ResMed (ASX: RMD) is a global medical technology company focused on digital health and respiratory care. It designs cloud-connected devices and software for sleep apnea, COPD, and other chronic ailments.

For fiscal year 2025, which ended on June 30, the revenues totalled $1.35 billion. This represents a 10% increase compared to revenues in the same quarter last year.

The company realised a 19% growth in GAAP operating income, which reached $454.5 million. Non-GAAP operating income was reported at $476.4 million.

GAAP net income was reported $379.7 million, or $2.58 per diluted share. Non-GAAP net income was tallied at $375.4 million, or $2.55 per diluted share.

The revenues and the earnings per share were also above analyst estimates. Such strong results reaffirm the company’s powerful presence on the ASX.

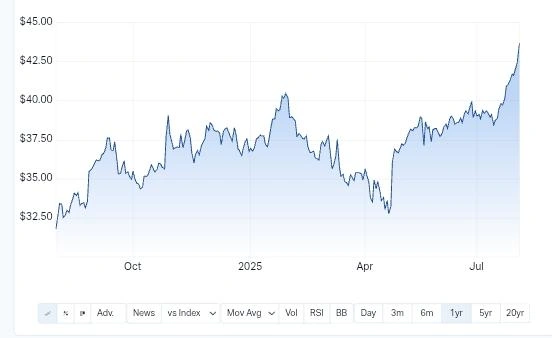

RMD ASX Chart

Why Did ResMed’s Revenue Rise?

Revenue went up thanks to product-mix shifts and wider global coverage. In Q4, devices brought in 52% of revenue.

Masks and accessories lent 36% to revenue, with SaaS and other software services contributing the remaining 12%. The Americas formed 58% of total revenue.

Europe, Asia, and other countries brought in 30%.The remaining 12% comes from software services in the U.S. and Germany.

ResMed has reported strong demand in non-invasive ventilation and the sleep apnea markets. Cloud-connected devices support better patient engagement and provider insight.

This technological advantage improves sales volumes and the long-term value of the platform in terms of capital appreciation.

Operating Margins and Cash Flow Strengthen

In the concluding quarter, gross margin rose to 60.8%, up by 230 bps compared to the last year. According to the non-GAAP method, the gross margin was 61.4%. The operating cash flow was $539 million for Q4.

For the full year, the operating cash flow remained $1.75 billion. With a free cash flow of $1.7 billion for FY2025, the figure rose 28% Y-o-Y. Strong cash flows allowed ResMed to step into a net cash position.

The company had a cash balance of $1.21 billion at the end of the quarter. There was a total debt of $668 million, with net cash of $541 million.

ResMed also has unused borrowing capacity to the tune of $1.5 billion. With such possibilities ahead, the company has numerous options to either invest, acquire, or return capital to shareholders.

What Strategic Moves Did the Company Make?

Innovation and acquisition were the main points of focus. ResMed spent roughly 7% of revenue on R&D in FY2025. It continues to jointly build its portfolio of patents and software ecosystem.

In Q4, ResMed finalised the acquisition of VirtuOx. VirtuOx is a U.S.-based independent diagnostic testing provider. This acquisition strengthens ResMed’s at-home sleep diagnostic capability.

It fits into the company’s vision of decentralised, digital-first healthcare. CEO Mick Farrell stated that VirtuOx would provide wider access to home sleep testing in key markets. The move apropos supports ResMed’s act to enter into end-to-end digital health pathways.

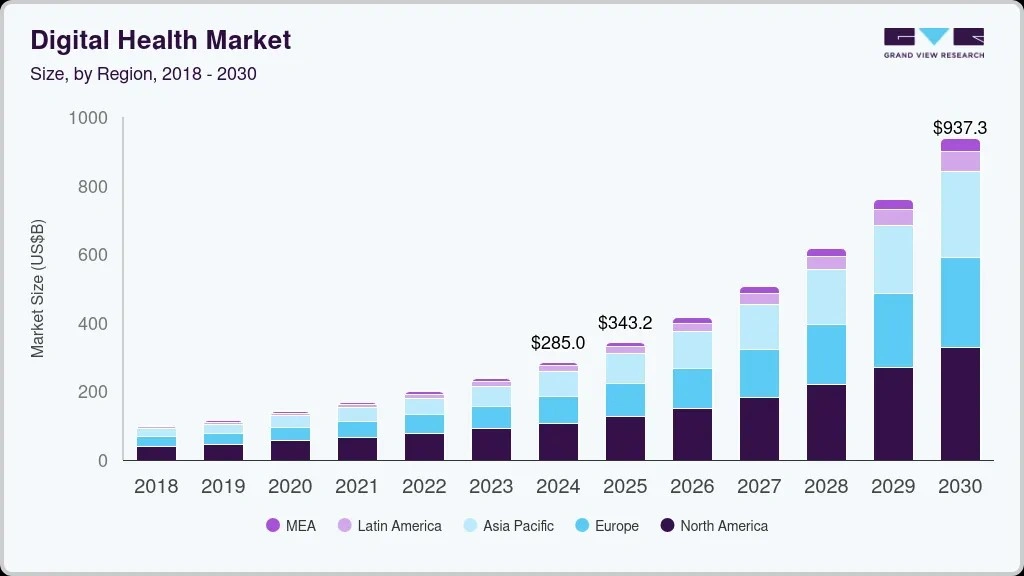

Digital Health Market to Surpass USD 946 Billion by 2030

It is estimated that by 2030, the global digital health market will exceed US$ 946 billion, with a CAGR of 22.2% from 2025 onwards. The rise in smartphone usage, better internet access, and higher demand for remote patient care fuel the growth.

Chronic disease management and government-health tech initiatives stand equally as dominant drivers. Telehealth holds the largest market share, with digital health services dominating all regions of the world.

How Did Investors React on the ASX?

After the earnings release, ResMed shares inched higher on the ASX.

Investors positively responded to the revenue beat and greater-than-expected free cash flow. The move to a net cash position was welcomed, too.

The analysts identified enhanced cost control and better margin scenarios as the key highlights.

While foreign exchange conversion headwinds remain, operational robustness still lies. ASX listing continues to offer Australian investors a stake in global health tech expansion.

Also Read: Pilbara Minerals Reports Strong June Quarter Performance Despite Price Pressures

Conclusion: What Lies Ahead for ResMed?

Entering 2026 with financial momentum and strategic clarity. The balanced sources of revenues create a strong cash flow with minimal debt load for future stability.

R&D and M&A continue to sit at the heart of its innovation pathway. Strong interest in cloud-connected devices feeds its software-for-scale business.

Therefore, ResMed is flexible with the digital respiratory care market growth. Being listed on the ASX allows investors direct exposure to the future growth of global health solutions.

Patients are shifting their expectations for care more toward digital and at-home, which is the recipe ResMed is solving for. The FY2025 results cement the

The company’s position is on top of both devices and data-driven care.