Australia’s largest listed insurers have delivered a mixed bag of results heading into 2026, with record catastrophe seasons, falling investment yields, and a resurgent health insurance market each pulling sector earnings in different directions. For investors watching the insurance stocks outlook 2026, the question is not whether the industry can grow, but whether it can do so without being derailed by the increasingly volatile Australian climate.

Here is how the five biggest insurance stocks on the ASX, ranked by market capitalisation, are positioned for the year ahead.

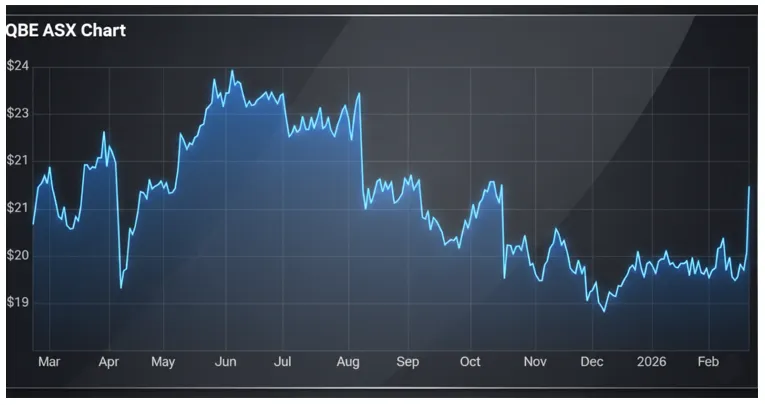

QBE Insurance Group (ASX: QBE) — Market Cap: ~$32.3 Billion

The standout performer of the group, QBE, closed out its full year to 31 December 2025 with statutory net profit after tax of US$2.16 billion, up sharply from US$1.78 billion in the prior year. Its adjusted return on equity hit 19.8%, and the combined operating ratio improved to 91.9%, the company’s strongest result in several years.

Also Read: QBE Insurance Reports 21% Profit Growth in FY25 as It Sells Trade Credit and Surety Business

Gross written premium grew 7% in constant currency, driven by targeted expansion across the North American and International divisions. QBE declared a full-year dividend of A$1.09 per share, a 25% lift on the prior year, with a 50% payout ratio.

Looking ahead, the company is guiding to a combined operating ratio of approximately 92.5% in 2026, with mid-single-digit constant-currency GWP growth and a medium-term adjusted ROE target of 15%+ or more. Even after a small share buyback, QBE’s balance sheet appears solid with a Prescribed Capital Amount multiple of 1.87x, which is comfortably above its target range of 1.6–1.8x. The insurer’s strong global diversification remains its key competitive advantage as domestic catastrophe costs remain elevated.

Figure 1: 1-year performance of QBE Insurance Group (ASX: QBE) stock on ASX

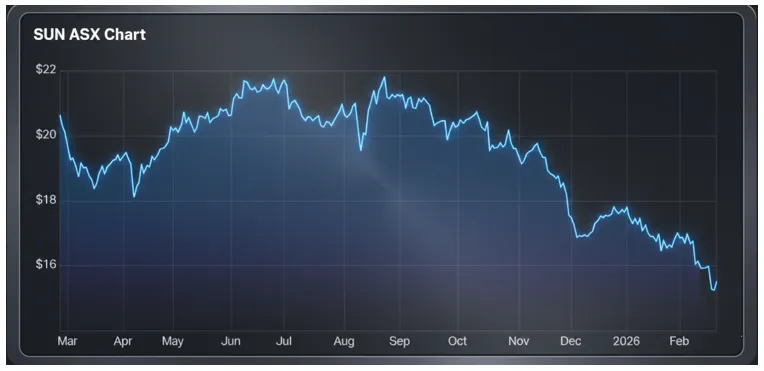

Suncorp Group (ASX: SUN) — Market Cap: ~$16.8 Billion

Suncorp’s first half of FY26 was defined by the weather. The group confronted nine declared natural hazard events, generating more than 71,000 claims at a net cost of around $1.3 billion a staggering $453 million above its half-year allowance. The resulting net profit after tax of just $263 million compared painfully against $1.1 billion in the prior corresponding period, and cash earnings fell to $270 million from $828 million.

Despite the headline numbers, Chief Executive Steve Johnston was keen to highlight the resilience of the underlying business. The underlying insurance trading ratio held at 11.7%, near the top of Suncorp’s 10–12% target range. Consumer gross written premium grew 6.3%, supported by motor and home unit growth, and the group completed $168 million of its $400 million on-market share buyback.

Suncorp’s balance sheet remains solid, with CET1 $700 million above the midpoint of its target range. The board declared a fully franked interim dividend of 17 cents per share. For the second half of FY26, management expects GWP growth around the bottom of the mid-single-digit range and underlying ITR to remain in the top half of the target band, a measured but credible outlook given the climate headwinds the sector faces.

Figure 2: 1-year performance of Suncorp Group (ASX: SUN) stock on ASX

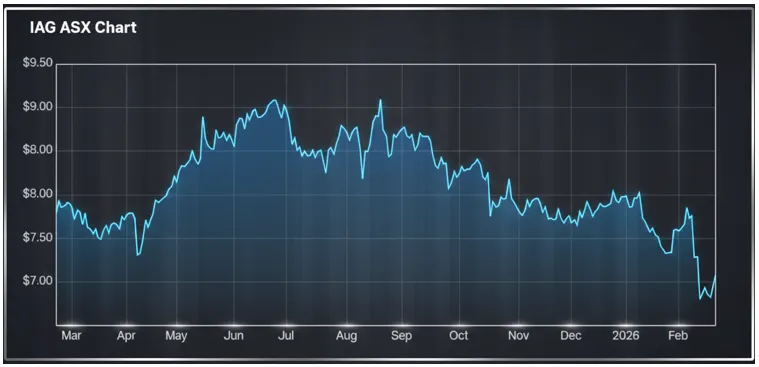

Insurance Australia Group (ASX: IAG) — Market Cap: ~$16.7 Billion

IAG’s 1H26 result told a tale of two numbers. Statutory net profit after tax of $505 million fell 35.1% from $778 million in the prior period, but the decline was heavily distorted by a one-off $174 million hit from its newly acquired RACQ Insurance (RACQI), struck hard by 17 Queensland weather events between September and December, before the business was folded into IAG’s global reinsurance program in January 2026.

Strip out that one-off, and IAG’s underlying insurance profit rose 7.6% to $804 million, with an underlying margin of 15.1%. Gross written premium grew 6% to $8.93 billion, buoyed by four months of RACQI contribution and solid underlying retail growth of around 4% in both Australia and New Zealand.

The board maintained its FY26 reported insurance profit guidance range of $1.55 billion to $1.75 billion, corresponding to a reported margin of 14–16%. IAG also announced an on-market buyback of up to $200 million. With RACQI now integrated into the reinsurance program, the path to the top half of that margin range looks increasingly achievable.

Figure 3: 1-year performance of Insurance Australia Group (ASX: IAG) stock on ASX

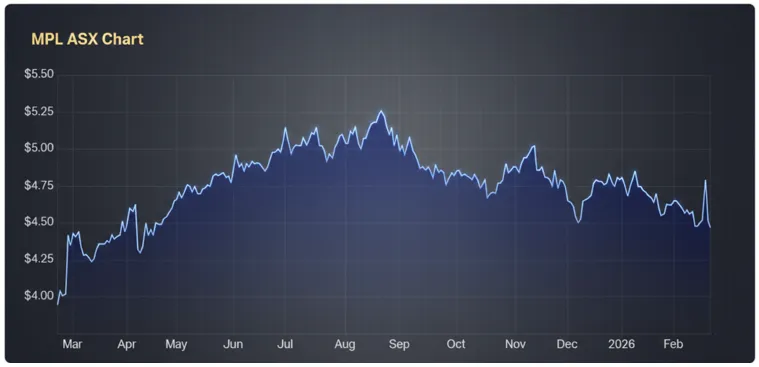

Medibank Private (ASX: MPL) — Market Cap: ~$12.3 Billion

Medibank’s result for the half year to 31 December 2025 was characterised by solid operational momentum beneath a weaker statutory headline. Reported net profit after tax fell 11% to $302.9 million, largely because the prior period had been boosted by a one-off $43.6 million COVID-19 reserve release. Underlying NPAT was essentially flat at $297.8 million, and group operating profit grew a healthy 6% to $381.7 million.

Health Insurance revenue rose 4.3% to $4.26 billion, and the company added 17,900 net policyholders in the half, more than double the prior period’s growth. Its rapidly expanding Medibank Health division posted segment profit growth of 28.5%, adding 61 GP clinics via the $163.5 million acquisition of Better Medical in December. The interim dividend was lifted 6.4% to 8.3 cents per share.

A $250 million APRA supervisory capital requirement linked to the 2022 cybercrime event remains in place, and ongoing class actions add to legal uncertainty. Still, the underlying growth story is compelling.

Figure 4: 1-year performance of Medibank Private (ASX: MPL) stock on ASX

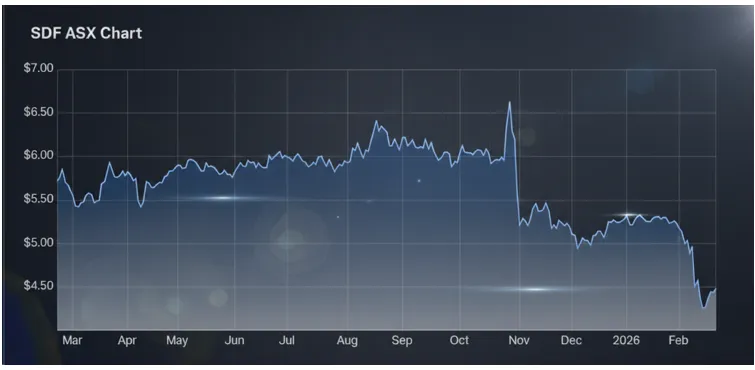

Steadfast Group (ASX: SDF) — Market Cap: ~$4.98 Billion

The smallest of the top five by market cap, Steadfast operates as an insurance broker and underwriting intermediary rather than a direct insurer, giving it a different risk profile. With a share price of $4.48 at the time of writing and a 2026 year-to-date decline of 15.15%, the market has been decidedly cooler on Steadfast than its larger peers. Earnings per share stands at $0.304, and the dividend yield is $0.195 per share.

Steadfast’s model, servicing a network of brokers and underwriting agencies across Australasia, Asia, and Europe, provides meaningful diversification. However, in a softening commercial insurance cycle with heightened competition from international capital, premium growth pressures could weigh on commission income in the near term.

Figure 5: 1-year performance of Steadfast Group (ASX: SDF) stock on ASX

Sector Verdict

The insurance stocks outlook for 2026 is one of cautious optimism. QBE leads the pack on profitability and capital strength. IAG and Suncorp are both navigating elevated catastrophe seasons with resilient underlying margins and share buybacks signalling balance sheet confidence. Medibank’s diversification into primary care positions it for longer-term growth, while Steadfast’s broker-centric model offers a different way to access the sector.

Climate risk is the defining variable for the year ahead. If Australia’s catastrophe season moderates in the second half, margins should recover sharply. If it does not, investors will need to look past the noise to the underlying insurance fundamentals, which, across the sector, remain broadly sound.