QBE Insurance has reported a 21% rise in net profit for the 2025 financial year and confirmed the sale of its global trade credit and surety portfolio to Swiss Re Corporate Solutions. The results highlight stronger underwriting performance and disciplined pricing across core divisions.

QBE Insurance Group reported a 21% rise in net profit for FY25, supported by stronger underwriting performance. [The Australian]

The insurer also recorded higher gross written premiums and improved margins. At the same time, QBE announced a strategic divestment designed to streamline operations and improve capital efficiency. These developments place QBE Insurance at the centre of market attention in early 2026.

QBE FY25 Earnings Results Show Strong Net Profit Growth

QBE Insurance Group reported a net profit after tax of approximately US$2.15 billion for FY25. This figure represents a 21% increase compared with FY24. The company attributed the rise to disciplined underwriting and improved risk selection.

Gross written premium reached about US$23.96 billion. That result marked a 7% increase from the previous year. QBE maintained pricing strength across several regions, which supported revenue growth despite competitive pressures in global insurance markets.

The company also improved its combined operating ratio to 91.9%. In FY24, the ratio stood at 93.1%. A lower combined ratio indicates stronger underwriting performance. Reduced catastrophe claims contributed to the improvement during the period.

QBE’s board increased the full-year dividend following the earnings release. Management stated that the balance sheet remains strong and well-capitalised. The company continues to focus on sustainable returns rather than volume-driven growth.

Underwriting Discipline and Investment Income Support Margins

QBE strengthened underwriting margins across its portfolio. Management maintained firm pricing in property, casualty, and specialty lines. This approach helped offset claims inflation in certain regions.

Lower catastrophe costs played a role in the improved result. Natural disaster losses remained manageable compared with previous years. That stability helped the insurer protect margins and preserve capital.

Investment income also supported overall performance. Higher interest rates boosted returns on fixed-income portfolios. The investment yield stood at about 4.9% during the year. Stronger investment returns complemented underwriting gains and lifted overall profitability.

The company emphasised portfolio optimisation as a key strategy. QBE reshaped underperforming segments and redeployed capital toward higher-return areas. These actions helped improve earnings quality and reduce volatility.

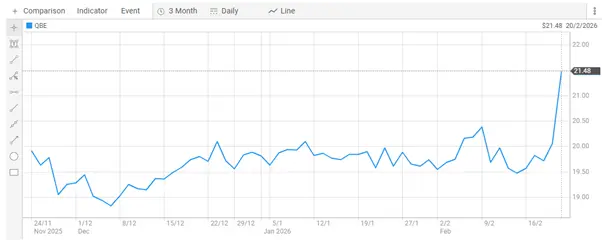

ASX Market Reaction Lifts QBE Share Price

The earnings announcement triggered a positive response on the Australian Securities Exchange. QBE shares rose around 7% following the release of results. Investors responded to stronger-than-expected profit growth and improved margins.

QBE net profit rose 21% in FY25, while gross written premiums increased 7% year-on-year. [ASX]

While QBE advanced, the broader ASX 200 index remained largely flat on the same trading day. The market showed mixed sector performance. However, QBE outperformed many financial stocks during that session.

The rally reflected investor confidence in the insurer’s strategy. Analysts noted that disciplined underwriting and capital management strengthened earnings resilience. The dividend increase also supported shareholder sentiment.

Trading volumes increased during the session. Market participants reacted quickly to the earnings data and forward guidance. The share price movement positioned QBE among the top performers on the exchange that day.

Swiss Re Acquisition of QBE Trade Credit and Surety Portfolio

Swiss Re confirmed that its Corporate Solutions division agreed to acquire QBE’s global trade credit and surety business. The transaction includes operations in Australia, the Pacific, and the United Kingdom. It excludes QBE’s French surety activities.

Swiss Re Corporate Solutions agreed to acquire QBE’s trade credit and surety portfolio. [Reuters]

The acquired portfolio generates approximately US$200 million in annual revenue. Swiss Re stated that the deal will strengthen its primary credit and surety insurance offering. The company expects to integrate experienced teams and established client relationships.

QBE described the sale as part of a broader strategic review. Management aims to sharpen focus on core underwriting segments. The company expects the divestment to improve capital allocation efficiency.

The transaction remains subject to regulatory approvals. Both parties anticipate completion in the coming months. Neither company disclosed the purchase price at the time of announcement.

Strategic Shift and Capital Allocation Focus

QBE has reshaped its portfolio over recent years. The sale of the trade credit and surety business aligns with this strategy. Management intends to concentrate resources on segments with stronger growth prospects and higher margins.

The insurer continues to evaluate capital deployment options. Leadership has prioritised disciplined growth, underwriting profitability, and balance sheet strength. The FY25 result reflects these priorities.

Swiss Re also signalled strategic intent. The acquisition expands its footprint in trade credit and surety insurance. Corporate Solutions aims to deepen client relationships in commercial insurance markets.

Both companies emphasised operational continuity. They stated that client service will remain stable during the transition. Staff transfers will support integration efforts once regulatory approvals are secured.

Insurance Industry Context and Competitive Landscape

Global insurers faced mixed conditions during FY25. Inflation influenced claims costs in several markets. At the same time, higher interest rates supported investment income across the sector.

Reinsurance capacity stabilised after previous volatility. Insurers adjusted pricing to reflect risk exposures. As a result, disciplined underwriting became central to performance outcomes.

QBE operates across multiple regions, including North America, Europe, and Asia-Pacific. Diversification has helped the company manage regional risk fluctuations. Stronger underwriting metrics in FY25 indicate improved risk management processes.

Swiss Re remains one of the world’s largest reinsurance groups. Its Corporate Solutions arm focuses on large and mid-sized enterprises. The acquisition of QBE’s trade credit and surety portfolio strengthens its commercial offering.

Also Read: Will Rising Interest Rates Pressure ASX Bank Profits in 2026?

Outlook for QBE Insurance and Market Implications

QBE enters FY26 with improved profitability and a streamlined portfolio. Management has signalled continued focus on underwriting discipline. The company also aims to maintain strong capital buffers.

Market participants will monitor catastrophe trends and claims inflation. These factors could influence underwriting margins in the coming year. However, QBE’s current financial position provides flexibility.

The divestment to Swiss Re may free up additional capital. QBE can redirect those funds toward growth initiatives or shareholder returns. The company has not announced further major asset sales at this stage.

Overall, QBE’s FY25 performance demonstrates stronger earnings momentum and strategic clarity. The profit increase, improved combined ratio, and portfolio restructuring mark significant developments for the insurer. Investors and industry observers will assess how these moves shape performance in FY26.

FAQs

- What was QBE Insurance’s net profit in FY25?

Ans. QBE Insurance reported a net profit after tax of approximately US$2.15 billion for the 2025 financial year. The result represents a 21% increase compared with FY24. Strong underwriting performance and disciplined pricing supported the growth.

- How much did QBE’s gross written premium grow in FY25?

Ans. QBE recorded gross written premiums of about US$23.96 billion in FY25. This reflects a 7% increase year-on-year. The growth came from pricing strength and portfolio adjustments across key regions.

- Why did QBE shares rise after the FY25 earnings announcement?

Ans. QBE shares increased by around 7% following the earnings release. Investors reacted positively to higher profit, improved underwriting margins, and a stronger combined operating ratio. The dividend increase also supported market sentiment.

- What is QBE’s combined operating ratio for FY25?

Ans. QBE reported a combined operating ratio of 91.9% in FY25. The ratio improved from 93.1% in FY24. A lower combined ratio indicates stronger underwriting profitability.

- What business is Swiss Re buying from QBE?

Ans. Swiss Re is acquiring QBE’s global trade credit and surety insurance business. The deal includes operations in Australia, the Pacific, and the United Kingdom. It excludes QBE’s French surety business.

- How much revenue does QBE’s trade credit and surety portfolio generate?

Ans. The trade credit and surety portfolio generates approximately US$200 million in annual revenue. Swiss Re stated that the acquisition will strengthen its commercial insurance platform.

- When will the Swiss Re acquisition of QBE’s portfolio be completed?

Ans. The transaction remains subject to regulatory approvals. Both companies expect completion in the coming months. They have not disclosed the purchase price.

- What does the QBE sale to Swiss Re mean for investors?

Ans. The sale allows QBE to sharpen its strategic focus and improve capital efficiency. Investors may view the move as part of broader portfolio optimisation. The company intends to concentrate on core underwriting segments.

- Is QBE Insurance financially stable in 2026?

Ans. QBE reported strong profitability, improved underwriting metrics, and solid capital levels in FY25. Management has indicated that the balance sheet remains well-capitalised. Future performance will depend on claims trends, catastrophe events, and market conditions.

{kind=link}