the world’s most established lithium powerhouses, companies with the scale and integration capabilities to weather market volatility while positioning for long-term growth. These giants operate across continents, control crucial resources, and maintain the financial firepower necessary to sustain operations through challenging cycles.

Albemarle Corporation (NYSE: ALB)

Albemarle Corporation

Albemarle Corporation (NYSE: ALB) stands as the undisputed leader in global lithium production, with a market capitalisation of approximately $10 billion despite recent share price pressures. The company’s integrated approach spans from upstream brine operations in Chile’s Salar de Atacama to downstream lithium hydroxide production facilities across multiple continents.

Albemarle’s strategic advantages became evident during Q1 2025 earnings, when the company demonstrated superior contract management compared to peers. While spot lithium prices collapsed, Albemarle’s long-term supply agreements with major customers including Panasonic and Samsung provided crucial revenue stability. The company’s Greenbushes mine in Australia, operated through a joint venture with Tianqi Lithium, produced 1.38 million tonnes of spodumene concentrate in fiscal 2024, making it the world’s largest lithium-producing mine.

Recent developments underscore Albemarle’s commitment to North American supply chain security. The company secured $150 million in US government funding to support construction of a commercial-scale lithium concentrator facility, while receiving an additional $90 million critical materials award from the Department of Defense. This backing reflects Washington’s recognition of Albemarle’s strategic importance in reducing Chinese supply chain dependence.

Sociedad Química y Minera (SQM) (NYSE: SQM)

Sociedad Química y Minera (SQM) (NYSE: SQM) leverages Chile’s extraordinary lithium endowments through its operations in the Salar de Atacama, one of the world’s highest-grade brine deposits. With a market capitalisation of $10.82 billion, SQM represents the largest pure-play exposure to Chilean lithium resources available to international investors.

The company’s recent partnership with state-owned copper giant Codelco received regulatory approval in April 2025, marking a crucial milestone in expanding Atacama output. This deal provides SQM with enhanced quota allocations while ensuring continued access to world-class brine resources. However, Q1 2025 results showed the impact of weak pricing, with total revenues declining 4% year-over-year despite stable production volumes.

Lithium Americas (NYSE: LAC)

Lithium Americas (NYSE: LAC) represents the next generation of North American lithium development through its flagship Thacker Pass project in northern Nevada. With a market capitalisation of USD 719.1 million, the company trades at a significant discount to established producers, reflecting development-stage risks and capital requirements.

The Thacker Pass project claims to host the “largest known measured lithium resource and reserve in the world,” positioning it as a cornerstone of US domestic lithium supply. The joint venture with General Motors (38% stake) provides both financial backing and secured offtake, while USD 250 million in funding from Orion Resource Partners enables Phase 1 construction through to completion, targeted for late 2027.

Diversified Mining Giants

The world’s largest mining companies provide diversified exposure to battery metals through their sprawling global operations, offering investors broad-based leverage to the energy transition while maintaining exposure to traditional commodities.

BHP Group (NYSE: BHP), with a market capitalisation of $131.6 billion, generates battery metals exposure primarily through its Nickel West operations in Australia. While nickel represents a relatively small portion of BHP’s overall portfolio compared to iron ore and copper, the division’s high-grade operations produce battery-grade nickel sulphate crucial for NMC battery production.

BHP’s strategic positioning extends beyond pure production metrics. The company’s massive scale provides financial resilience during commodity downturns while enabling substantial capital allocation toward battery metals expansion when market conditions improve. Recent presentations indicate a continued commitment to nickel operations despite challenging near-term fundamentals.

Vale (NYSE: VALE) offers perhaps the most significant nickel exposure among diversified miners, with operations spanning Canada, Indonesia, and Brazil. The company’s Canadian operations produce Class I nickel suitable for battery applications, while Indonesian facilities target the stainless steel market through lower-grade material.

Vale’s battery metals strategy encompasses both nickel and cobalt production, with cobalt recovered as a byproduct from nickel operations. The company’s market capitalisation of USD 44.6 billion reflects its position as one of the world’s largest mining companies, though nickel price volatility continues impacting overall profitability.

The integration advantage of NYSE-listed giants becomes apparent during market stress. While junior explorers struggle to access capital and maintain operations, companies like Albemarle and SQM can sustain development programs, acquire distressed assets, and position for the next upcycle. This financial resilience, combined with established customer relationships and operational expertise, reinforces their competitive moats in an increasingly challenging environment.

Investment Landscape: Opportunities and Risks

Which Companies Stand to Benefit

The current battery metals downturn is creating a classic case study in competitive positioning, where cost structure and balance sheet strength separate survivors from casualties. Investors seeking exposure to the eventual recovery should focus on companies occupying the lowest quartiles of global cost curves while maintaining financial flexibility.

Pilbara Minerals exemplifies this winning formula through its position in the 30th percentile of global lithium costs, combined with a conservative debt-to-EBITDA ratio of just 0.6x. This financial strength enables the company to maintain operations and even consider acquisitions while competitors retreat. Similarly, Albemarle Corporation benefits from contract diversification and processing integration that provides earnings stability during price volatility.

ESG considerations are becoming increasingly critical as automakers face pressure to ensure ethical sourcing throughout their supply chains. Companies like Canada Nickel Company positioned in stable jurisdictions with strong environmental regulations command premiums over operations in countries with governance concerns. The Democratic Republic of Congo’s recent cobalt export suspension highlights how political instability can disrupt supply chains, making Canadian and Australian assets more attractive despite higher operating costs.

Recycling plays an expanding role in investment narratives. RecycLiCo Battery Materials and similar companies positioned in battery waste processing could capture significant value as the first generation of EV batteries reaches end-of-life around 2030-2035. The IEA projects recycling could meet 80% of collection targets by 2040, creating substantial revenue opportunities for early movers in this space.

Key Risks and Watch Points

The battery metals sector faces unprecedented uncertainty across multiple dimensions, with traditional supply-demand models challenged by rapid technological shifts and geopolitical tensions. Price volatility remains the most immediate concern, with lithium prices demonstrating their capacity for dramatic swings, from 2021 lows to 2022 peaks and back to multi-year lows by 2025.

Technology disruption presents both threats and opportunities. Sodium-ion batteries require no lithium, nickel, or cobalt, potentially reducing demand for traditional battery metals. While current energy density limitations restrict sodium-ion applications, rapid improvements could threaten market assumptions about future metal requirements.

Geopolitical risks continue escalating. China’s recent export restrictions on lithium processing technology, combined with the Democratic Republic of Congo’s cobalt export suspension, demonstrate how supply chain concentration creates vulnerability to trade disruptions. The US Inflation Reduction Act requirements for domestic content add another layer of complexity for companies serving North American markets.

Oversupply conditions may persist longer than many investors anticipate. Chinese production capacity continues expanding despite current losses, supported by vertically integrated companies that can absorb mining losses through downstream profits. This dynamic could suppress prices well into 2026, testing the financial reserves of even well-positioned producers.

Environmental and social governance risks are rising as scrutiny intensifies around mining practices. Water usage in lithium brine operations faces increasing regulatory pressure, particularly in Chile’s Atacama Desert, while indigenous land rights concerns affect project development timelines across multiple jurisdictions.

Future Outlook: Navigating the Battery Metals Transition

The long-term fundamentals supporting battery metals demand remain robust despite near-term market turbulence. Global decarbonization initiatives continue expanding, with grid-scale energy storage installations projected to add 78GW globally in 2025, requiring approximately 45,000 tonnes of lithium. This application represents growing diversification away from pure EV demand, providing additional demand pillars that could support price recovery.

Supply chain diversification efforts are accelerating across multiple fronts. The US Department of Energy continues deploying billions in critical minerals funding, while European initiatives like the Critical Raw Materials Act mandate supply source diversification. These policy frameworks create structural support for non-Chinese producers, potentially commanding premium pricing for “friend-shored” materials.

Technological innovation offers multiple pathways for market evolution. Direct lithium extraction (DLE) technology could unlock previously uneconomic brine resources while reducing environmental impact. Companies like Cornish Lithium in the UK and various Nevada-based projects are pioneering these approaches, potentially reshaping global supply geography.

Recycling infrastructure development accelerates as the first generation of EV batteries approaches end-of-life. Tesla’s battery recycling initiatives and partnerships with companies like Redwood Materials signal growing industry commitment to circular economy principles. This trend could reduce primary mining pressure while creating new revenue streams for recycling specialists.

The investment timeline for battery metals recovery likely extends into 2026-2027, when demand growth could finally outpace supply additions. Companies surviving the current downturn with strong balance sheets and low-cost operations should benefit disproportionately from any price recovery, making current valuations potentially attractive for patient capital.