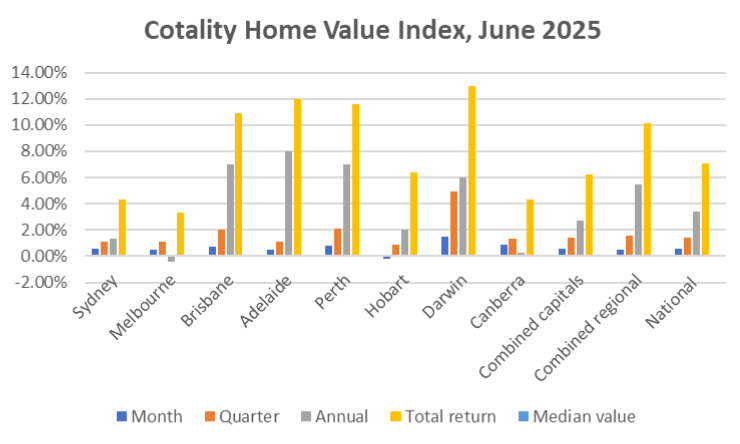

Australia’s increasing cost of living is crippling people’s daily lives. Regardless of the actual inflation or tax rate data, a Sky News report mentions that mental health has worsened for nearly 50% of Australians due to the cost of living crisis. A closer look at the June 2025 Cotality home value index shows that housing prices hit a new high in June as market confidence was bolstered by declining interest rates.

It doesn’t stop here. A 2024 report named “OECD Employment Outlook 2024” mentioned that, in Australia, real wages remain 4.8% below their pre-pandemic levels from the fourth quarter of 2019, marking one of the most significant declines among OECD nations.

So, it is evident that the country is sinking deeper into the cost of living crisis. But is there a way out? How can you manage your savings to make a way out of this crisis? Let’s find out in this article.

Spend Consciously: Your Phone Should Not Cost More Than Your Bank Balance

Overspending often happens not out of recklessness, but from a lack of visibility. Tapping your card or ordering takeout might seem harmless in the moment, but the costs pile up quickly. Some even buy expensive smartphones, which drain all the dollars from their banks.

Financial adviser Katrina Robbins says, “Don’t spend more than you earn – it’s the golden rule. It’s also about knowing where your money’s actually going.”

One of the best habits to build is a structured account setup:

- One for bills,

- One for everyday spending, and

- Another for savings or treats.

This way, your essential expenses stay protected, and you can clearly see where lifestyle choices are making an impact. The rent prices are rising by an average of $230 per month for many; tracking every dollar is now more important than ever.

Superannuation Is Super Important: Not a “Later” Problem

Many Australians think of superannuation as a “later” problem. But in a cost of living crisis, your super is one of the few tools you can leverage now to create long-term security.

“Super is your future freedom fund. Get it working for you now so you have choices later,” says Robbins.

Even small contributions above the minimum compound significantly over time. Without you even noticing it. Follow this super easy 3 steps procedure:

- Review your super fund,

- Check if you’re in the right investment option for your stage of life, and

- Consider salary sacrificing if possible.

Taking ownership of your super today means you’re building a cushion for tomorrow.

Financial Goals Should be Your No.1 Priority

Everything feels uncertain sometimes. You hit a moment when everything feels meaningless, crazy, twisted. How can you bring your motivation back to the work? It’s your financial goals. Having financial goals gives you direction and motivation. It might be as ambitious as buying a home or as practical as reducing debt or building an emergency fund.

Sit quietly for a few minutes. No phone, no interaction with anyone. And ask yourself: What do I want my money to do for me?

Robbins encourages people to connect their goals with their values. “See it, touch it, name it. That clarity keeps momentum going when things feel slow.” Maybe your dream is to help your children through uni. Or, maybe you want to travel the world. Whatever it is, setting intentional goals makes each dollar more meaningful.

During a cost of living crisis, it’s easy to lose sight of the bigger picture. Clear financial goals help you focus on what matters most and avoid lifestyle creep.

Review Regularly: Don’t Wait for Things to Go Wrong

Too often, people only review their finances when things go wrong. In this economic climate, that’s risky. Around 13.4% of the population, or roughly 1 in every eight people in Australia, lives below the poverty line as per 2022 data. More than 9 in 10 Australians (91%) say they feel at least moderately concerned about the rising cost of living, and women express greater worry than men. So, you can understand that proactive financial management has never been more crucial.

Think of this like dental hygiene, small, regular check-ups can prevent painful problems later. Look for better deals on bills, reassess spending patterns, and stay aware of changes in your income or expenses.

Don’t Be Ashamed; Seek Help

“There are financial hardship assistance programs available from many insurers, energy providers and home loan lenders,” notes Compare the Market’s economic director David Koch. Katrina mentions, “Know when you don’t know, and find people you trust.”

Guidance is everywhere if you just ask. It can Aust be a financial adviser, or your bank, or a budgeting coach, or a community support service. The main point is, don’t be ashamed to ask for help.

Facing the Future with Confidence

Australia’s cost of living crisis is not easing. Nearly half of Australians (48.7%) are experiencing increased mental health issues, such as anxiety or depression, due to ongoing cost-of-living pressures. Younger generations (Gen Z at 72% and Millennials at 56%) are most affected. Families are combining households, delaying moving out, or downsizing to maintain financial stability. However, if you follow these 5 steps, it won’t be very difficult to live a smart, financially-healthy life.