Good first-half numbers were reported by Sims Limited, even though the commodity markets were mixed. The revenue stands at 3,778.6 million, an increase of 3.7%.

EBITDA underlying improved by 24.0 to become 249.8 million. Sub EBIT increased by 65.9 per cent to $121.1 million. Underlying NPAT increased by 70.9 per cent to $60.0million.

The margins increased in major operations. The management attributed pricing discipline and efficiency. The interim dividend increase was 40 per cent to 14 cents per share.

The Sims Limited has a global metals recovery business based on recycling and processing. [Sims Limited]

How Did Sims Limited’s FY26 Performance Improve Profits?

The results of the Sims Limited FY26 performance were supported by the increased prices of non-ferrous metals and the fast development of lifecycle services.

Trading margins remained strong despite the fact that ferrous markets remained soft. Underlying costs were increasing at a very low rate of 2.8 which was also lower than inflation. The ROI on capital has improved by 1.9 to 6.2.

There was a reduction of central overheads following the effort to restructure. There were also tighter working capital controls and cash discipline that favoured earnings. All these elements were combined to provide enhanced profitability within the group.

Metal Recycling Business Remains Stable

The metal division was the most significant contributor to the company. Segment revenue amounted to 3451.2 million. Volumes dropped 2.0%, with additional volumes going through unprocessed, needing additional treatment.

The percentage of trading margin remained constant at 19.6. The primary uplift was done by non-ferrous categories. The increased cost of aluminium and copper prices favoured realised sales values.

North America provided underlining EBIT of 53.3 million dollars. The Australian and New Zealand shares registered 21.5 million, even when the demand for ferrous was weak. Cost pressures were countered by operational efficiencies and reflected margins.

The metal division led revenue. Volumes fell, and more required extra processing. [Sims Limited]

What Drove Sims Lifecycle Services’ Surge?

The half was marked with outstanding growth by Sims Lifecycle Services. Revenue jumped 69.9% to $327.4 million. Repurposed units rose 17.8 per cent to 5.3 million. EBITDA increased by $171.8 million to $56.8 million.

Underlying EBIT increased by 247.5 per cent to 49.0 million. Memory shortages were backed with resale pricing- DDR4. The demand in hyperscaler was high throughout the world’s data centres.

Price gains contributed about 70 per cent of the growth in revenues. The capacity also increased in Ireland to focus on European demand by the business.

Balance Sheet And Cash Flow Stay Conservative

The balance sheet was strong throughout the period. Net assets stood at $2.5 billion. The gearing stood at 19.9, which is conservative leverage. The increase in working capital was attributed to better non-ferrous prices.

Approximately 70 million is associated with the hedge margin deposit. Turnover of cash continued to be healthy. The capital will be recycled through property sales and portfolio optimisation.

The goal of the management is to build liquidity as it finances specific growth projects. This strategy fosters stability through cycles of commodities.

Balance sheet strong; assets $2.5b, gearing conservative, working capital increased. [Sims Limited]

What Is The Outlook For The Second Half?

Non-ferrous markets and lifecycle services are expected to remain strong, according to the management. The constriction of DDR4 supply is expected to continue in 2027+. Domestic scrap demand may be supported by US tariffs.

The development of the electric arc furnace would tend to increase the recycling requirement in the long run.

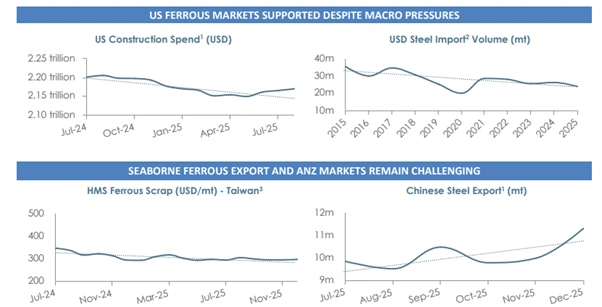

Nevertheless, the steel exports in China can continue to suppress the ferrous pricing. Sims intends to base its attention on margins and not volumes.

Efficiency initiatives and controlled utilisation of capital are still priorities. Shareholders will closely follow the adoption of the Sims Limited financial results for FY26.

FAQs

Q1: What were the key profit figures in 1H FY26?

A1: Underlying EBIT reached $121.1 million, and underlying NPAT was $60.0 million.

Q2: How much did revenue grow?

A2: Sales revenue increased 3.7% to $3,778.6 million.

Q3: What drove Sims Lifecycle Services’ growth?

A3: Strong DDR4 pricing and hyperscaler demand lifted revenue 69.9% and margins were sharply higher.

Q4: What dividend was declared?

A4: An interim dividend of 14 cents per share, up 40% year-on-year.

Strengths of the Earnings of FY26 of Sims Limited.