Rare earths have become central to the worldwide technology and energy transition. Dysprosium, neodymium, and praseodymium remain the most strategic of the metals. Electric vehicles, defence systems, and clean energy infrastructure critically depend on them. Has electrification put investors on edge as demand rises?

The supply security race is putting pressure on the industry. Presently, China is a major player in the rare earth supply chain. Some Western markets are creating projects to avoid dependency. This change spurs new investment opportunities. Australia, Canada, and the U.S. are setting up alternative supply chains.

Strategic rare earths driving global technology and energy transition.

What Makes Dysprosium Important In Global Supply Chains?

Dysprosium acts as a heavy rare earth and is allied with the manufacture of high-strength permanent magnets, which are essential for wind turbines and electric vehicles. With dysprosium in machining, the prototype offers heat resistance; that is, the prototype can be assured to endure every extreme condition. Demand for this rare element grows with the expansion of the EV and wind-power industries.

The Chinese hold most of the world’s dysprosium reserves, creating risks for supply stability. Keeping prices constant is difficult when the Chinese policy restricts exportation. Such price instability causes significant price spikes, making investments difficult. Companies outside China are now looking for alternative sources.

Increasingly, Australian rare earth projects have begun targeting dysprosium. A number of companies, such as Northern Minerals, are developing projects with deposits rich in dysprosium. Such assets are gaining global interest in terms of supply diversification.

How Does Neodymium Power The Clean Energy Future?

Neodymium is critical to neodymium-iron-boron (NdFeB) magnets. These magnets power electric motors coupled with renewable energy systems. Without neodymium, the cost of producing electric vehicles would rise significantly.

Demand forecasts are bullish. Analysts expect demand for neodymium to grow by double digits this decade. Scaling of production is by far the biggest driver, given that EV manufacturers require much neodymium. Wind energy projects also demand a huge supply of neodymium magnets.

China continues to fulfil the producer role for neodymium. Nonetheless, ASX-listed companies like Lynas Rare Earths are among the few non-Chinese suppliers. Investors appreciate Lynas for securing supplies in the West. Its processing works in Malaysia for industries worldwide.

Neodymium powers EV motors and renewables, preventing soaring production costs.

Praseodymium Strengthens Market Position

Praseodymium is another rare-earth element important for making magnets. It helps make the NdFeB magnet stronger and more efficient. The requirement to pass higher performance according to industry expectations serves to increase the demand for praseodymium.

Praseodymium is used in alloys, aircraft engines, and renewable energy systems. It has a similar market outlook as neodymium, with increasing consumption tied to EVs. A high supply risk continues due to the concentration in China.

For investors, the praseodymium-related assets are strategic. Australian and Canadian juniors are exploring praseodymium-rich deposits. With the diversification of supply chains, these projects could rise in importance.

Rare Earths Investors Should Focus On Supply Risks

Supply-chain risk is the main concern for rare earth investors. China’s unmatched dominance in processing must be recognised. With rising geopolitical tensions, exports would be subjected to laws imposed by those countries. Investors tracking dysprosium, neodymium, and praseodymium have to keep an eye on policy changes.

The West is funding projects along the rare earth supply chain. The US and EU consider these metals critical. Australia is also going ahead with supporting projects through grants and strategic partnerships. This government support indeed boosts investor confidence.

ASX-listed players such as Arafura Rare Earths and Hastings Technology Metals are building magnet metal projects. These companies represent Australia joining the global supply chain and are gaining momentum to compete with the Chinese.

Why Should Investors Watch Rare Earths Now?

Global demand for EVs and renewables is accelerating. Chemicals are positioned at the centre of this growth. Dysprosium, neodymium, and praseodymium rank among the most critical magnet metals, needing the highest security in supply to complete their strategic value.

Market analysts profess strong long-term support for prices. Investors have started leaning towards juniors with exposure to rare earth. Big names of companies with production in place, like Lynas, remain bankable. Diversified portfolios with rare earths can ameliorate geopolitical risk.

For exposure to clean energy growth, rare earths have now become an imperative sector for all investors. These metals provide strategic advantages as well as economic advantages.

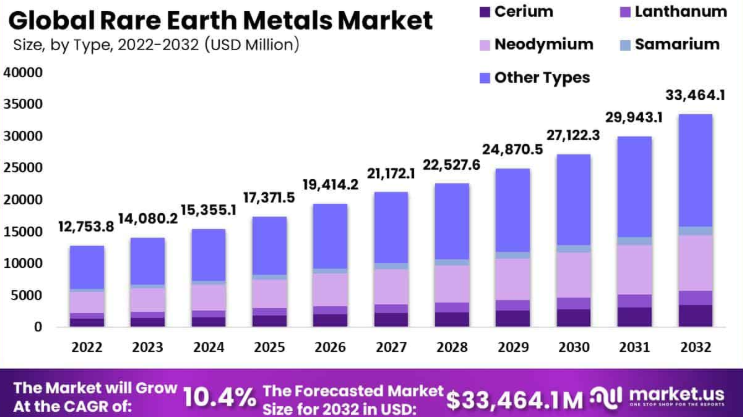

Rare Earths Emalemts Market Forecast

Market Outlook For Rare Earths In 2025

The market outlook for 2025 for rare earths remains strongly positive. Demand grows for dysprosium, neodymium, and praseodymium. They are needed for EV motors, wind turbines, and defence technologies. Price support is expected to be strong with the electrification trend on the rise globally, according to analysts. China remains the largest supplier, but until recently, Australia, Canada, and the US have begun scaling their projects. On the ASX, companies are emerging as very important players in altering the global supply chain. Investors focus on companies that will be able to supply sustainable production and processing capacity. The industry is fast becoming a key portfolio for clean energy and strategic defence investments around the world.

Also Read: The Rare Earths Race: Who Controls the Future of Tech & Clean Energy Supply Chains

Frequently Asked Questions (FAQs)

- Why are dysprosium, neodymium, and praseodymium important for clean energy?

They are among the key elements for manufacturing permanent magnets that go into the construction of EVs, wind turbines, and defence systems.

- Which countries dominate in the supply of rare earths?

China leads worldwide for mining and processing, but Australia, the US, and Canada are all increasing their capacities.

- What companies in the ASX are rare earth leaders?

The large names include Lynn Rare Earths, Arafura Rare Earths, Hastings Technology Metals, and Northern Minerals.

- Are price risks related to supply risks?

Restrictions in Chinese exports or political disruptions can cause sudden increases in prices for rare earth metals.

- What is the forecast for rare earth demand?

Strong growth is expected due to rising EV sales and the deployment of renewable energy.

- Can rare earth be dubbed as a sustainable investment?

Yes, rare earth supports clean-energy and defence technologies, though supply risks remain.

- Are rare earths an investment worthy of portfolios?

Yes, it can provide a hedge against supply shocks worldwide and from demand for clean energy.