Australians Seek Stronger Cover Amid Rising Costs

Australians continue prioritising home insurance as climate risk and property values push premiums higher. The average cost of home insurance in Australia stands at $1,460 annually. This equates to around $121 per month, based on recent data.

Premiums Vary Across States and Territories

Queensland records the highest average premium at $1,692 annually. The Australian Capital Territory follows with $1,634. Western Australia averages $1,504 while New South Wales sits at $1,479. Northern Territory households pay around $1,400. Victoria’s average stands at $1,370, while South Australia and Tasmania are lower at $1,139 and $1,114 respectively.

Average annual premium in different states of Australia

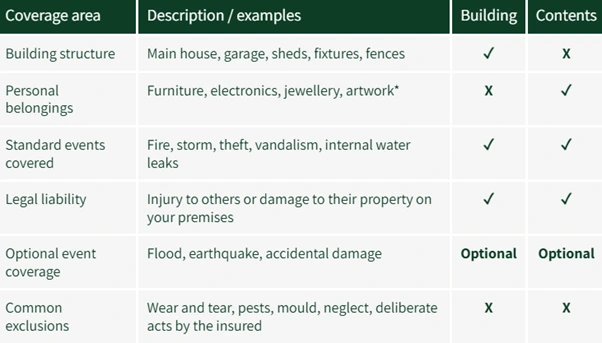

Understanding the Key Types of Home Insurance

Homeowners can choose from several insurance types based on property use. Building insurance covers the physical structure of the home. It includes fixed items such as floors, roof and walls. It usually comes with liability cover if someone is injured on the premises. Contents insurance applies to belongings inside the home. It covers furniture, electronics and personal items. Renters use the same cover, often labelled renter’s insurance. Combined home and contents insurance offers both cover types in one policy. It remains the most comprehensive option available. Landlord insurance is separate and protects rental properties. It adds cover for rental income loss and tenant damage. This guide does not assess landlord insurance.

What Home Insurance Typically Covers

Most policies protect against events like fire, storm damage and theft. However, exclusions vary. Reading the Product Disclosure Statement is essential. It outlines the full scope and limitations of cover. Policies may exclude damage from wear and tear, mould or vermin. Damage from renovations or if the home remains unoccupied may also require special conditions.

Coverage under Home Insurance

Key Terms to Understand Before Buying a Policy

The excess is the amount the policyholder pays when making a claim. A higher excess often means lower premiums. Lower excess options increase premium costs. Some policies allow a $0 excess. Others go as high as $5,000. Additional excesses may apply during home renovations or when the property is vacant.

The insurance premium is the regular amount paid to maintain cover. It can be paid monthly or annually. Annual payments sometimes attract a discount. Premium costs depend on both controllable and uncontrollable factors. Controllable factors include the type of cover, excess amount and applicable discounts. Uncontrollable factors include property location, building materials and proximity to emergency services.

Steps to Make a Home Insurance Claim

The policyholder must report the case to the insurer in writing in case an incident occurs. In this regard, a claim form is filed, and it should be supported by the relevant evidence such as the receipts, photos, or official reports. When they can evaluate the claim, payment will be given out to the policyholder with respect to the payment after deducting any excess relating to the policy.

Strategies to Save on Home Insurance in 2025

- Australians can lower premiums by shopping around instead of auto-renewing.

- Comparing policies at renewal helps secure competitive rates.

- Buying a new policy online can save up to 30% in the first year.

- Bundling policies can provide further discounts, such as combining home and car insurance.

- Installing security devices like smart sensors and alarms can attract discounts.

- Insurers may reward regular home maintenance with reduced premiums.

- Choosing a higher excess can also lower premiums.

- Policyholders must pay more out-of-pocket if they make a claim with a higher excess.

Also Read: Stranger Things 5 Teaser Unleashes Final Showdown in Hawkins

Home Insurance Remains Essential Amid Increasing Risks

Extreme weather events and bushfire risks continue driving demand for reliable insurance. A well-chosen home insurance policy protects both property and possessions. Consumers benefit from understanding available cover types, excess options and cost factors. Comparing providers annually helps ensure policies remain cost-effective.

Home Insurance Must Be Tailored to Individual Needs

Every household has different needs based on ownership, location and lifestyle. Renters need contents insurance to cover belongings. Homeowners need building insurance to cover the structure. A combined policy may best suit those seeking comprehensive protection. Checking exclusions, limits and claim processes remains important. Selecting the right policy helps ensure financial security when unexpected events occur.

Insurers Offer Flexibility and Incentives to Policyholders

Some insurers allow customisation of cover levels. Others reward no-claim periods or long-term customers with loyalty discounts. Flexible excess choices and online account management tools support customer convenience. Clear documentation and responsive claims handling also help customers manage their policies effectively.

Conclusion

Home insurance is a much-needed protection for Australian homes and their valuables. The premiums vary across regions and, therefore, policyholders benefit through rational considerations of their alternatives. Through the examination of the policy clauses, bargaining over anything above the necessities, and a right maintenance of the property, Australians can easily control the insurance spending and at the same time obtain the coverage befitting their situations.