Aurizon has rewarded shareholders with a higher interim dividend after delivering stronger half-year earnings and cash flow, signalling confidence in its outlook and capital management strategy.

The rail freight operator increased its dividend payout ratio to 90% of underlying net profit after tax and declared an interim dividend of 12.5 cents per share, 90% franked. The company will pay the dividend on 25 March 2026 to shareholders on the register at 3 March 2026.

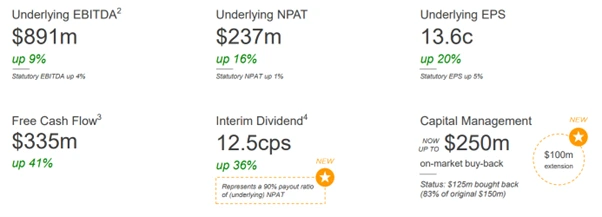

The lift in dividends follows a solid financial performance for the half year ended 31 December 2025. Aurizon reported EBITDA of $891 million, up 9% on the prior corresponding period, while net profit after tax rose 16% to $237 million. Earnings per share climbed 20% to 13.6 cents.

Figure 1: Highlights of the Aurizon Holdings’ strong financial results in first half of 2026 [Aurizon]

Stronger earnings underpin higher payout

Aurizon drove earnings growth through higher volumes, a regulatory revenue uplift and disciplined cost control. The company’s Bulk, Coal and Network divisions all delivered improved EBITDA, with Network benefiting from an uplift in track access revenue and Coal supported by higher volumes and favourable operating costs.

Managing Director and CEO Andrew Harding said the result highlighted the strength of Aurizon’s core operations and the continued growth in bulk and containerised freight.

For investors, the key takeaway sits in the company’s decision to return a larger share of profits. By lifting the payout ratio to 90% and boosting the interim dividend from 9.2 cents in the prior period to 12.5 cents, Aurizon has delivered a 36% increase in dividends per share.

That move signals confidence in both earnings quality and cash generation.

Free cash flow strengthens balance sheet flexibility

Aurizon generated free cash flow of $335 million for the half, up 41% on the prior period. The stronger cash flow gives the board room to lift dividends while still funding capital expenditure and growth initiatives.

The company also extended its on-market share buy-back by a further $100 million, taking the total program to up to $250 million. That extension adds another lever for capital returns and supports earnings per share by reducing the share count.

For income-focused investors, the combination of a higher dividend payout and ongoing buy-backs strengthens total shareholder returns. For long-term holders, the disciplined capital allocation approach suggests management intends to balance growth with consistent distributions.

Upgraded full-year dividend outlook

Aurizon went a step further and upgraded its full-year dividend guidance. The company now expects to pay 22–23 cents per share for FY2026, up from its previous guidance of 19–20 cents per share.

That upgrade provides greater visibility for investors who rely on dividend income. It also reflects management’s confidence in maintaining earnings momentum through the second half, assuming no major supply chain disruptions.

Aurizon maintained its full-year underlying EBITDA guidance range of $1.68 billion to $1.75 billion, reinforcing expectations of stable operating performance.

Strategic certainty supports long-term value

Beyond the numbers, Aurizon continues to progress strategic initiatives that could underpin long-term returns.

The company submitted a draft 10-year undertaking for the Central Queensland Coal Network late last year. Subject to regulatory approval, the new framework could deliver an average annual revenue uplift of $45 million across the undertaking period.

Aurizon also completed its Network Ownership Structure Review and decided to retain its integrated above and below rail model. Management concluded that keeping full ownership of the Network would deliver the best long-term value for shareholders.

For investors, that decision removes uncertainty around potential structural changes and signals a focus on stability and steady cash flows.

What it means for investors

Aurizon’s latest dividend increase sends a clear message. The company believes it can generate reliable earnings, convert them into cash and return a substantial portion to shareholders.

Investors gain:

- A higher fully franked interim dividend.

- Improved visibility on full-year dividend expectations.

- Ongoing capital management through buy-backs.

- Confidence in stable core businesses and regulatory settings.

However, Aurizon still operates in sectors exposed to commodity demand, weather events and supply chain risks. Management has flagged the importance of avoiding major disruptions such as derailments or prolonged wet weather.

Even so, the combination of stronger profits, higher free cash flow and a clear capital return strategy places Aurizon in a solid position.

For dividend-focused investors, the latest increase strengthens Aurizon’s appeal as a steady income generator within the Australian infrastructure and freight landscape. For growth-oriented shareholders, disciplined cost control and strategic clarity offer support for sustained earnings over the medium term.

As Aurizon moves into the second half of FY2026, the market will watch whether the company can maintain volume growth and execute its regulatory and cost initiatives. For now, the dividend uplift signals management’s confidence — and delivers a tangible reward to investors.