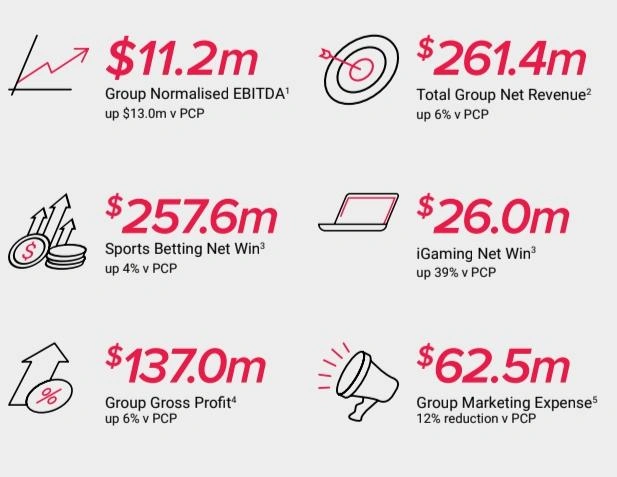

The PointsBet FY25 annual report marks a significant turning point for pari-mutuel and iGaming operators. With a normalised EBITDA level of $11.2 million, PointsBet cemented its first positive EBITDA financial year. It reflected a drastic turnaround in performance from previous losses.

Group net revenue for FY25 rose to $261.4 million, reflecting 6% year-on-year growth. Results were driven by higher net win in both sports betting and iGaming. Sports betting net win climbed 4% to $257.6 million, while iGaming net win surged 39% to $26.0 million, highlighting the segment’s contribution to growth.

Marketing expenses dropped 12% to $62.5 million, indicating tighter cost discipline. The improved cost control, together with revenue growth, would lay the foundation for profitability.

How did operational growth fuel EBITDA positive FY25?

PointsBet’s operational growth in FY25 was anchored in core markets after exiting the U.S. The company now concentrates on Australia and Ontario, Canada, where scale advantages are more readily achieved.

In Australia, statutory EBITDA made $30.1 million. On a like-for-like basis, adjusting for higher product fees and POCT, EBITDA was $39.2 million versus $26.8 million last year, pointing to a sturdy domestic market. Ontario’s growth was positive but still below expectations. The downside mostly lay in the casino vertical, which underperformed. Yet, the market remains a centre of focus because of its long-term revenue potential.

By investing in operational efficiency and targeted marketing, PointsBet enhanced its digital wagering and iGaming platform and improved margins. This operational growth had a direct impact on profitability.

What challenges remain for PointsBet FY25 annual report stakeholders?

Despite a turnaround in the EBITDA, the company registered a statutory net loss of $18.2 million versus $42.3 million in FY24. Reduced loss highlights progress but also underscores the work ahead. No dividends were declared; none are likely in the near future, given reinvestment needs.

Another impacting factor is ownership changes, on which PointsBet tries to strike an equilibrium. In 2025, MIXI Australia started a takeover bid, which saw it become the controlling shareholder with 66.43% of the company’s shares by mid-September. This development in the other way adds a layer of complexity for current investors, as strategic direction may be shunted under newly dominant control.

The blend of improving profitability and residual corporate activity means there are opportunities to grasp and uncertainties to weigh for stakeholders.

MIXI becomes shareholder of 66.43% in year 2025

Why is this operational growth pivotal?

The achievement of EBITDA positivity in FY25 validates management’s stand that it was best to rationalize those operations that were not attracting any significant revenue or profit. The shift to focus on markets in which PointsBet can compete effectively has yielded clear gains.

The upside turned around the perception among investors at a time when there’s an ownership transition underway. During the year, the company’s shares strengthened from $0.47 to a high of $1.19, buoyed by market confidence about the improved financial health and operational capability of PointsBet.

Being EBITDA positive also translates into financial flexibility. Narrowing losses and a more controlled marketing spend mean PointsBet can look to reinvest in technology and customer acquisition with a handsome balance sheet behind it.

Where will growth come next?

PointsBet is trying to consolidate its strength in Australia while aiming to build a better result in Ontario. The company is still rolling out scalable, cloud-owned wagering and iGaming technology.

Management strives to overcome the shortcomings that have persisted in Ontario casino operations with a strategic intent to secure more market share while diversifying the revenue streams other than sports betting. Product innovation shall likely be the core driver of growth in FY26, especially in digital gaming.

A lean operational style remains important. The FY25 results are proving that EBITDA can be sustained on lean costs coupled with strategic investments in growth markets.

What is the outlook?

While building a basis for future performance, the PointsBet FY25 annual report notes that management upheld that operational growth, cost discipline, and product innovation will remain areas of core strategies.

The presence of MIXI as the majority shareholder presents a challenge and an opportunity. Even though there might arise some uncertainty stemming from governance changes, MIXI’s presence could accelerate PointsBet’s ability to scale and innovate. With a strong revenue base and a positive EBITDA result, PointsBet can better contend with these changes as compared to years past.

Going forward, with leaner operations in tow, PointsBet’s focus on its two core regions sets the stage for sustainable profitability. Operational growth in FY25 will be an essential mark for investors to check progress in FY26.

Also Read: Locksley Resources (ASX: LKY) Annual Report 2025: Critical Minerals Update

FAQs

Q1: Did PointsBet achieve EBITDA positive FY25?

Yes. The company reported normalised EBITDA of $11.2 million, thus recording its first positive EBITDA year.

Q2: What was the source of growth operationally for PointsBet in FY25?

Growth was Royalty higher sports betting and iGaming net win, coupled with lower marketing expenses.

Q3: Did PointsBet make a net profit in FY25?

No. The company registered a statutory net loss of $18.2 million, despite the turnaround of EBITDA.

Q4: What is the effect of the MIXI takeover on the outlook of PointsBet?

MIXI holds 66.43 % of shares, giving it control. This will expedite strategic initiatives and provide support for future growth.