The Australian share market closed out a turbulent but ultimately positive week on Friday, finishing 1.8 per cent higher for the five trading days despite a bruising final session that saw technology stocks tumble and consumer names take a battering. The S&P/ASX 200 shed just 4.8 points on Friday, or 0.05 per cent, to settle at 9,081.4, while the All Ordinaries dropped 0.14 per cent as investors digested a flood of half-year earnings results and global macro signals.

So how did the market manage to end the week in the green? The answer lies in a rotation away from growth and discretionary stocks toward the more defensive corners of the market, utilities, financials and energy, which provided enough ballast to keep the index afloat.

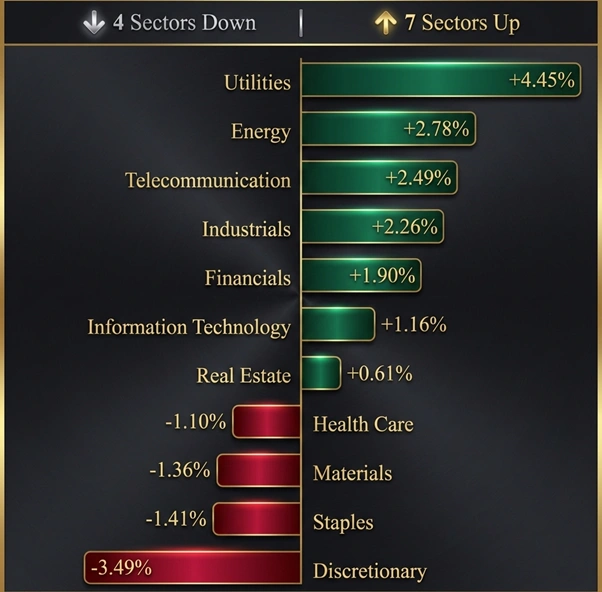

Financials and Utilities Did the Heavy Lifting

While six of the ASX’s eleven sectors closed Friday in the red, financials and utilities stepped up to absorb the damage. The S&P/ASX 200 Financials index (XFJ) has risen 8.39 per cent year-to-date and gained 16.77 per cent over the past year, making it one of the standout performers of 2026. The sector’s exposure to rising interest margins and strong insurance outcomes continues to attract investor interest.

Figure 1: ASX Sectors’ Performance in the Last Week

QBE Insurance led the financials charge on Friday, jumping 7.1 per cent after reporting better-than-expected investment returns alongside lower natural disaster claim payouts than the market had anticipated. It was the kind of clean, straightforward result that investors reward, and in a week dominated by messy earnings surprises, QBE’s clarity stood out.

Also Read: QBE Insurance Reports 21% Profit Growth in FY25 as It Sells Trade Credit and Surety Business

The utilities sector also punched above its weight. The S&P/ASX 200 Utilities index (XUJ) has now risen 18.42 per cent over the past year and gained 5.97 per cent year-to-date, reflecting the broader market’s growing appetite for defensive yield as interest rate uncertainty lingers. Utilities rose 0.73 per cent on Friday, bucking the broader trend.

Energy Stocks Rode the Oil Price Wave

Oil prices climbing to a six-month high gave the energy sector a meaningful lift throughout the week. Traders bid up crude prices on growing expectations of US military action against Iran, and ASX-listed energy companies captured that upside.

Woodside gained 1.2 per cent on Friday and Beach Energy added 0.9 per cent as both stocks rode the commodity tailwind. The S&P/ASX 200 Energy index (XEJ) has surged 13.46 per cent year-to-date and 15.16 per cent over the past year, one of the best-performing sectors on the local bourse in 2026.

Santos, meanwhile, struck a deal to supply 20 petajoules of gas per annum to the Whyalla Steelworks over 10 years, though the market took the news cautiously, with the stock slipping 0.9 per cent on Friday.

Also Read: Santos Locks In 10-Year Gas Deal to Fuel Whyalla Steelworks’ Green Iron Ambition

Tech Stocks Dragged — Again

The technology sector continued its painful descent. The S&P/ASX 200 Information Technology index (XIJ) has now fallen 19.55 per cent year-to-date and cratered 39.29 per cent over the past 12 months, cementing its place as the worst-performing sector on the ASX by a wide margin.

Friday brought more pain. Wisetech Global slid 3.8 per cent, a stock that has now fallen 26 per cent in the past month alone. Xero lost 3.7 per cent. Megaport suffered the sharpest blow, tumbling 11.8 per cent after its half-year results revealed an underlying net loss of $3.3 million. Despite strong jumps in revenue and annual recurring revenue, the market punished the company for failing to turn its top-line growth into bottom-line profit.

Consumer Stocks Took a Hit From Mixed Results

The consumer discretionary sector, which includes Lovisa and Wesfarmers, fell 1.44 per cent on Friday and has declined 4.02 per cent year-to-date. Consumer staples also dropped 1.44 per cent on the day, though the sector remains modestly positive for the year.

Guzman y Gomez delivered the week’s most dramatic consumer story, with shares plunging 13.9 per cent to a new record low after the Mexican-themed fast food chain reported half-year results showing stagnation in its critical US expansion strategy. EToro analyst Zavier Wong noted the result contained some positives, more customers through the door and encouraging profit signals, but the market focused squarely on the US growth concerns.

Baby Bunting, which had surged earlier in the week on strong results, gave back much of those gains on Friday as sellers cashed in, with the stock falling 6.1 per cent. Aristocrat Leisure, Nick Scali and Dusk Group each lost around 4 per cent, while Myer slipped 3.9 per cent.

The Bright Spots

Not everything went backwards. Defence contractor Austal surged 5.5 per cent after securing a $4 billion defence contract, a massive win that the market rewarded immediately. Telix Pharmaceuticals shot up 14.2 per cent after its accounts showed the biopharmaceutical company on track to crack $1 billion in revenue next year.

Gold miner Newmont bucked its sector, falling 4.9 per cent after flagging a 10 per cent dip in output while it upgrades mines across its global portfolio.

What It All Means

This week’s trading paints a clear picture of where investor confidence currently sits. Defensive income, financials, utilities, and energy attract buyers. High-growth tech and consumer-facing businesses face a more sceptical audience until they prove earnings can match their valuations. The ASX’s ability to finish the week positive despite these cross-currents reflects the underlying resilience of the market’s more established sectors, even as the growth trade continues to unwind.