Harvey Norman has reported solid growth in its half-year results for the period ended December 2025. The retailer recorded higher system sales, stronger profit, and continued balance sheet strength. Management attributed the performance to momentum in Australian franchise operations and overseas company-operated stores.

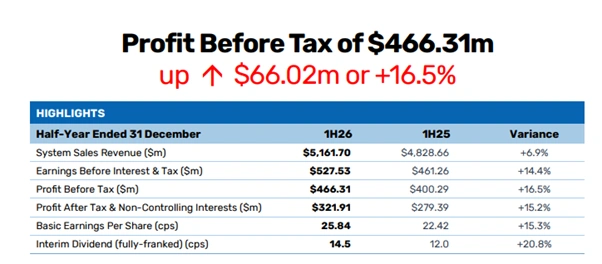

Harvey Norman reported a 6.9% rise in system sales to $5.16 billion in 1H26. [insideretail]

The company confirmed that system sales increased 6.9 per cent to $5.16 billion in 1H26. Profit before tax also improved, while earnings per share rose at a double-digit rate. The group maintained cost discipline and continued to expand its international presence.

System Sales Growth Driven by Franchise and International Momentum

Australian franchisees delivered steady performance during the half. Aggregated franchisee sales revenue increased 4.8 per cent to $3.50 billion. This growth contributed significantly to the overall system sales uplift.

Overseas company-operated stores recorded stronger growth. Aggregated sales revenue for those operations increased 11.6 per cent to $1.66 billion. International diversification remained a key contributor to earnings, with overseas operations accounting for 25 per cent of total profit before tax, excluding property revaluations.

Australian franchise operations contributed to overall sales growth during the half-year. [The Australian]

Management noted that strong performances in New Zealand, Singapore, Malaysia, Ireland, Slovenia and Croatia supported the result. The group also continued to invest in its United Kingdom operations, expanding product categories and store networks.

Profit Before Tax and Earnings Per Share Rise

The company reported a 16.5 per cent increase in profit before tax to $466.31 million. Excluding the net impact of AASB 16 and property revaluations, profit before tax rose 20.1 per cent to $372.79 million. These figures reflect operating improvements across segments.

Profit before tax increased 16.5% to $466.31 million in 1H26. [Harvey Norman]

Basic earnings per share increased 15.3 per cent to 25.84 cents. Management linked this improvement to disciplined expense control and higher sales volumes. Marketing expenses remained flat as a percentage of system sales, despite revenue growth. Marketing represented 3.8 per cent of system sales in 1H26, compared with 4.0 per cent in 1H25.

Operating expenses also improved as a proportion of sales. Operating costs accounted for 17.8 per cent of system sales, down from 18.0 per cent in the prior corresponding period. These results indicate tighter cost management while preserving brand presence.

Property Portfolio Supports Earnings Stability

The property segment continued to provide stable earnings and asset growth. The group’s global property portfolio stands at approximately $5 billion. Management described the balance sheet as tangible asset-rich and conservatively geared.

The company recognised a net property revaluation adjustment of $95.80 million in the income statement. It also recorded a fair value increase of $16.29 million for New Zealand properties on the balance sheet. These adjustments contributed to stronger reported earnings.

Property segment profit before tax increased 14.2 per cent to $205.93 million. The portfolio includes both freehold and leasehold properties across multiple countries. Management stated that property ownership supports long-term operational stability and financial flexibility.

International Retail Segment Delivers Standout Performances

The overseas company-operated retail segment recorded substantial growth. Profit before tax from this segment rose 32.3 per cent to $47.06 million. Several regions posted notable increases.

New Zealand delivered improved profit outcomes, supported by property valuation gains and retail momentum. Singapore and Malaysia also reported higher profit before tax, reflecting stronger consumer demand and improved margins. Ireland posted a 40.0 per cent rise in profit before tax to $25.08 million.

International operations delivered double-digit growth across several regions. [Harvey Norman]

Slovenia and Croatia produced significant percentage growth, with profit before tax rising 102.6 per cent to $5.44 million. These results demonstrate the benefits of geographic diversification. Management described international exposure as a competitive advantage in a changing retail environment.

Strong Balance Sheet and Cash Flow Position

The company maintained a strong balance sheet at the end of the half. Net assets and total assets both increased compared with the prior corresponding period. The group reported a low net debt-to-equity ratio of 5.89 per cent, compared with 5.40 per cent in 1H25.

Operating cash flows remained strong. Management emphasised ample cash reserves and solid cash conversion. The company stated that this position supports ongoing investment in store networks, digital platforms and property assets.

The balance sheet strength also provides capacity to manage economic uncertainty. The group continues to operate with conservative gearing, which reduces financial risk. Management indicated that liquidity levels remain sufficient to fund working capital and capital expenditure.

Franchising Operations and Margin Improvement

The franchising operations segment recorded improved profitability. Profit before tax from franchising operations rose 27.9 per cent to $27.92 million. The segment also achieved a higher margin compared with the previous year.

Management attributed the improvement to higher franchisee sales and stable operating costs. The company maintained marketing investment while achieving sales growth. This approach helped protect brand visibility without increasing expense ratios.

Franchisees benefited from category expansion and continued customer demand for home, technology, and furniture products. The integrated retail, franchise, property, and digital model continues to underpin performance across markets.

Also Read: Commonwealth Bank Launches A$90M AI Upskilling Program

Outlook and Strategic Focus

Management stated that the company will continue to focus on disciplined cost control and international expansion. The group plans to invest further in the United Kingdom store network and digital capabilities. It will also maintain its property ownership strategy to support long-term stability.

The company enters the second half of FY2026 with a solid financial base. Strong earnings growth, stable cash flow, and a low gearing ratio provide flexibility. International diversification remains central to future performance.

The 1H26 results reflect growth in system sales, profit, and earnings per share. Franchise operations and overseas company-operated stores both contributed to the outcome. The property portfolio added earnings support and asset value uplift.

Overall, the half-year performance demonstrates operational resilience and balanced growth across segments. The company continues to position itself for sustained performance in domestic and international retail markets.

FAQs

- What did Harvey Norman report in its 1H26 financial results?

Ans. Harvey Norman reported a 6.9 per cent increase in total system sales to $5.16 billion for the half year ended 31 December 2025. Profit before tax rose 16.5 per cent to $466.31 million. Basic earnings per share increased to 25.84 cents. The company also increased its interim dividend.

- How did franchise and international operations perform in 1H26?

Ans. Australian franchise operations recorded steady sales growth during the half year. Overseas company-operated stores delivered stronger growth, with markets including New Zealand, Ireland, Singapore, Malaysia, Slovenia and Croatia contributing to improved earnings.

- Did Harvey Norman increase its dividend in 1H26?

Ans. Yes. The company increased its fully franked interim dividend for the half year ended 31 December 2025. The dividend increase reflects improved profitability and cash flow strength.

- What drove profit growth in the half-year results?

Ans. Higher system sales supported the profit increase. The company also maintained cost discipline and improved margins across several segments. International retail operations contributed meaningfully to earnings growth.

- How did the property portfolio impact results?

Ans. The property segment generated stable earnings during the half year. The company also recognised property revaluation gains, which supported reported profit. The global property portfolio remains valued at approximately $5 billion.

- What is the company’s financial position following 1H26?

Ans. Harvey Norman reported a strong balance sheet position. The group maintained a low net debt-to-equity ratio and strong operating cash flow. Management stated that liquidity remains sufficient to fund future growth initiatives.

- What is the outlook following the 1H26 results?

Ans. The company entered the second half of FY2026 with continued sales momentum. Management remains focused on disciplined cost control, international expansion and maintaining balance sheet strength.

{kind=link}