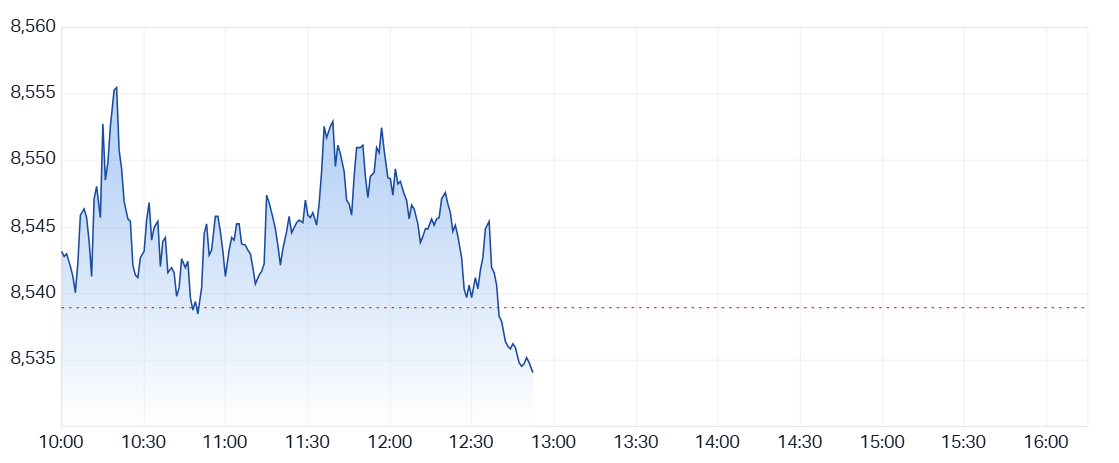

As of 12:52 pm AEST on 6 June, the S&P/ASX 200 index has slipped slightly by 4.90 points to sit at 8,534.00, down just 0.06% from the previous close of 8,538.90. Despite the marginal dip, market sentiment remains relatively steady with the index still up 1.18% over the past five days, and just 0.94% shy of its 52-week high of 8,615.20.

Earlier in the session, the ASX 200 touched an intraday high of 8,555.6 at 10:19 am, before retreating toward midday as sellers took over the momentum. The day’s low thus far has been 8,533.9, hovering just beneath its current level.

ASX 200 Midday Performance: June 6 2025 [Market Index]

Sector Overview: Defensive Plays Lead

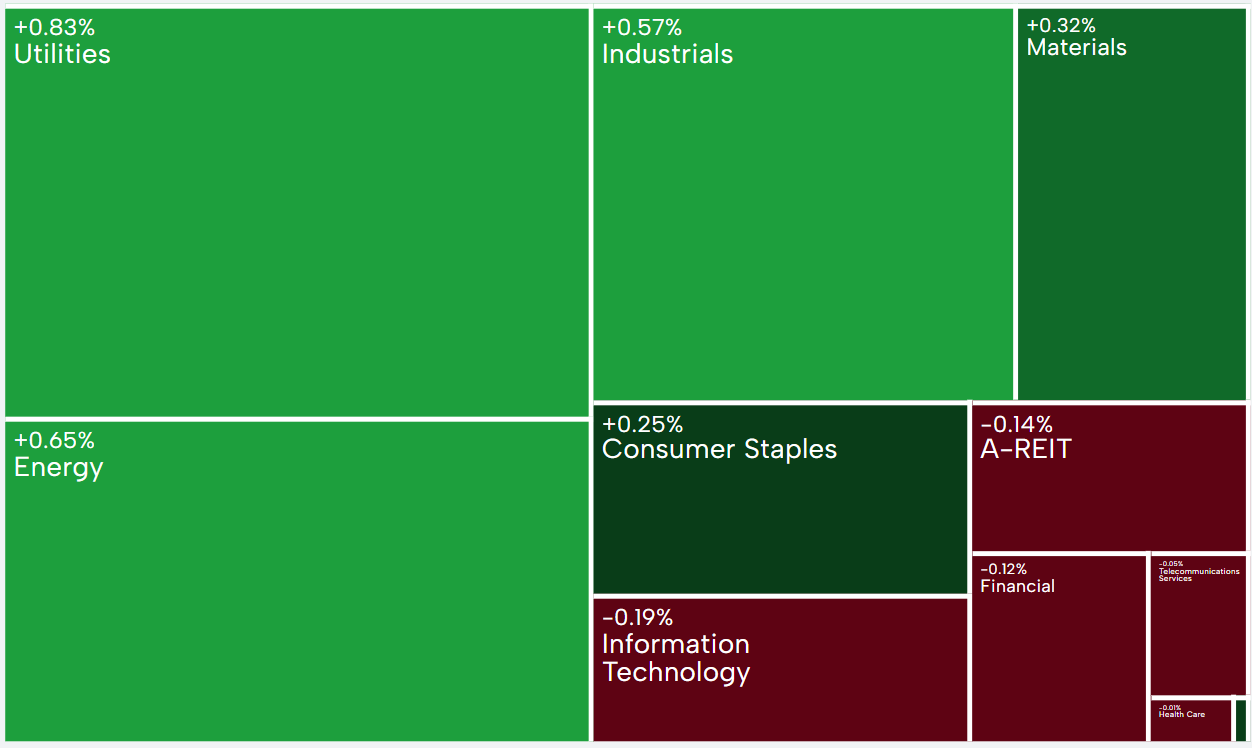

A glance at sectoral performance reveals a mixed bag for the Australian Stock Exchange at midday.

Utilities lead the gains with a +0.83% rise, closely followed by Energy at +0.65% and Industrials with a solid +0.57%. These defensive and cyclical sectors are proving resilient amid global macroeconomic uncertainties and appear to be drawing safe-haven interest.

Materials gained +0.32%, benefiting from selective strength in large-cap miners despite sharp losses in individual names like Pilbara Minerals and Liontown Resources.

On the other hand, Information Technology is the worst-performing sector with a decline of -0.19%, alongside A-REITs (-0.14%), Financials (-0.12%), and Telecommunications Services (-0.05%). The Health Care sector was largely flat, edging down -0.01%.

ASX 200 Sector Performance Heatmap [ASX.com.au]

Top Movers on the ASX 200

📈 Top 5 Gainers

- Whitehaven Coal Limited (WHC): Up 3.49% to $5.785, riding on strong coal demand and a favourable energy outlook.

- James Hardie Industries PLC (JHX): Rose 2.86% to $40.25, continuing its strong momentum from the U.S. housing recovery.

- Qantas Airways Limited (QAN): Up 2.74% to $10.685, as travel volumes remain robust ahead of the winter holidays.

- Nufarm Limited (NUF): Gained 2.14% to $2.145, supported by heightened investor interest as reflected in a 286% spike in trading volume.

- Alcoa Corporation (AAI): Climbed 1.75% to $43.03, tracking strength in aluminium futures.

📉 Top 5 Decliners

- West African Resources Limited (WAF): Fell sharply by 5.34% to $2.48, leading losses on the ASX 200.

- Pilbara Minerals Limited (PLS): Dropped 5.19% to $1.28 as lithium prices remain under pressure.

- Liontown Resources Limited (LTR): Down 3.88% to $0.62 amid a broader slide in small-cap mining.

- IGO Limited (IGO): Lost 3.69% to $4.18, impacted by negative sentiment across the battery metals space.

- Clarity Pharmaceuticals Ltd (CU6): Declined 3.65% to $2.245 on moderate volume.

Unusual Volume: Notable Trading Surges

Several stocks are trading at volumes significantly above their 90-day average:

- Light & Wonder Inc. (LNW): Volume surged 432%.

- IDP Education Limited (IEL): Posted a 362% jump in volume, totalling 2.75 million shares.

- Capstone Copper Corp. (CSC): Activity surged 304%.

- Nufarm Limited (NUF): Volume up 286%, reflecting its spot among today’s top gainers.

- Imdex Limited (IMD): Trading activity rose 273%.

These spikes suggest either investor repositioning ahead of macro events or potential speculative interest.

Market Outlook

Although the ASX 200 has seen a minor midday retreat, the broader trend remains positive. The index continues to hover near historic highs, with gains in defensive sectors like Utilities and Energy helping offset losses in Information Technology and REITs.

With investors parsing global inflation prints, interest rate signals, and commodity price trends, the Australian Stock Exchange is likely to remain sensitive to macroeconomic headlines. Any signs of resilience in commodities or stability in bond yields may continue to support risk sentiment on the ASX.

As we head into the afternoon session, traders will be closely watching whether the index can regain intraday highs or if profit-taking persists.